Tight Supply Supports Oil Prices

- ULSD futures break resistance

- Shut-in production remains in the Gulf of Mexico

- ULSD supplies are notably short

- Overseas natural gas demand grows dramatically

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Oil prices continued their upward climb. ULSD prices tore through resistance, settling around $2.27 as the week of September 24 ended. Next resistance may be found at $2.32. Major resistance follows at $2.45, last seen in October 2018.

WTI crude oil futures reached a new high at $74.27 last week. Next resistance is at $77. The strength of crude oil prices reflects tight inventories, in part reflecting the production shut-ins and reduced refinery activity of Hurricane Ida.

There remains shut-in production according to the BSEE. The most recent data show 294,000 barrels of oil, 16.2% of Gulf output. Natural gas production is still short 24.3% of output.

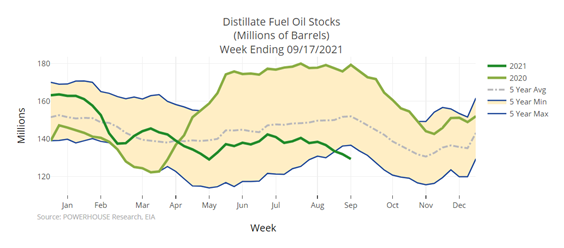

Slim supply is especially problematic for ULSD. Stocks of ULSD have been moving below the low of the past five-year minimum for several weeks. And with the change of seasons, temperatures are falling 10 to 20 degrees as an autumn front sweeps the country.

Distillate Fuel Oil Stocks 2015 – 2021 Source: EIA, Powerhouse

Several economic situations are contributing to the current supply constraint. The U.S. is down approximately one million barrels per day of refining capacity due to pandemic-related closures. Oil producers are subject to the same labor, trucking and material shortages plaguing supply chains globally. Air travel is finally showing signs of life, now only down 7.7% from this time in 2019.

Gasoline demand is following traditional autumnal patterns, falling as summer driving fades into the past. Gasoline inventories traditionally bottom out in late October. (In the next several weeks, Powerhouse will start to evaluate the “gas crack spread,” an important measure of profitability for the refiner and an indicator of profitably for the retailer.)

Supply/Demand Balances

Supply/demand data in the United States for the week ended Sept. 17, 2021, were released by the Energy Information Administration.

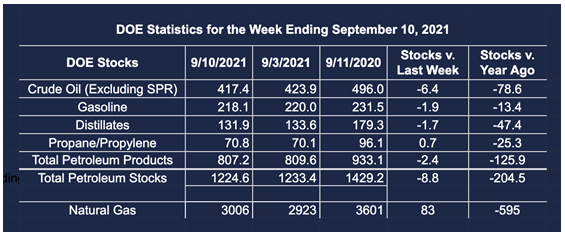

Total commercial stocks of petroleum fell 2.6 million barrels during the week ended Sept. 17, 2021.

Commercial crude oil supplies in the United States decreased by 3.5 million barrels from the previous report week to 414 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down at 0.1 million barrels to 8 million barrels

PADD 2: Down 2.8 million barrels to 111.1 million barrels

PADD 3: Down 0.3 million barrels to 223.9 million barrels

PADD 4: Unchanged at 23.4 million barrels

PADD 5: Down 0.4 million barrels to 47.5 million barrels

Cushing, Oklahoma, inventories were down 1.5 million barrels from the previous report week to 33.8 million barrels.

Domestic crude oil production was up 500,000 barrels per day from the previous report week to 10.6 million barrels daily.

Crude oil imports averaged 6.465 million barrels per day, a daily increase of 704,000 barrels. Exports increased 185,000 barrels daily to 2.809 million barrels per day.

Refineries used 87.5% of capacity; 5.4 percentage points higher from the previous report week.

Crude oil inputs to refineries increased 960,000 barrels daily; there were 15.347 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 977,000 barrels daily to 15.863 million barrels daily.

Refineries used 87.5% of capacity; 5.4 percentage points higher from the previous report week.

Crude oil inputs to refineries increased 960,000 barrels daily; there were 15.347 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 977,000 barrels daily to 15.863 million barrels daily.

Total petroleum product inventories increased 0.9 million barrels from the previous report week.

Gasoline stocks increased 3.5 million barrels from the previous report week; total stocks are 221.6 million barrels.

Demand for gasoline rose 4,000 barrels per day to 8.896 million barrels per day.

Total product demand increased 1.234 million barrels daily to 21.145 million barrels per day.

Distillate fuel oil stocks fell 2.6 million barrels from the previous report week; distillate stocks are at 129.3 million barrels. EIA reported national distillate demand at 4.424 million barrels per day during the report week, an increase of 628,000 barrels daily.

Propane stocks fell 0.5 million barrels from the previous report week; propane stocks are at 70.3 million barrels. The report estimated current demand at 1.293 million barrels per day, an increase of 404,000 barrels daily from the previous report week.

Natural Gas

Natural gas futures have been one of the volatility stars of the 21st century. They traded as low as $1.76 in 2001, reaching their record high of $15.78 in December 2005. Over the next several years, prices slowly retreated to their earlier lows, bottoming at $1.43 in June 2020. Last week, spot natural gas futures held at $5.00.

This level reflected massive growth in overseas demand that the United States has been working to meet. The country has become a net exporter of natural gas but still faces barriers with liquefaction and adequate LNG shipping to support export demand. New resistance can be found at $6.50, last seen in February 2014.

According to the EIA:

Net [natural gas] injections into storage totaled 76 Bcf for the week ended September 17, compared with the five-year (2016–2020) average net injections of 74 Bcf and last year’s net injections of 70 Bcf during the same week. Working natural gas stocks totaled 3,082 Bcf, which is 229 Bcf lower than the five-year average and 589 Bcf lower than last year at this time.

The average rate of injections into storage is 13% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 9.3 Bcf/d for the remainder of the refill season, the total inventory would be 3,490 Bcf on October 31, which is 229 Bcf lower than the five-year average of 3,719 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved