Overview and COVID-19 Apparent Demand Response

The U.S. Energy Information Administration (EIA) released its weekly data on diesel and gasoline retail prices for the week ended June 22. Retail prices for gasoline rose for the eighth consecutive week, by 3.1 cents/gallon. Diesel prices, which have not yet shown a strong rebound, rose by 2.2 cents. The COVID-19 pandemic caused severe demand destruction, which is reversing gradually. The EIA publishes weekly “product supplied” data as its proxy for demand. These data show gasoline demand crashing from 9,696 barrels per day (kbpd) during the week ended March 13 to just 5,065 kbpd during the week ended April 3, a huge hit of 4,631 kbpd in just four weeks. That was the low point. Data for the week ended June 12 show that gasoline demand has recovered to 7,870 kbpd. The EIA points out that “product supplied” is not a precise measure of demand, but these data provide the most up-to-date numbers publicly available.

Diesel demand dropped sharply in response to COVID-19, and it now is recovering in fits and starts. Diesel demand stagnated at first, but it now appears to be on an upward trend. The EIA reported that distillate fuel oil demand plunged by 1,256 kbpd between the week ended March 13 and the week ended April 10, slumping from 4,013 kbpd to 2,757 kbpd in a four-week period. Diesel demand crept back up to 3,164 kbpd by the week ended April 24. Apparent demand weakened again during the week ended May 1, dropping to 3,129 kbpd. A rebound came during the week ended May 8, bringing demand to 3,818 mmbpd. The week ended May 22 saw diesel demand drop once again to 3,266 kbpd, followed by a successive drop to 2,718 kbpd during the week ended May 29. During the week ended June 12, diesel demand popped back up to 3,555 kbpd.

Comparing the most recent weekly data available (for the week ended June) with data from the week ended March 13 (before mandatory shelter-in-place orders began to take hold,) the data show that over a 13-week period, gasoline demand has climbed back up to 81% of its March 13 level. Diesel demand has been more volatile, but it was back at 89% of its March 13 level. Diesel demand began the year at a low level, partly because the winter was one of the mildest on record. Until last week’s small stock drawdown, diesel inventories had grown for ten consecutive weeks.

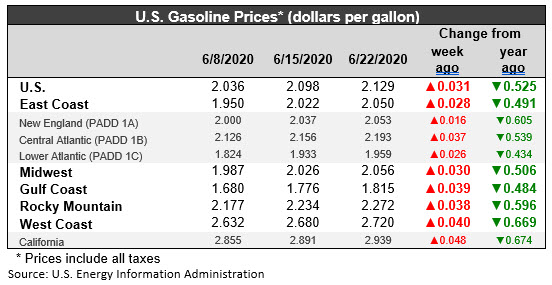

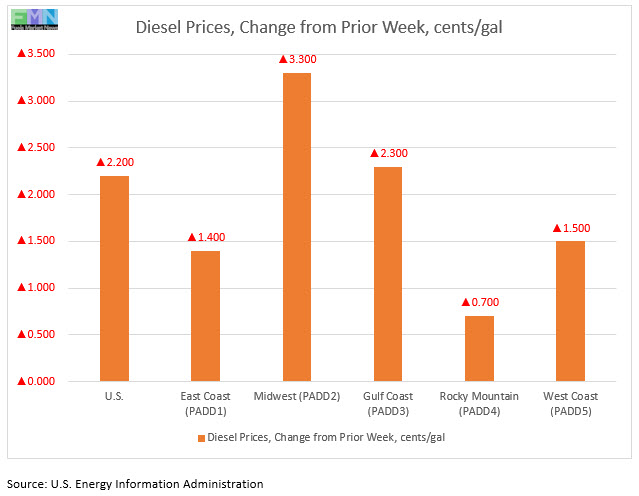

For the week ended June 22, retail prices for gasoline rose by 3.1 cents/gallon. Retail prices for diesel rose by 2.2 cents/gallon.

The national average price for gasoline was $2.129/gallon. This price was 52.5 cents/gallon below the price for the same week one year ago. In February, retail prices for gasoline were higher than they had been a year earlier. The COVID-19 pandemic caused gasoline prices to fall below $2/gallon. Now, prices in four of the five PADDs have regained the $2/gallon level. From late-November through early March, gasoline prices had been above their levels from last year. During the week ended March 2, retail gasoline prices were a mere 0.001 cent/gallon above last year’s level. The huge price declines since then have brought gasoline prices dramatically below their levels of last year.

