Exclusive Analysis by Dr. Nancy Yamaguchi

West Texas Intermediate (WTI) crude oil futures prices fell below $41 a barrel this week and are hovering just under $40.50 a barrel. Most of Wall Street slid yesterday, but massive earnings by the tech giants buoyed the market overall. The combined market value of Amazon, Apple, Alphabet and Facebook surged by $250 billion. These companies now account for around one fifth of the S&P 500. The COVID-19 pandemic is giving markets a split personality. Companies that help people and businesses shift toward life online are flourishing. Conversely, companies that depend on conventional consumption and activity are languishing. Energy and banking have been hit hard.

Throughout the month, WTI crude has traded at prices usually within a one-dollar range above and below $40 a barrel. Prices have found at least a temporary equilibrium in the $39-$41 a barrel range. Last week, however, prices were at the high end of the range, with some high trades at over $42 a barrel. This week, oil prices are declining, with lows yesterday falling below $39 a barrel before beginning to climb back. Concern remains that the U.S., and many other countries, will face a second wave of economic damage persisting for an unknown length of time. Oil prices appear to be headed for a finish in the red this week, though crude oil futures are supported more than product prices.

The Federal Open Market Committee (FOMC) held a regularly scheduled meeting this week. Decisions about interest rates are made by the FOMC at its regularly scheduled meetings, of which there are eight per year. Because of the COVID-19 pandemic and the economic recession, the FOMC already has held two unscheduled meetings this year. The Fed has repeatedly calmed the market by stating that it will employ all of its tools to support the economic recovery. As expected from this week’s regularly scheduled meeting, the FOMC kept the interest rate flat.

Hopes for a rapid economic recovery were set back again this week when statistics revealed that initial unemployment claims are rising again rather than falling. The Department of Labor reported that 1,434,000 people filed initial unemployment claims during the week ended July 25, an increase of 12,000 from the prior week’s upward-revised level of 1,422,000. This was the second week in a row with an increase. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for the next 15 weeks. There were hopes that weekly jobless claims would fall below one million this month. Unfortunately, the relentless increase in COVID-19 infections is shutting some economic activities down again. During the 19 weeks since U.S. states began to issue shelter-in-place orders, 56.6 million Americans have filed initial jobless claims.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have surpassed 17 million. Global cases have risen to 17,325,093, with 673,868 deaths. Confirmed cases in the U.S. have risen to 4,495,375. U.S. deaths attributed to the disease have reached 152,075. According to the COVID Tracking Project, the seven-day week from July 24 through July 30 brought an average of 63,870 new confirmed cases each day, and an average death toll of 1,095 per day.

Note that crude and product inventory data this month may be complicated by stormy weather, which can have impacts all along the supply chain for fuel. Hurricane Hanna was the first Atlantic hurricane to make landfall in Texas, on Padre Island, since Hurricane Dolly in 2008. Disaster response was complicated by the COVID-19 pandemic. Offshore oil production and refinery operations were largely unaffected. Tropical Storm Isaias has been upgraded to Hurricane Isaias and currently is approaching Florida. Inventory drawdowns typically boost oil prices.

WTI crude futures prices opened at $40.34 a barrel today, down by $0.72 a barrel (1.8%) from last Friday’s open of $41.06 a barrel. Today, prices are under pressure, though they have recovered from yesterday’s lows. Oil prices may end the week in the red. Our weekly price review covers hourly forward prices from Friday, July 24 through Friday, July 31. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

