Release Date: Sept. 8, 2021

Forecast Highlights

- The September Short-Term Energy Outlook (STEO) remains subject to heightened levels of uncertainty related to the ongoing recovery from the COVID-19 pandemic. U.S. economic activity continues to rise after reaching multiyear lows in the second quarter of 2020 (2Q20). U.S. gross domestic product (GDP) declined by 3.4% in 2020 from 2019 levels. This STEO assumes U.S. GDP will grow by 6.0% in 2021 and by 4.4% in 2022. The U.S. macroeconomic assumptions in this outlook are based on forecasts by IHS Markit. Our forecast assumes continuing economic growth and increasing mobility. Any developments that would cause deviations from these assumptions would likely cause energy consumption and prices to deviate from our forecast.

- Brent crude oil spot prices averaged $71 per barrel (b) in August, down $4/b from July but up $26/b from August 2020. Brent prices have risen over the past year as result of steady draws on global oil inventories, which averaged 1.8 million barrels per day (b/d) during the first half of 2021 (1H21). We expect Brent prices will remain near current levels for the remainder of 2021, averaging $71/b during the fourth quarter of 2021 (4Q21). In 2022, we expect that growth in production from OPEC+, U.S. tight oil, and other non-OPEC countries will outpace slowing growth in global oil consumption and contribute to Brent prices declining to an annual average of $66/b.

- More than 90% of crude oil production in the Federal Offshore Gulf of Mexico (GOM) was offline in late August following Hurricane Ida. As a result of the outage, GOM production averaged 1.5 million b/d in August, down 0.3 million b/d from July. We expect that crude oil production in the GOM will gradually come back online during September and average 1.2 million b/d for the month before returning to an average of 1.7 million b/d in 4Q21.

- Total U.S. crude oil production averaged 11.3 million b/d in June—the most recent monthly historical data point. We forecast it will remain near that level through the end of 2021 before increasing to an average of 11.7 million b/d in 2022, driven by growth in onshore tight oil production. We expect growth will result from operators beginning to increase rig additions, offsetting production decline rates.

- We estimate that 98.4 million b/d of petroleum and liquid fuels was consumed globally in August, an increase of 5.7 million b/d from August 2020 but still 4.0 million b/d less than in August 2019. We forecast that global consumption of petroleum and liquid fuels will average 97.4 million b/d for all of 2021, which is a 5.0 million b/d increase from 2020, and by an additional 3.6 million b/d in 2022 to average 101.0 million b/d, almost even with 2019 levels.

- U.S. regular gasoline retail prices averaged $3.16 per gallon (gal) in August, the highest monthly average price since October 2014. Recent gasoline price increases reflect rising wholesale gasoline margins amid relatively low gasoline inventories. In addition, recent impacts from Hurricane Ida on several U.S. Gulf Coast refineries are adding upward price pressures in the near term. Estimated gasoline margins surpassed 70 cents/gal in late August. We expect margins will remain elevated in the coming weeks as refining operations as U.S. Gulf Coast remain disrupted. We forecast that retail gasoline prices will average $3.14/gal in September before falling to $2.91/gal, on average, in 4Q21. The expected drop in retail gasoline prices reflects our forecast that gasoline margins will decline from currently elevated levels, both as a result of rising refinery runs as operations return in the first half of September following Hurricane Ida and because of typical seasonality.

- Propane net exports in our forecast average close to 1.2 million b/d for the remainder of 2021, reflecting elevated global demand for U.S. propane and reduced supply from other sources related to ongoing OPEC+ production cuts. In 1H22, we assume global production of propane and butanes will rise as OPEC+ countries increase crude oil production. We expect this increase will limit additional demand for U.S. propane exports, despite growing global propane demand, and keep U.S. net propane exports close to 1.2 million b/d in 2022.

