Long-Term Oil Planning: Shifting From Supply to Demand

- Oil industry expects global demand to peak by 2040

- Electric cars will cut fuel demand by only 1 to 1.5 mbd

- Correlation between GDP growth and oil use is failing

- North American weather shifting 1.5 to 2 months.

The Matrix

The oil industry has focused on finding new reserves for most of its existence. The concern was that economic growth might not be sustained if oil reached its supply peak. That concern – called “peak oil”– was the point at which declining output from producing wells was not able to be replaced with new supply.

The peak oil debate appears now to be archaic. It has been overtaken by a series of changes that could actually cause demand for oil to top out. And perhaps much more rapidly than might be imagined. The typical industry expectation is for a peak around 2040. European companies are in this group with American oil companies still rejecting the idea of a top.

The reasons for a potential downturn in demand do not reflect substantially less consumer demand. Rather, it is because the conditions under which demand is satisfied are likely to be satisfied with fewer hydrocarbons.

Technology is the most obvious source of more efficient oil use through re-engineering the internal combustion engine. In addition, fuel demand could fall as carbon rules become effective.

The broad acceptance of electric vehicles will eat into oil demand. This will reflect improved battery performance that is expected to allow travel for hundreds of miles without a recharge. Ironically, the advent of broad use of electric vehicles could have less impact than might be expected. One analysis projects 100 million electric autos on the roads by 2035. (There are one million in use today.) Even this dramatic increase in vehicles could reduce global demand for oil of one to 1.5 million barrels per day.

Most of the new oil demand now being experienced is happening in developing countries. Historically, there has been high correlation between economic growth and oil demand. This relationship is now failing in advanced economies. As developing nations achieve growth, a similar decoupling may be expected.

Supply/Demand Balances

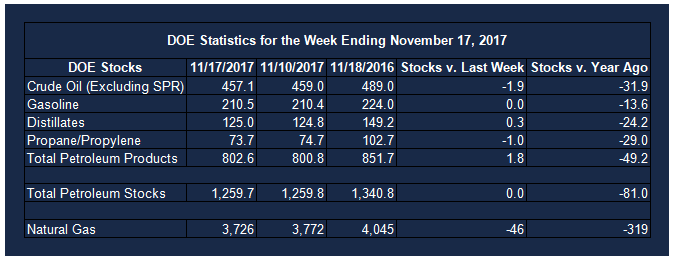

Supply/demand data in the United States for the week ending November 17, 2017 were released by the Energy Information Administration.

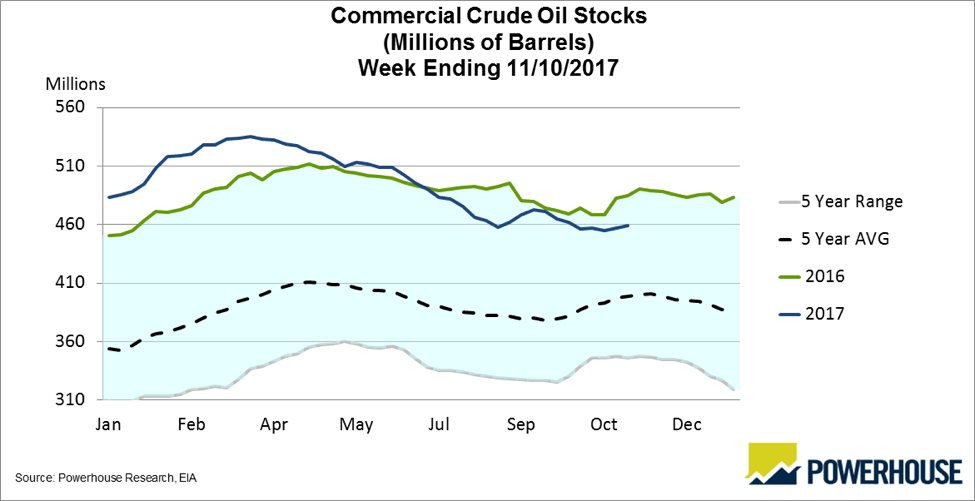

Total commercial stocks of petroleum were unchanged from the previous report week ending November 17, 2017.

Builds were reported in stocks of fuel ethanol, K-jet fuel, distillates, and other oils. Draws were reported in stocks of residual fuel and propane. Stocks of gasoline were unchanged from the previous report week.

Commercial crude oil supplies in the United States decreased to 457.1 million barrels, a draw of 1.9 million barrels.

Crude oil supplies increased in three of the five PAD Districts. PAD District 1 (East Coast) crude oil stocks increased 1.1 million barrels, PADD 4 (Rockies) stocks expanded 0.5 million barrels, and PADD 5 (West Coast) stocks grew 1.6 million barrels. PAD District 2 (Midwest) stocks declined 2.4 million barrels and PADD 3 (Gulf Coast) stocks fell 2.5 million barrels.

Cushing, Oklahoma inventories decreased 1.9 million barrels from the previous report week to 61.2 million barrels.

