The Rally in Oil Prices Is Intact

- ULSD price gap on roll to December contract is half-recovered

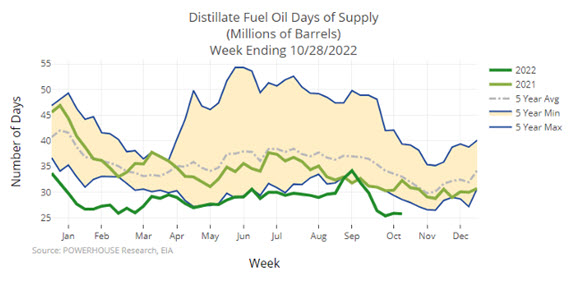

- Fewer than 27 days of ULSD supply available

- Mixed data on broader economy challenge expectations

- Natural gas futures move above $6.00

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

Oil prices advanced last week. This was especially important for ULSD; November futures expired at $4.19 on October 31. The December contract became spot, causing an immediate loss of $0.51 in value.

Underlying market prices, however, a significant shortfall in distillate fuel oil supply pressured prices higher. ULSD settled at $3.9150 at week’s end, more than half of the change-of-contract loss.

Tight distillate fuel oil stocks can be seen in data on Days of Supply. A small improvement noted in last week’s Weekly Energy Market Situation was reversed as inventories gained only 400,000 thousand barrels and demand grew 2.6 million barrels, reflecting growth in winter heating demand. Cumulative Heating Degree Days in populous areas of the Northeast are developing more rapidly than last year. The Middle Atlantic states are already 103 HDDs higher than last year at this time, (+48 HDDs for the country overall.)

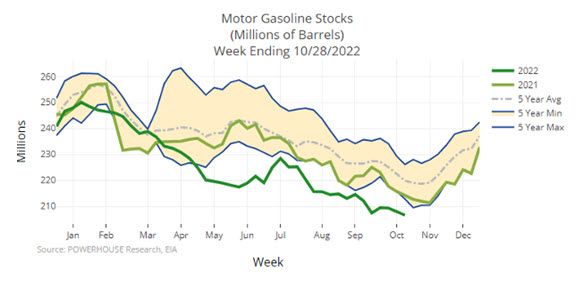

The situation in gasoline is only marginally better. Inventories fell 1.3 million barrels last week. They continue to move below the average of the past five years. The market is within sight of an annual turn in stocks. Facilities should be returning from turnaround, developing supply for next spring.

RBOB spot futures followed ULSD with a substantial loss in value as the December future contract became spot. The November/December roll saw a loss of $0.2950. Prices recovered nearly $0.22 of that by week’s end.

Last week’s action suggests that the bullish petroleum product situation reported here remains in place.

Contradictions in the overall economy present a major BUT in our analysis. Output recovered after two down quarters, and employment remains strong. BUT inflation remains high and efforts by the Federal Reserve have not yet been able to bring it under control. Bottlenecks in the supply chain may be easing, BUT they remain an issue for manufacturers and distributors. Ironically, inventories of consumer goods are growing. Housing markets are under water BUT consumer spended continues apace.

This collection of contradictions is so enmeshed that it seems impossible to draw a solid conclusion as to the economy’s direction. We seem at present to be dragging ourselves along, BUT a recession cannot be excluded. Perhaps this week’s mid-term elections will temper rhetoric, lower the temperature or even offer a new direction for the economy. Maybe not.

Stay tuned, plan as if life were normal. Consider buying options as defined cost, limited risk instruments for cap programs.

Supply/Demand Balances

Supply/demand data in the United States for the week ended October 28, 2022, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell (⬇) 0.7 million barrels to 1.224 billion barrels during the week ended October 28, 2022.

Commercial crude oil supplies in the United States decreased (⬇) by 3.1 million barrels from the previous report week to 436.8 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down (⬇) 0.3 million barrels to 7.6 million barrels

PADD 2: Plus (⬆) 2.1 million barrels to 112.4 million barrels

PADD 3: Down (⬇) 3.5 million barrels to 246.0 million barrels

PADD 4: Down (⬇) 0.2 million barrels to 23.2 million barrels

PADD 5: Down (⬇) 1.3 million barrels to 47.5 million barrels

Cushing, Oklahoma inventories were up (⬆) 1.3 million barrels from the previous report week to 28.2 million barrels.

Domestic crude oil production was down (⬇) from the previous report week at 11.9 million barrels daily.

Crude oil imports averaged 6.205 million barrels per day, a daily increase (⬆) of 25,000 barrels. Exports decreased (⬇) 1.204 million barrels daily to 3.925 million barrels per day.

Refineries used 90.6% of capacity; 1.7 percentage points higher (⬆) than the previous report week.

Crude oil inputs to refineries increased (⬆) 406,000 barrels daily; there were 15.842 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose (⬆) 301,000 barrels daily to 16.266 million barrels daily.

Total petroleum product inventories rose (⬆) by 2.4 million barrels from the previous report week, rising to 787.3 million barrels.

Total product demand decreased (⬇) 106,000 barrels daily to 20.481 million barrels per day.

Gasoline stocks decreased (⬇) 1.3 million barrels from the previous report week; total stocks are 206.6 million barrels.

Demand for gasoline decreased (⬇) 271,000 barrels per day to 8.660 million barrels per day.

Distillate fuel oil stocks increased (⬆) 0.4 million barrels from the previous report week; distillate stocks are at 106.8 million barrels. EIA reported national distillate demand at 4.257 million barrels per day during the report week, an increase (⬆) of 379,000 barrels daily.

Propane stocks increased (⬆) by 1.2 million barrels from the previous report week to 88.1 million barrels. The report estimated current demand at 1.034 million barrels per day, an increase (⬆) of 314,000 barrels daily from the previous report week.

Natural Gas

The United States injected 107 Bcf of natural gas into storage during the last full week of October. Withdrawal season starts with 3.5 Tcf of natural gas, modestly higher than expectations.Prices ended last week at $6.40 per MMBtus. This was a new high for the rally that began at $4.75 on October 24. Upside pressure reflected renewed exports of LNG from Cove Point, Maryland, prospects for a rail workers strike in November, and lower water levels on the Mississippi river. The river situation could inhibit coal deliveries, fueling a move to natural gas to power utilities.It is also uncertain when LNG exports from Freeport, Louisiana will resume. FERC has put its restart on hold, pending receipt of more information.The weekly close above $6.00 puts next resistance at $6.74 and then $7.22.

According to the EIA:

Net injections into storage totaled 107 Bcf for the week ended October 28, compared with the five-year (2017–2021) average net injections of 45 Bcf and last year’s net injections of 66 Bcf during the same week. Working natural gas stocks totaled 3,501 Bcf, which is 135 Bcf (4%) lower than the five-year average and 101 Bcf (3%) lower than last year at this time.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2022 Powerhouse Brokerage, LLC, All rights reserved