Release Date: Feb. 7, 2023

Forecast overview

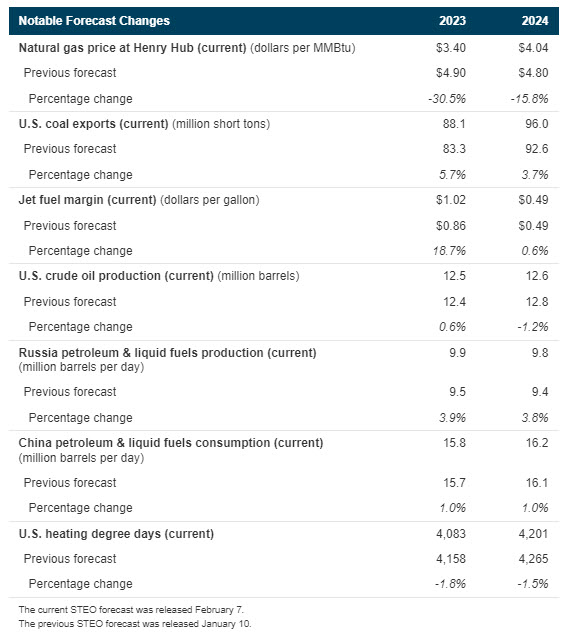

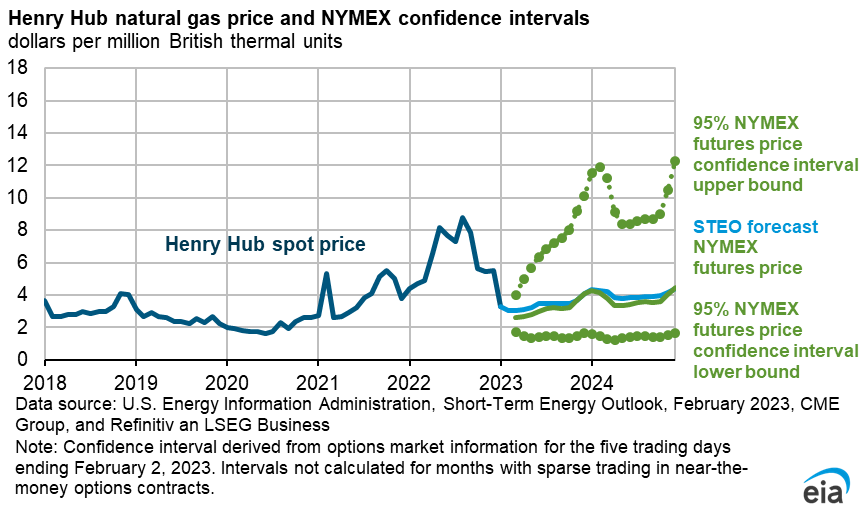

- Natural gas prices. We forecast that the Henry Hub natural gas spot price will average $3.40 per million British thermal units (MMBtu) in 2023, down almost 50% from last year and about 30% from our January Short-Term Energy Outlook (STEO) forecast. We revised our outlook for Henry Hub prices as a result of significantly warmer-than-normal weather in January that led to less-than-normal consumption of natural gas for space heating and pushed inventories above the five-year average.

- Natural gas storage. As a result of less-than-normal natural gas consumption in January, natural gas inventories ended the month above their five-year (2018–2022) average. We now expect inventories will close the withdrawal season at the end of March at more than 1.8 trillion cubic feet, 16% more than the five-year average.

- Global liquid fuels consumption. We expect global liquid fuels consumption to increase by 1.1 million barrels per day (b/d) in 2023 and by 1.8 million b/d in 2024, driven primarily by growth in China and other non-OECD countries. The outcomes of our demand forecast remain uncertain as China shifts away from its zero-COVID-19 policy and global economic conditions evolve.

- Global liquid fuels production. We expect oil production in Russia to average 9.9 million b/d in 2023, down 1.1 million b/d from 2022. Our forecast for Russia’s 2023 production is 0.4 million b/d more than in the January STEO because crude oil liftings data suggest that Russia’s exports have remained higher than we expected following the EU’s ban on seaborne imports of crude oil from Russia that began on December 5. However, we still forecast Russia’s oil production to fall in the coming months, as we expect the EU’s ban on seaborne petroleum products from Russia that began February 5 will cause refineries in Russia to reduce crude oil inputs, which will disrupt crude oil production.

- Electricity generation. Electricity generation in our forecast falls by 2% in 2023 and then rises by 2% 2024. The generation mix continues to shift away from coal. The share of U.S. electricity generated from coal falls from 20% in 2022 to 17% in 2024. As the share of coal declines, it will be offset by increases in the share of generation from renewable sources of energy, which rises from 22% in 2022 to 26% in 2024.

- S. GDP growth. Based on the S&P Global macroeconomic model, we assume U.S. real GDP will contract slightly in the first half of 2023 (1H23), partly resulting from a decline in residential fixed investment. GDP growth picks up in 2H23 and reaches an annual average of 2.1% in 2024.