National Uncertainties Slow Oil Market Reactions

- Market activity slows as President’s Covid-19 raises fears

- All oil futures hold support

- Higher prices must overcome bearish fundamentals

- Natural gas faces a 31 cent price gap

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Powerhouse noted last week that volatility could remain abated through the national election, “jump at Election Day and remain high thereafter.” It didn’t take long for that idea to be tested.

News that the President contracted Covid-19 reached the markets on Friday, October 2. The reaction of oil futures was tepid. Prices of WTI crude oil ended the week of Oct. 2, 2020 at $37.05 for a weekly loss of $3.20. (Friday’s loss on the day was down $1.71.)

Product price declines were constrained too. ULSD had a weekly and Friday loss of $0.0410. RBOB’s record is similar, a weekly loss of $0.0907, and within that a Friday decline of $0.0334.

Daily trading volume for WTI was about 811,000 trades on Friday. ULSD traded 176,000 times and RBOB futures changed hands 164,000 times. None of this was unusual.

The most important observation of market activity on Friday was that none of the core oil market futures broke support. Moreover, none of the futures settled the day at the lows. Price support for WTI crude oil remains untested at $36.13. Support for RBOB is at $1.0755, and ULSD finds support at $1.0605.

At writing the President’s physical situation is not clear. Were it not for this, oil prices appeared ready to pierce support and move lower.

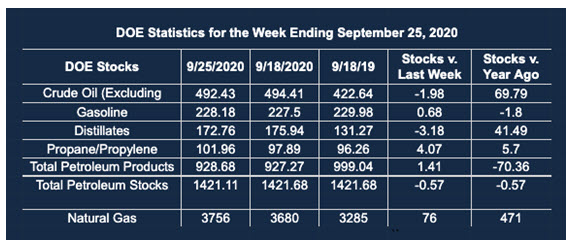

Supply and demand data for the United States have been trending down recently. EIA reported total product demand for the week ending September 25 at 17.4 million barrels, a week-on-week drop of nearly one million barrels per day.

Last year at the comparable week, demand was cruising along at 20.8 million daily barrels. The 3.3 million barrel-per-day decline in demand has been felt among all products. Jet fuel itself lost over 900,000 barrels per day. Other Oils lost 1.1 million barrels daily.

Markets operate more smoothly in calm circumstances. Uncertainty is an invitation to delay action. The CME reminds us that the oil markets are operating with new layers of uncertainty. These include (i) consumer spending in the transportation sector 45 percent below the pre-pandemic level, (ii) Airline traffic at 70% below normal, (iii) Uncertainty on how Covid-19 courses through the global economy and (iv) high levels of diesel and heating oil supplies.

Supply/Demand Balances

Supply/demand data in the United States for the week ended Sept. 25, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 0.6 million barrels during the week ended Sept. 25, 2020.

Commercial crude oil supplies in the United States decreased by 2.0 million barrels from the previous report week to 492.4 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Fell 0.3 million barrels to 10.7 million barrels

PADD 2: Plus 2.8 million barrels to 143.3 million barrels

PADD 3: Fell 1.5 million barrels to 263.5 million barrels

PADD 4: Fell 0.4 million barrels to 23.1 million barrels

PADD 5: Fell 2.5 million barrels to 51.8 million barrels

Cushing, Oklahoma inventories were up 1.8 million barrels from the previous report week to 56.1 million barrels.

Domestic crude oil production was unchanged from the previous report week at 10.7 million barrels daily.

Crude oil imports averaged 5.122 million barrels per day, a daily decrease of 45,000 barrels. Exports increased 490,000 barrels daily to 3.512 million barrels per day.

Refineries used 75.8% of capacity, up 1.0% from the previous report week.

Crude oil inputs to refineries increased 300,000 barrels daily; there were 13.670 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 188,000 barrels daily to reach 14.119 million barrels daily.

Total petroleum product inventories rose 1.4 million barrels from the previous report week.

Gasoline stocks increased 0.7 million barrels daily from the previous report week; total stocks are 228.2 million barrels.

Demand for gasoline rose 14,000 barrels per day to 8.529 million barrels per day.

Total product demand decreased 992,000 barrels daily to 17.447 million barrels per day.

Distillate fuel oil stocks decreased 3.2 million barrels from the previous report week; distillate stocks are at 172.8 million barrels. EIA reported national distillate demand at 3.655 million barrels per day during the report week, a decrease of 304,000 barrels daily.

Propane stocks increased 4.1 million barrels from the previous report week; propane stocks are 102.0 million barrels. The report estimated current demand at 615,000 barrels per day, a decrease of 434,000 barrels daily from the previous report week.

Natural Gas

Winter natural gas futures opened with the November contract at $2.769. The price could not sustain so intense a jump from October’s expiration price of $2.101. The contract ended the first day as spot at $2.561. Market action has left a $0.31 gap that has been only minimally filled.

According to the EIA:

The net injections [of natural gas] into storage totaled 76 Bcf for the week ending September 25, compared with the five-year (2015–19) average net injections of 78 Bcf and last year’s net injections of 109 Bcf during the same week. Working natural gas stocks totaled 3,756 Bcf, which is 405 Bcf more than the five-year average and 471 Bcf more than last year at this time.

The average rate of injections into storage is 6% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.3 Bcf/d for the remainder of the refill season, the total inventory would be 4,128 Bcf on October 31, which is 405 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2020 Powerhouse Brokerage, LLC, All rights reserved