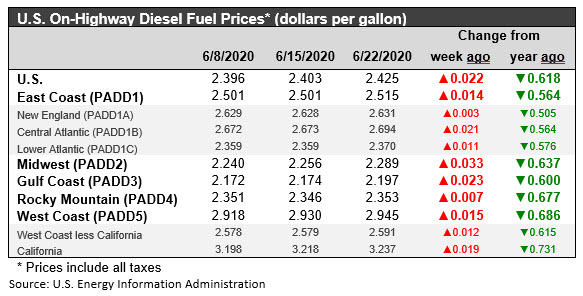

Diesel prices also had been above last year’s level, but prices are now well below these levels. On a national average basis, the retail price for diesel averaged $2.425/gallon—61.8 cents/gallon lower than the price in the same week last year. For the calendar year to date, retail prices for diesel have shed a total of 65.4 cents/gallon.

Futures Prices and Retail Price Outlook

During the week June 15 to June 19, West Texas Intermediate (WTI) crude oil futures prices bounced back by $3.00/b (8.3%), recovering the prior week’s loss of $3.15/b. WTI futures have regained the $40/b level. Last week, a worrisome acceleration of COVID-19 infections and news of the U.S. economic recession caused a market pullback. The month of May began with phased economic re-opening. Since then, however, twenty-two states have reported recent increases in coronavirus cases. The latest insight holds that this rise in infections cannot be called a “second wave” since the first wave never receded. Instead, the COVID-19 pandemic is like a “forest fire” that will burn as long as fuel is provided.

During the week of June 15 to June 19, gasoline futures prices jumped by 14.46 cents (12.9%,) more than regaining last week’s decline of 6.74 cents. Diesel futures prices rebounded strongly by 9.57 cents/gallon (8.7%,) following last week’s decline of 6.74 cents. Today, future prices look strong. While the relationship between futures prices and retail prices is not immediate or one-for-one, the strength in futures markets suggests that gasoline and diesel retail prices will rise in the coming week.

Retail Diesel Prices

The week ended June 22 brought a 2.2 cents/gallon increase in the retail price for diesel. For the year to date, diesel prices have fallen by a cumulative 65.4 cents/gallon, a major downward slump that only now seems to be reversing. In the autumn of 2019, retail diesel prices had been below the $3/gallon mark until the attacks on Saudi Arabian oil facilities in mid-September 2019. They rose at that time, and they remained above the $3/gallon mark until the week ended February 3, 2020. Prices then continued to slide. For the current week, retail diesel prices rose by 2.2 cents to arrive at an average price of $2.425/gallon. Prices rose in all PADDs. The national average price for the week was 61.8 cents/gallon below where it was during the same week last year.

In the East Coast PADD 1, diesel prices rose 1.4 cents to reach an average price of $2.515/gallon. Within PADD 1, New England prices increased by 0.3 cents to average $2.631/gallon. Central Atlantic diesel prices rose by 2.1 cents to average $2.694/gallon. Lower Atlantic prices rose by 1.1 cents to reach an average price of $2.370/gallon. PADD 1 prices were 56.4 cents/gallon below their levels for the same week last year.

In the Midwest PADD 2 market, retail diesel prices increased by 3.3 cents to average $2.289/gallon. This was the largest price increase among the PADDs. Prices were 63.7 cents below their level for the same week last year. PADD 2 joined PADD 3 during the week ended June 17, 2019, in having diesel prices fall below $3/gallon. Prices subsequently fell below $3/gallon in PADD 4 and PADD 1. Six weeks ago, PADD 5 prices also slid below the $3/gallon mark.

In the Gulf Coast PADD 3, retail diesel prices rose by 2.3 cents to average $2.197/gallon. PADD 3 continues to have the lowest diesel prices among the PADDs, currently 22.8 cents below the U.S. average. Prices were 60.0 cents below their level for the same week in the previous year.

In the Rocky Mountains PADD 4 market, retail diesel prices rose by 0.7 cents to an average price of $2.353/gallon. PADD 4 prices were 67.7 cents lower than for the same week in the prior year.