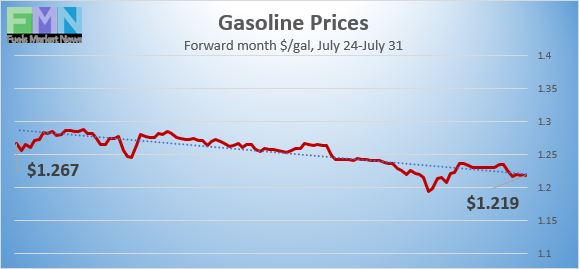

Gasoline Prices

Gasoline Prices

Gasoline futures prices opened at $1.237 per gallon today on the NYMEX, compared with $1.263/gallon on Friday, July 24. This was a loss of 2.6 cents (2.1%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline retreated by 1.1 cents/gallon during the week ended July 27. Seven weeks ago, retail prices reclaimed the territory above $2 per gallon. Retail prices averaged $2.175/gallon at the national level. Gasoline futures prices have a downward tilt today, trading in the range of $1.21/gallon to $1.24/gallon. Contracts are moving to the next forward month. The week appears to be heading for a finish in the red. The latest price is $1.2186/gallon.

Source: Prices as reported by DTN Instant Market

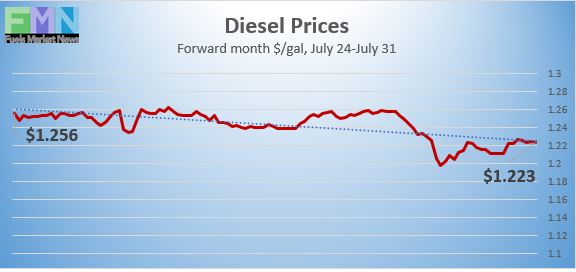

Diesel Prices

Diesel Prices

Diesel opened on the NYMEX today at $1.2235/gallon, down by 3.41 cents, or 2.7%, from last Friday’s open of $1.2576/gallon. U.S. average retail prices for diesel eased by 0.6 cents per gallon during the week ended July 27 to average $2.427/gallon. Diesel prices generally have weakened this year, missing some of the price recovery seen in crude and gasoline markets. Diesel futures prices today are roughly flat, and prices appear to be heading for a finish in the red. Contracts are moving to the next forward month. Currently, diesel is trading in the range of $1.21-$1.23/gallon. The latest price is $1.2232/gallon.

Source: Prices as reported by DTN Instant Market

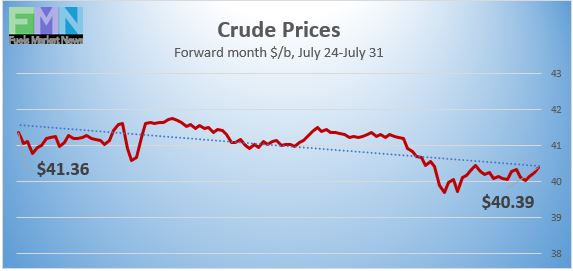

WTI Crude Prices

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $40.34 a barrel, compared with $41.06 a barrel last Friday. This was a loss of $0.72 a barrel (1.8%.) The week began with WTI prices above the $41 a barrel level, but the COVID-19 crisis is viewed as getting worse. Initial unemployment claims rose for the second week in a row, while just a few weeks ago they were on a downward trend. Congress and the White House have not agreed upon the next U.S. economic stimulus bill. WTI crude is struggling to remain above $40 a barrel, trading in the $40.00–$40.50 a barrel range currently. The latest price is $40.42 a barrel.

Source: Prices as reported by DTN Instant Market

PRICE MOVERS THIS WEEK: BRIEFING

WTI crude oil futures prices fell below $41 a barrel this week and are hovering just under $40.50 a barrel. Most of Wall Street slid yesterday, but massive earnings by the tech giants buoyed the market overall. The combined market value of Amazon, Apple, Alphabet and Facebook surged by $250 billion. These companies now account for around one fifth of the S&P 500. The COVID-19 pandemic is giving markets a split personality. Strong performances are being turned in from companies that help people shift toward staying connected and conducting more business and daily life online. Conversely, companies that depend on conventional consumption and activity are languishing. Energy and banking have been hit hard.