Natural Gas

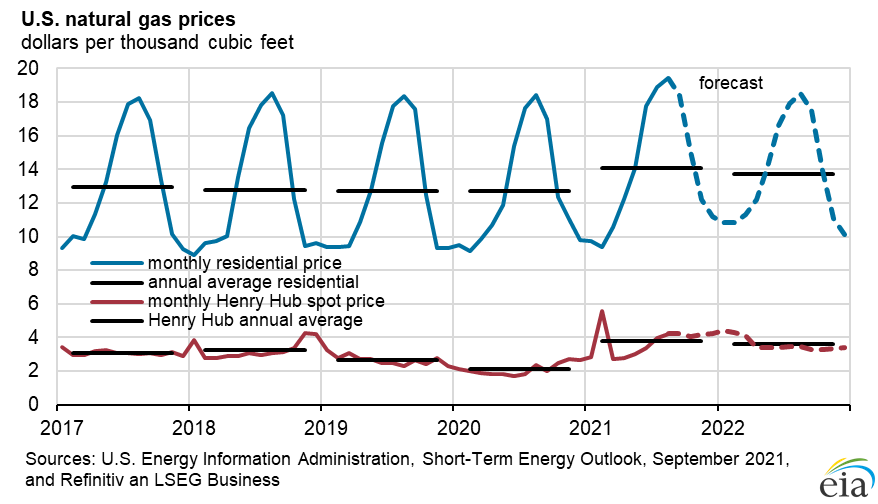

- In August, the natural gas spot price at Henry Hub averaged $4.07 per million British thermal units (MMBtu), which is up from the July average of $3.84/MMBtu. The August increase reflects hotter temperatures in August on average across the United States compared with July, which caused demand for natural gas in the electric power sector to be higher than expected. Prices rose further in late August when Hurricane Ida caused a decline in natural gas production in the GOM.

- Henry Hub spot prices in August were $1.77/MMBtu higher than in August 2020. Steadily rising natural gas prices over the past year primarily reflects: growth in liquefied natural gas (LNG) exports, rising domestic natural gas consumption for sectors other than electric power, and relatively flat natural gas production. We expect the Henry Hub spot price will average $4.00/MMBtu in 4Q21, as the factors that drove prices higher during August lessen. Forecast Henry Hub prices this winter reach a monthly average peak of $4.25/MMBtu in January and generally decline through 2022, averaging $3.47/MMBtu for the year amid rising U.S. natural gas production and slowing growth in LNG exports.

- More than 90% of natural gas production in the GOM was offline in late August following Hurricane Ida. GOM production of marketed natural gas averaged 1.9 billion cubic feet per day (Bcf/d) in August, down 0.4 Bcf/d from July. We expect that natural gas production in the GOM will gradually come back online during the first half of September and average 1.5 Bcf/d for the month before returning to an average of 2.1 Bcf/d in 4Q21.

- We expect dry natural gas production will average 92.7 Bcf/d in the United States during 2H21—up from 91.7 Bcf/d in 1H21—and then rise to 95.4 Bcf/d in 2022, driven by natural gas and crude oil prices, which we expect to remain at levels that will support enough drilling to sustain production growth.

- We expect that U.S. consumption of natural gas will average 82.5 (Bcf/d) in 2021, down 0.9% from 2020. U.S. natural gas consumption declines in 2021, in part, because electric power generators switch to coal from natural gas as a result of higher natural gas prices. In 2021, we expect residential and commercial natural gas consumption combined will rise by 1.2 Bcf/d from 2020 and industrial consumption will rise by 0.6 Bcf/d from 2020. Rising natural gas consumption in sectors other than the electric power sector results from expanding economic activity and colder winter temperatures in 2021 compared with 2020. We expect U.S. natural gas consumption will average 82.6 Bcf/d in 2022, mostly unchanged from 2021.

- We estimate that U.S. natural gas inventories ended August 2021 at about 2.9 trillion cubic feet (Tcf), which is 7% lower than the five-year (2016–20) average for this time of year. Injections into storage this summer have been below the previous five-year average, largely as a result of hot weather and high exports occurring amid relatively flat natural gas production. We forecast that inventories will end the 2021 injection season (end of October) at almost 3.6 Tcf, which would be 5% below the five-year average.