MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

April 3, 2020: Oil prices jumped 25% on Thursday when President Donald Trump tweeted that he expected Saudi Arabia and Russia to end the oil price war, and that production cuts would amount to 10 or even 15 million barrels per day. Markets then wavered up and down, Russia stating they had no discussion yet with Saudi Arabia. There has been no official action by Saudi Arabia, Russia or the OPEC+ group. A massive production cut could not happen immediately but talks look increasingly likely. Buyers bid prices up, not wanting to be left behind. The COVID-19 pandemic continues to rage. The supply and demand balance points to weaker prices. Roughly one third of the world’s population is sheltering in place. Note that even if the world cut production by 10 or 15 mmbpd, the International Energy Agency estimated last week that oil demand is down by as much as 20 mmbpd.

The Bureau of Labor Statistics (BLS) has just released the Employment Situation Report for March, showing total nonfarm payroll employment fell by 701,000 in March. The unemployment rate rose to 4.4 percent. Markets are edging lower, but not as dramatically as they might. Can it be that the weekly reports of unemployment claims prepared the market for such a massive loss of jobs in March? Can markets prepare for an even more significant drop in April?

The U.S. is now far and away the hotspot of the COVID-19 pandemic. All fifty of the United States have confirmed cases. Every state governor has declared a state of emergency. The U.S. has 245,573 confirmed cases, more than twice the number reported in Spain and Italy. U.S. fatalities are reported at 6,058. Global confirmed cases have passed the million mark, standing at 1,030,628, with the death toll more than doubling to 54,137 since last week. This week brought a low WTI crude price of $19.90/b. Many market analysts predict prices will soon fall below $20/b. WTI crude futures prices opened at $24.81/b this morning, up by $1.52/b (6.5%) for the week, and the rally is stabilizing this morning. This week appears ready to break the five-week downward slide in oil prices.

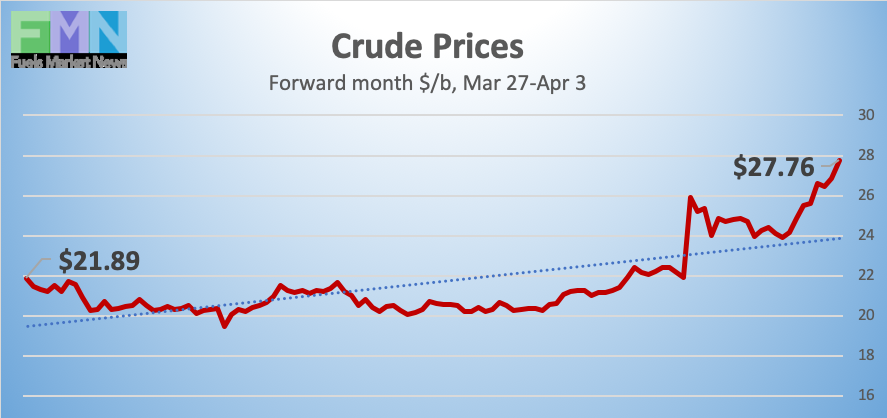

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, March 27, at $23.29/b. Prices fell to open at $20.93/b on Monday. However, yesterday’s price surge brought today’s market opening up to $24.81/b, so the Friday-to-Friday week brought a rebound of $1.52 (6.5%). This week may end in the black. The prior three weeks brought a combined drop of $22.80. Our weekly price review covers hourly forward prices from Friday, March 27th, through Friday, April 3rd. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

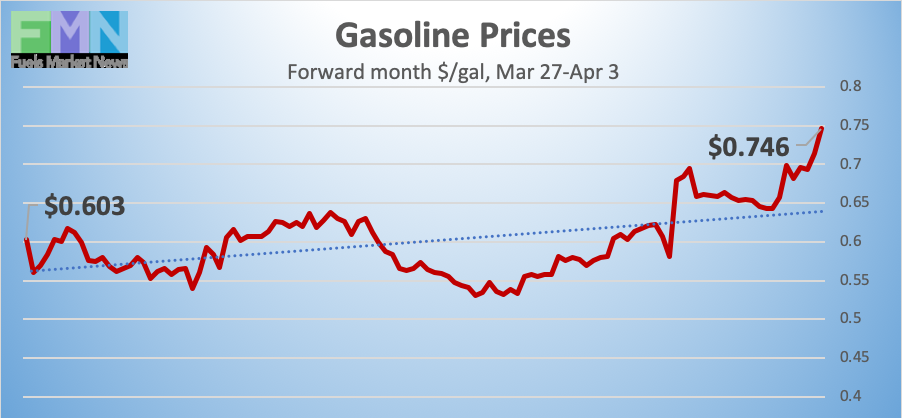

GASOLINE PRICES

Gasoline opened on the NYMEX at $0.5713/gallon on Friday, March 27, and prices rebounded to open at $0.6586/gallon on Friday, April 4, including a switch to the next forward month contracts. This was an increase of 8.73 cents (15.3%). The prior three weeks had brought a massive collapse totaling nearly 95 cents per gallon. U.S. average retail prices for gasoline dropped by 11.5 cents/gallon during the week ended March 30th. Futures prices for gasoline ramped up again this morning in early trades, and currently are ebbing. Nonetheless, the week appears to be ready to finish in the black. Trades are occurring mainly in the range of $0.65-$0.76/gallon. The latest price is $0.7114/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.0782/gallon on Friday, March 27, and opened on Friday, April 4, at $0.9969/gallon, a decline of 8.13 cents (7.5%). U.S. average retail prices for diesel fell by 7.3 cents/gallon during the week ended March 30th. Retail prices for diesel have fallen for twelve consecutive weeks. Prices today are showing a rise-and-fall, following yesterday’s more dramatic spike-and-fall cycle. Diesel futures prices may finish in the red this week. Contracts have been trading mainly in the $0.99-$1.10/gallon range. The latest price is $1.0547/gallon.