Throughout the month, WTI crude has traded at prices usually within a one-dollar range above and below $40 a barrel. The supply and demand equation has many moving parts, and prices have found at least a temporary equilibrium in the $39-$41 a barrel range. Last week, however, prices were at the high end of the range, with some high trades at over $42 a barrel. This week, oil prices are declining, with lows falling below $39 a barrel. Concern remains that the U.S. will face a second wave of economic damage persisting for an unknown length of time. Oil prices appear to be headed for a finish in the red this week, though crude oil futures are supported more than product prices.

The Federal Open Market Committee (FOMC) met this week on July 28 and 29. The FOMC is the branch of the Federal Reserve Board that sets the direction of national monetary policy. Decisions about interest rates are made by the FOMC at its regularly scheduled meetings. The Committee holds eight regularly scheduled meetings annually, and it may hold unscheduled meetings as necessary. Because of the COVID-19 pandemic and the economic recession, the FOMC already has held two unscheduled meetings this year. The Fed has repeatedly calmed the market by stating that it will employ all of its tools to support the economic recovery. As expected from this week’s regularly scheduled meeting, the FOMC kept the interest rate flat. As summarized in its official statement:

The path of the economy will depend significantly on the course of the virus. The ongoing public health crisis will weigh heavily on economic activity, employment and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.

Hopes for a rapid economic recovery were set back again this week when statistics revealed that initial unemployment claims are rising again rather than falling. The Department of Labor reported that 1,434,000 people filed initial unemployment claims during the week ended July 25, an increase of 12,000 from the prior week’s upward-revised level of 1,422,000. This was the second week in a row with an increase. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for the next 15 weeks. There were hopes that weekly jobless claims would fall below one million this month. Unfortunately, the relentless increase in COVID-19 infections is shutting some economic activities down again. During the 19 weeks since U.S. states began to issue shelter-in-place orders, 56.6 million Americans have filed initial jobless claims.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have surpassed 17 million. Global cases have risen to 17,325,093, with 673,868 deaths. Confirmed cases in the U.S. have risen to 4,495,375. U.S. deaths attributed to the disease have reached 152,075. According to the COVID Tracking Project, the seven-day week from July 24 through July 30 brought an average of 63,870 new confirmed cases each day, and an average death toll of 1,095 per day.

Note that crude and product inventory data this month may be complicated by stormy weather, which can have impacts all along the supply chain for fuel. Hurricane Hanna was the first Atlantic hurricane to make landfall in Texas, on Padre Island, since Hurricane Dolly in 2008. Disaster response was complicated by the COVID-19 pandemic. Offshore oil production and refinery operations were largely unaffected. Tropical Storm Isaias has been upgraded to Hurricane Isaias, and it currently is approaching Florida. Inventory drawdowns typically boost oil prices.

The American Petroleum Institute (API) released information on Tuesday showing a significant drawdown from crude oil inventories. According to the API, 6.829 mmbbls of crude was drawn from stockpiles. This was partly counteracted by additions of 1.083 mmbbls of gasoline and 0.187 mmbbls of diesel. The API’s net drain on inventories was 5.559 mmbbls. Market analysts had predicted small drawdowns from crude and gasoline inventories plus an addition to diesel inventories.

The U.S. Energy Information Administration (EIA) published official inventory data on Wednesday. The EIA statistics showed a major drawdown of 10.611 mmbbls from crude oil inventories. This was the largest crude drawdown all year. There were relatively small additions to product inventories: 0.503 mmbbls of diesel and 0.654 mmbbls of gasoline. The EIA net result was a large inventory drawdown of 9.454 mmbbls. Crude oil inventories have expanded in 21 of the 29 weeks since the first week of January, sending a total of 99.01 mmbbls of crude oil into storage.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26, but the downward trend was reversed during the past four weeks, and Cushing stocks are back up to 51,421 mmbbls.

U.S. crude production remained stable at 11.1 mmbpd during the week ended July 24, according to the EIA. U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production during the first four weeks of July rose to an average of 11.05 mmbpd.