Growing Crude Oil Production Enhances U.S. National Security

- Downtrends in crude oil and gasoline remain in force, distillate prices more neutral

- Crude oil production tops 12 million barrels daily

- Domestic shale oil output gains add to U.S. oil self-sufficiency

- Stratospheric European natural gas prices re-aligning economic relationships

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

The downtrend in crude oil remains in place since the highs of early June. The Federal Reserve’s clearly signalled intention to reduce aggregate U.S. demand in order to combat inflation has been taken by the market as a strong indicator of lower future demand for crude oil. Gasoline prices largely mirror the trend in crude oil. Distillate futures prices are currently tracing a more muddled pattern as the concerns of a slowing economy are being offset by very low inventory levels on a worldwide basis

In 2021, the United States imported about 8.47 million barrels per day (b/d) of petroleum. Petroleum includes crude oil, hydrocarbon gas liquids (HGLs), refined petroleum products such as gasoline and diesel fuel, and biofuels. During the same year, the U.S. exported about 8.63 million b/d of petroleum to the global market. The resulting total net petroleum imports (imports minus exports) were about -0.16 million b/d in 2021, which means that the United States was a net petroleum exporter of 0.16 million b/d in 2021.

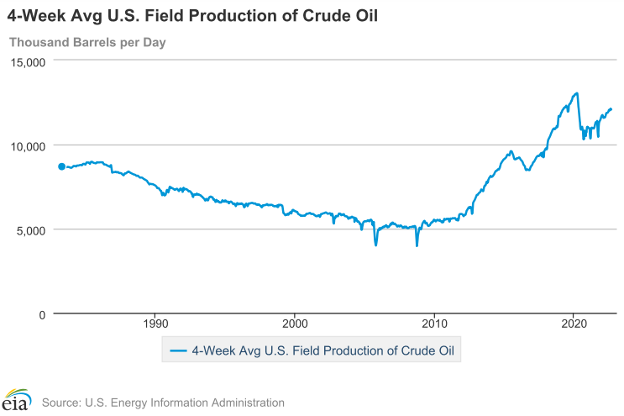

This dramatic change from the 1970’s OPEC oil embargo and the fears of being energy-dependent on other countries was made possible, of course, by the shale revolution and the subsequent repeal of the ban on U.S. crude oil exports. The graph below is a stark reminder of the massive change in scale of U.S. crude oil production. With domestic daily production levels now back over 12 million barrels per day, a return to the pre-Covid highwater mark certainly looks possible.

While Russia may be able to find new buyers for the crude it can no longer sell to the West, it is highly uncertain if they will be able to increase their own production levels while still under stringent economic sanctions. Saudi Arabia has long played the role of the key swing producer. Will they cede this role to the United States as the continuing advances in shale technology allow the U.S. to maintain such high levels of production?

Supply/Demand Balances

Supply/demand data in the United States for the week ended September 9, 2022, were released by the Energy Information Administration.

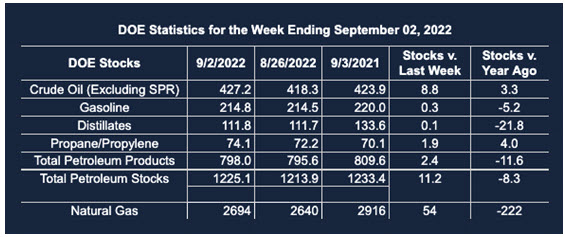

Total commercial stocks of petroleum rose 11.2 million barrels during the week ended September 2, 2022.

Commercial crude oil supplies in the United States increased by 8.8 million barrels from the previous report week to 427.2 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.7 million barrels to 6.9 million barrels

PADD 2: Down 0.6 million barrels to 107.2 million barrels

PADD 3: Plus 9.9 million barrels to 241.3 million barrels

PADD 4: Plus 0.5 million barrels to 22.8 million barrels

PADD 5: Down 0.1 million barrels to 49.0 million barrels

Cushing, Oklahoma, inventories were down 0.5 million barrels from the previous report week to 24.8 million barrels.

Domestic crude oil production was up UNCH barrels per day from the previous report week at 12.1 million barrels daily.

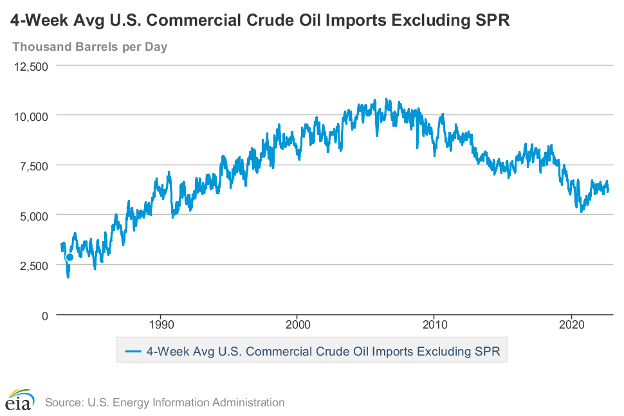

Crude oil imports averaged 6.779 million barrels per day, a daily increase of 824,000 barrels. Exports decreased 534,000 barrels daily to 3.433 million barrels per day.

Refineries used 90.9% of capacity; 1.8 percentage points lower than the previous report week.

Crude oil inputs to refineries decreased 309,000 barrels daily; there were 15.929 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 319,000 barrels daily to 16.309 million barrels daily.

Total petroleum product inventories rose by 3.4 million barrels from the previous report week, rising to 799.0 million barrels.

Total product demand decreased 181,000 barrels daily to 19.892 million barrels per day.

Gasoline stocks increased 0.3 million barrels from the previous report week; total stocks are 214.8 million barrels.

Demand for gasoline rose 136,000 barrels per day to 8.727 million barrels per day.

Distillate fuel oil stocks increased 0.1 million barrels from the previous report week; distillate stocks are at 111.8 million barrels. EIA reported national distillate demand at 3.624 million barrels per day during the report week, an increase of 58,000 barrels daily.

Propane stocks were increased by 1.9 million barrels from the previous report week to 74.1 million barrels. The report estimated current demand at 1,070,000 barrels per day, an increase of 423,000 barrels daily from the previous report week.

Natural Gas

Russia and China have agreed to build a pipeline carrying natural gas from Siberia to China. This gas would previously have gone to Europe. It is a response to efforts to isolate Russia from European markets because of the Ukrainian invasion.

An American bank has raised its forecast for natural gas prices through 2025. Things like the re-direction of Siberian natural gas and ongoing political tensions are likely to starve European markets for some time. Last week, WEMS also noted the increasingly perilous situation for hydropower and nuclear power generation in the EU.

The bank projects prices at the Netherlands Title Transfer Facility to average $65 per MMBtu in the fourth quarter and $53 per MMBtu next year. (Prices are expected to retreat in 2024 and 2025.)

According to the EIA:

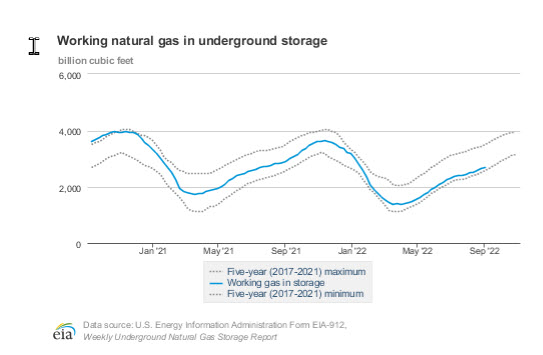

Net injections [of natural gas] into storage totaled 54 Bcf for the week ending September 2, compared with the five-year (2017–2021) average net injections of 65 Bcf and last year’s net injections of 48 Bcf during the same week. Working natural gas stocks totaled 2,694 Bcf, which is 349 Bcf (11%) lower than the five-year average and 222 Bcf (8%) lower than last year at this time.

3The average rate of injections into storage is 5% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.2 Bcf/d for the remainder of the refill season, the total inventory would be 3,296 Bcf on October 31, which is 349 Bcf lower than the five-year average of 3,645 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2022 Powerhouse Brokerage, LLC, All rights reserved