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, March 27, at $23.29/b. Prices fell to open at $20.93/b on Monday, then surged to close at $25.32 on Thursday. Prices relaxed to open at $24.81/b at today’s market opening. The Friday-to-Friday week brought a gain of $1.52 (6.5%). Today, prices rallied in early trades, then tailed back down, likely based on the Jobs Report. But prices remain up for the week. A finish in the black will break a streak of losses extending back for the last five weeks. WTI futures prices currently are trading mainly in the range of $25.00-$28.50/b. The latest price is $26.53/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices jumped 25% on Thursday when President Donald Trump tweeted that he expected Saudi Arabia and Russia to end the oil price war by cutting production by 10 million barrels per day. He later raised the estimate to 15 mmbpd. Prices retreated when Russia stated that no such deal was in the works. Prices then crept back up when Saudi Arabia called for an urgent meeting with the OPEC+ group and “another group of countries.” Market experts quickly debunked the idea that a production cut of 10 million bpd could happen immediately, but traders did not want to be left behind, and prices are climbing. The rally may not last, however, if the OPEC+ group fails to agree to meet, or if Saudi Arabia and Russia fail to make conciliatory statement of some sort. The fundamentals point to weaker prices. Roughly one third of the world’s population is sheltering in place. Even if 10-15 mmbpd of production cuts are made, the International Energy Agency (IEA) estimated last week that oil demand will drop by as much as 20 million barrels per day. Storage and transportation sectors are being overwhelmed.

The Bureau of Labor Statistics (BLS) has just released the Employment Situation Report for March, showing total nonfarm payroll employment fell by 701,000 in March. The unemployment rate rose to 4.4 percent. The coronavirus pandemic is beginning to show up in the official statistics. Most of the jobs lost were in the leisure and hospitality sectors. Declines also occurred in social assistance, professional and business services, retail trade, and construction. Declines also occurred, paradoxically, in health care. Normally scheduled services, including office visits to physicians and dentists, have been cancelled.

The U.S. is now far and away the hotspot of the COVID-19 pandemic. Cases have been confirmed in all fifty of the United States, and every state governor has declared a state of emergency. Most states have initiated some form of shelter-in-place ordinance. Sparsely populated North Dakota is the only state remaining that has not mandated a statewide limit on gatherings. As of the time of this writing, the U.S. has 245,573 confirmed cases, more than twice the number reported in Spain and Italy. Fatalities are reported at 6,058. Global confirmed cases have passed the million mark, standing at 1,030,628, with the death toll more than doubling to 54,137 since last week. This week brought a low WTI crude price of $19.90/b. Many market analysts predict that oil prices will fall below $20/b, despite the current rally. WTI crude futures prices opened at $24.81/b this morning, up by $1.52/b (6.5%) for the week. Today’s price strength appears ready to break a five-week downward slide in oil prices.

Stock markets have been volatile this week. The Dow Jones Industrial Average rose on Monday, fell on Tuesday and Wednesday, and rose again (alongside oil) on Thursday. As of Thursday, the battered Dow Jones had climbed back above 21,400 points. This was a recovery of over 2,800 points from the nadir of March 24th, but still down 7,900 points from the recent high in mid-February. Today, stock markets are edging lower, based largely on the BLS Jobs Report. However, the impact of 701,000 lost jobs has not yet pulled down markets as much as it might have. Was this because markets had been digesting weekly unemployment claims, preparing for a dour Jobs Report for March? Markets may need to prepare for a worse Jobs Report in April.

The American Petroleum Institute (API) reported a crude inventory build of 10.48 mmbbls. The API also reported a build of 6.1 mmbbls of gasoline, and a drawdown of 4.5 mmbbls from diesel inventories diesel. The API’s net inventory draw was 12.08 mmbbls. Market analysts had predicted across-the-board inventory additions, but with a total addition to inventories of only 6.6 mmbbls.

U.S. Energy Information Administration (EIA) official statistics showed more significant additions to inventories. The addition to crude stocks was 13.833 mmbbls, the addition to gasoline stocks was 7.524 mmbbls, and the drawdown from distillate stockpiles was 2.194mmbbls. The EIA net result was a major inventory build of 19.163 mmbbls.

The EIA also reported that U.S. crude production during the week ended March 27th remained unchanged from the prior week’s level of 13.0 mmbpd. According to this weekly data series, U.S. crude production averaged 13.025 mmbpd in February 2020, the highest total ever. An increasing number of rigs have been idled, however, so the production numbers are expected to ease soon.