In the West Coast PADD 5 market, retail diesel prices rose by 1.5 cents to average $2.945/gallon. PADD 5 prices were 68.6 cents below their level from last year. Until December 2019, PADD 5 had been the only district where diesel prices were higher than they were in the same week last year. Subsequently, prices rose until this was true in all other PADDs. Prices have fallen dramatically, and the national average price is now well below its level of last year. PADD 5 prices excluding California increased by 1.2 cents to average $2.591/gallon. This price was 61.5 cents below the retail price for the same week last year. California diesel prices rose by 1.9 cents to reach an average price of $3.237/gallon. Until the week ended June 24, 2019, California had been the only major market where diesel prices were above $4/gallon, where they had been for nine weeks. California prices retreated below $4/gallon from July through October, rose above $4/gallon again during the first three weeks of November, and declined since then until just the past three weeks. California diesel prices were 73.1 cents lower than they were at the same week last year.

Retail Gasoline Prices

The COVID-19 pandemic is having a massive impact on the U.S. gasoline market. With the phased re-opening of the economy, demand is rising as are prices. During the week ended June 8, U.S. retail gasoline prices finally regained the $2/gallon threshold, after falling below this level during the week ended April 6 and remaining there for the next nine weeks. During the current week ended June 22, average retail prices for gasoline rose by 3.1 cents/gallon to average $2.129/gallon. Prices rose in all PADDs. Retail gasoline prices for the current week were 52.5 cents per gallon lower than they were one year ago. Until November, gasoline prices had been below their levels of last year. Prices then rose to surpass last year’s levels in all PADDs. The downhill price slide changed this, making gasoline a bargain. Until the pandemic, it had been over four years since the average retail price for gasoline was below the $2/gallon mark.

Looking back at historic prices, gasoline prices hit a peak of $2.903/gallon during the week ended October 8, 2018. Prices then slid downward for 14 weeks in a row, shedding a total of 66.6 cents per gallon. In the next 17 weeks, prices marched back up by 66 cents/gallon. Prices came very close to the peak they hit in early October 2018. However, the months of May and the June 2019 brought an easing of prices amounting to 23.3 cents per gallon. The week ended July 1 reversed that downward trend and sent prices up once again. The COVID-19 pandemic caused a price collapse, but prices began to recover in May.

For the current week ended June 22, East Coast PADD 1 gasoline retail prices rose by 2.8 cents to arrive at an average of $2.050/gallon. This week’s average price was 49.1 cents/gallon below where it was during the same week last year. Within PADD 1, New England prices increased by 1.6 cents to average $2.053/gallon. Central Atlantic market prices rose by 3.7 cents, reaching an average of $2.193/gallon. Prices in the Lower Atlantic market rose by 2.6 cents to average $1.959/gallon.

In the Midwest PADD 2 market, retail gasoline prices rose by 3.0 cents to average $2.056/gallon. PADD 2 prices for the week were 50.6 cents/gallon lower than they were for the same week last year.

In the Gulf Coast PADD 3 market, gasoline prices rose by 3.9 cents to average $1.85/gallon. During the week ended March 16, PADD 3 was the first region where retail prices fell below the $2/gallon level. It was joined subsequently by PADD 2, then by PADD 1, and then by PADD 4. Currently, PADD 3 remains the only PADD where prices are still below $2/gallon. PADD 3 usually has the lowest average prices among the PADDs. PADD 3 prices for the week were 48.4 cents/gallon lower than for the same week last year.

In the Rocky Mountains PADD 4 market, gasoline pump prices increased by 3.8 cents, reaching an average price of $2.272/gallon. This week’s PADD 4 prices were 59.6 cents/gallon lower than at the same time last year.

In the West Coast PADD 5 market, retail gasoline prices rose by 4.0 cents to average $2.720/gallon. This was the largest price hike among the PADDs. PADD 5 typically has the highest retail prices for gasoline, and until mid-March it had been the only PADD where retail gasoline prices stayed above $3/gallon. Prices this week were 67.4 cents/gallon lower than last year’s price. Prices excluding California rose by 3.2 cents to average $2.460/gallon, which was 66.1 cents/gallon below last year’s price. California prices rose by 4.8 cents to average $2.939/gallon. California had been the last state where gasoline prices had remained above the $3/gallon line, but this changed the week ended March 30. On Thursday March 19, California led the U.S. by taking the dramatic step of ordering a statewide shelter-in-place to combat the spread of COVID-19. This order affected approximately 40 million people, and it caused a dramatic contraction in fuel demand. California retail gasoline prices were 67.4 cents per gallon below their levels from the same week last year.