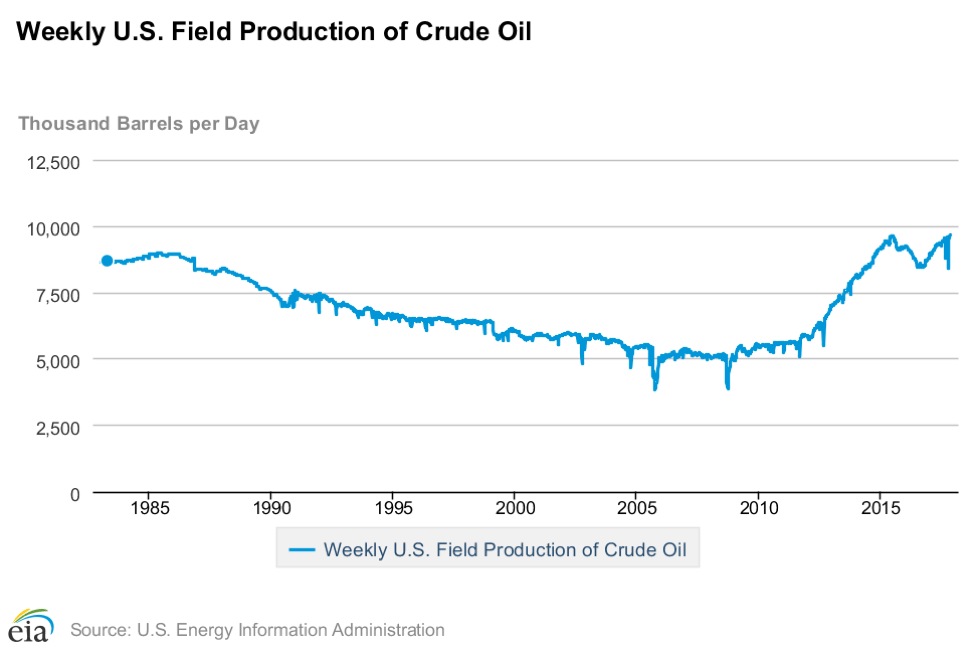

Domestic crude oil production increased 13,000 barrels daily to 9.658 million barrels per day from the previous report week.

Crude oil imports averaged 7.873 million barrels per day, a daily decrease of 25,000 barrels. Exports rose 462,000 barrels daily to 1.591 million barrels per day.

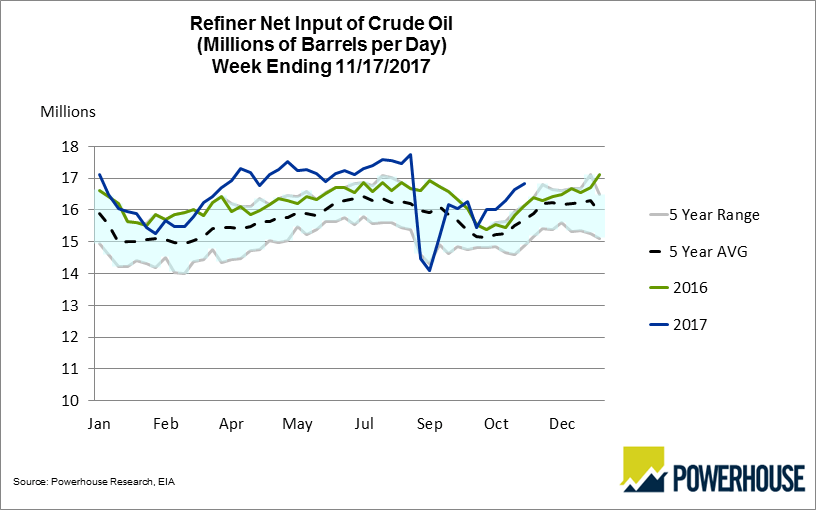

Refineries used 91.3 per cent of capacity, an increase of 0.3 percentage points from the previous report week.

Crude oil inputs to refineries increased 199,000 barrels daily; there were 16.838 million barrels per day of crude oil run to facilities.

Gross inputs, which include blending stocks, rose 69,000 barrels daily to 16.962 million barrels daily.

Total petroleum product inventories saw an increase of 1.8 million barrels from the previous report week.

Gasoline stocks were unchanged from the previous report week; total stocks are 210.5 million barrels.

Demand for gasoline increased 423,000 barrels per day to 9.595 million barrels daily.

Total product demand decreased 466,000 barrels daily to 19.289 million barrels per day.

Distillate fuel oil supply rose 0.3 million barrels from the previous report week to 125.0 million barrels.

National distillate demand was reported at 4.057 million barrels per day during the report week. This was a weekly increase of 27,000 barrels daily.

Propane stocks decreased 1.0 million barrels from the previous report week to 73.7 million barrels. Current demand is estimated at 1.119 million barrels per day, a decrease of 403,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Working gas in storage was 3,726 Bcf as of Friday, November 17, 2017, according to EIA estimates. This represents a net decrease of 46 Bcf from the previous week. Stocks were 319 Bcf less than last year at this time and 121 Bcf below the five-year average of 3,847 Bcf. At 3,726 Bcf, total working gas is within the five-year historical range.

Temperature has frustrated demand for natural gas this autumn. One possible explanation could be found in one analysis of a seasonal shift in weather. Weather 2000, a New-York based meteorologist notes,

Due to ocean circulations and hemispheric patterns and some events that operate on more multi-decadal and multi-century time scales eastern North America seasons are fundamentally shifting about 1 ½ to 2 months.

Septembers are becoming a true summer month, October is a bleed-over CDD month where you can get some real CDD in the southern half of the US and occasional 80 degree days in Chicago.

November and December have become autumn, and January through April has become the true 100-day or 4 month HDD season. April has blown away some of the earlier autumn months in terms of EIA withdrawal and snowstorm potential, May and June are spring and July through September summer.

Incredibly in gas consuming regions from the Midwest to Northeast every single December this decade has been warm. We believe that is the case this year. Other forecasters will look at the warm December and say; “winter is over”; They will not call a spade a spade.

New Years to Easter or Martin Luther King Day to Tax Day we believe there is a lot of harsh winter potential whether the entry point is upper Midwest to High Plains or New England focused. There will be a lot of that this year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this memo helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2017 Powerhouse, All rights reserved