Excerpted from This Week in Petroleum

In October 2022, the New York Harbor spot price for ultra-low sulfur diesel (ULSD) averaged $4.36 per gallon (gal), the highest monthly average price since May 2022 and the second-highest monthly average price on record (Figure 1). The diesel crack spread—the difference between the price of crude oil and an equivalent volume of diesel—marked a historic high at $2.14/gal in October, even higher than during the summer. By comparison, this high was $1.61/gal, or over four times, more than the diesel crack spread had been in October 2021. The increases in distillate prices, both in the United States and globally, have been the result of multiple factors:

- Low inventories of distillate fuel oil (which is primarily consumed as diesel), both in the United States and globally

- Increasing demand for distillate, partially related to seasonal drivers such as agricultural demand and home heating demand in the Northeast

- Less production of distillate related to seasonal refinery maintenance, as well as lower refinery utilization in Europe following labor strikes

- Higher costs of transporting distillate ahead of the EU’s February ban on petroleum product imports from Russia

U.S. inventories of distillate fuel oil have been below the five-year (2017–2021) low since the start of 2022 (Figure 2). Since April, total U.S. distillate inventories have been below the five-year low and more than 20% below the five-year average. The Northeast—the combined New England (PADD 1A) and the mid-Atlantic (PADD 1B) regions—has been more than 40% below the five-year low since the end of July. The low inventories have primarily been the result of less global refining capacity since 2020, as well as high demand in early 2022 and global trade disruptions later in the year linked to Russia’s full-scale invasion of Ukraine. Consumption through the summer in 2022 has remained below pre-pandemic levels, but has increased relative to 2020. Even when consumption has not been at above-average levels, the higher relative consumption combined with lower refinery production of distillate has contributed to the lower inventories. High crude oil prices contribute directly to higher prices for petroleum products such as distillate fuel oil, while constraints on refinery capacity further contribute to high prices by increasing the crack spread associated with the value of refining.

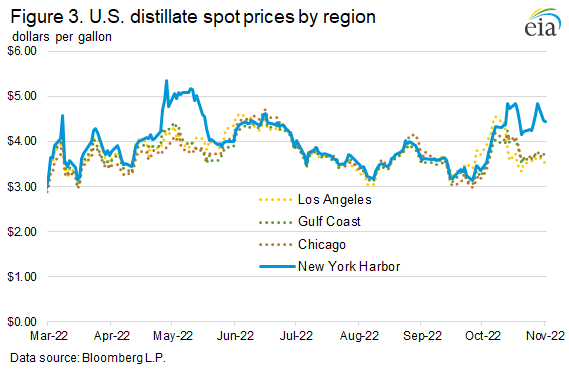

Prices at the New York Harbor pricing benchmark are higher relative to other U.S. benchmarks at Chicago, the Gulf Coast, or Los Angeles (Figure 3). The ULSD spot price at New York Harbor averaged 56 cents/gal higher than the Gulf Coast benchmark in October, compared with 17 cents/gal higher from January through September 2022. The reason for the increase at New York Harbor in October is a combination of normal seasonal increases in demand, abnormally low inventories, and limited distillate supplies available for import. As we discussed in our Winter Fuels Outlook, U.S. distillate demand is seasonal, in part because of its use in home heating mostly in the Northeast. The beginning of the winter demand cycle for home heating oil is likely the primary catalyst for rising prices because rising seasonal demand is drawing on already substantially strained regional inventories.

In addition to market conditions in the United States, a strike by refinery workers in France took several of that country’s refineries offline at the end of September through most of October. Reuters estimated the total refinery capacity that was taken offline by the strikes at 740,000 barrels per day in early October (b/d). Lower French refinery utilization is likely to further strain already low European distillate inventories, and the effects could ripple through the global market. In Europe, tight distillate supplies present additional complications compared with the United States because distillate is more widely used as the primary transport fuel in light-duty vehicles. Reduced natural gas imports into Europe from Russia may also be increasing demand for distillate as a potential alternative fuel for power generation, industry, or home heating oil this winter. As in the United States, distillate inventories at the Amsterdam Rotterdam Antwerp (ARA) storage hub have been well below their five-year average since the start of 2022 and were more than 1.0 million barrels below the five-year average through most of the summer (Figure 4).

Although seasonal factors such as home heating are important in determining changes in U.S. distillate demand over the course of the year, distillate fuel oil is primarily consumed in the on-road transportation sector, which includes medium- and heavy-duty trucking. Large volumes of distillate are also consumed in the commercial, industrial, and rail sectors. As a result, distillate fuel demand is strongly tied to economic conditions and expectations. Concerns about rising interest rates and increasing inflation were also likely contributing to some relative weakness in distillate demand in September. The most recent increase in distillate prices in October follows a period of lower distillate demand (measured as product supplied) in September, which had been reducing some pressure on distillate prices (Figure 5). The low demand in September may have been partially a result of caution by rail operators who may have been reluctant to restock their diesel supplies because of the threat of a rail strike at that time. Renewed concerns about a rail strike in November may similarly contribute to some weakness in distillate demand from the rail sector.

Another uncertain factor relating to global distillate supplies in the near term is the potential for increasing refinery production of distillate fuel oil in China. China may begin exporting more distillate fuel oil in response to higher export quotas from the Chinese government, although whether exports from China actually rise to fill these quotas remains uncertain. In addition, trade press reports the first sales of distillate and other petroleum products from the newly started Al-Zour refinery in Kuwait, which could become a new source of distillate in the coming months.

The potential for reducing market pressure on inventories through new production is constrained by global capacity to transport distillate. A large volume of distillate fuel oil imports from Russia previously flowed into Europe by pipeline. But as buyers in Europe turn elsewhere to procure distillate, global demand for clean product tanker shipping has been increasing. (Clean product tankers are tanker ships that carry refined products such as gasoline, distillate, or jet fuel, as opposed to dirty product tankers that carry crude oil or residual fuel oil.) Distillate volumes needed to replace pipeline volumes will most likely need to travel by tanker, and tanker routes are also likely to become longer as European buyers increase purchases from the Middle East and United States. Even if inventories of distillate fuel oil on the U.S. Gulf Coast or Asia were to increase, limitations on available shipping capacity are likely to continue contributing to price premiums in the Northeast or European distillate markets because of higher tanker shipping rates.