Black Friday

- COVID-19 variant identified in South Africa named Omicron

- World Health Organization says Omicron is a “variant of concern”

- WTI prices fall more than 10% on Friday

- EIA reports first natural gas withdraw of the 2021-2022 season

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Black Friday marks the beginning of the Christmas Holiday shopping season. On the Friday after Thanksgiving, retailers promote big sales and low prices, making it the busiest shopping day of the year. U.S. futures markets trade a short session on Black Friday–typically a sleepy session. Not this year. Traders slashed the price of WTI crude oil over 10% as news of a COVID-19 “variant of concern” was discovered in South Africa. Brent crude saw the 7th largest one-day price drop. ULSD and RBOB finished the session just shy of $0.3 lower. What we learn about the new variant, Omicron, over the coming days will determine if this is a one-day sale or the start of a broader move lower in price.

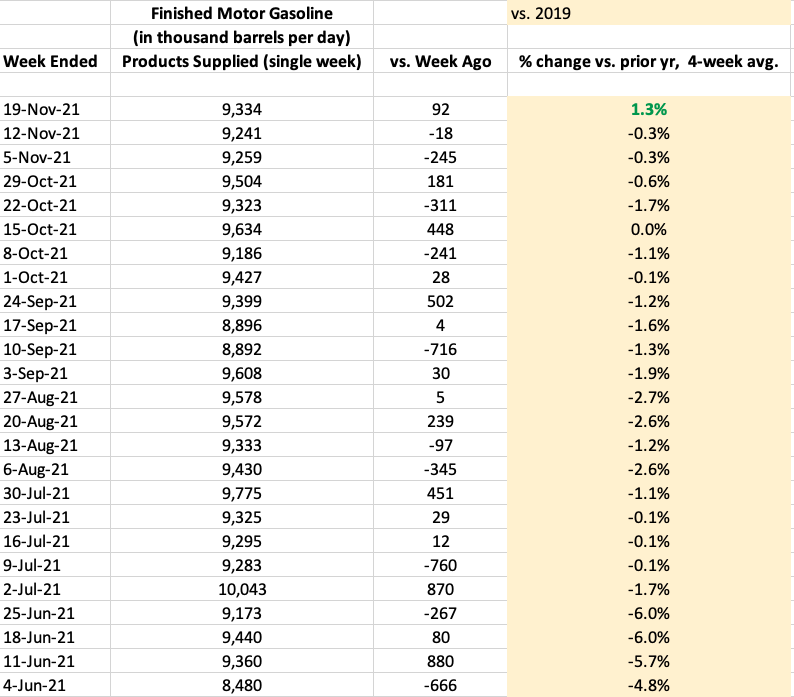

Omicron has the potential to derail the recovery in demand that has been building throughout 2021. Domestic airlines welcomed backed holiday travelers in close to pre-pandemic numbers. Data released last week by the EIA marked the first time that the current rolling 4-week average for gasoline demand was above the same period in 2019.

Gasoline Product Supplied Jun-Nov 2021 Source: EIA

The most immediate impact from the discovery of Omicron was the initiation of new travel bans by multiple countries on flights originating from South Africa and several other southern African nations. COVID-19 cases were already rising globally, with Austria being the first European country to go back into lockdown. If new travel bans (or worse, lockdowns) become widespread, the demand outlook could quickly turn bearish.

OPEC+ is meeting later this week to discuss output. Traders had been bracing for a more hawkish tone from the group as they assessed a coordinated SPR release from the U.S. other major energy-consuming nations. While the group has committed to increasing production monthly by 400,000 b/d through late 2022, they also have the right to alter the plan as market conditions change. Omicron adds new uncertainty to their discussions.

There is still a lot to be learned about the new variant. The outbreak occurred in a country where vaccination rates are low. It is unknown how effective our current vaccines and boosters will be against Omicron. We have learned a lot since the start of the pandemic, and vaccine manufactures say they can react much faster if necessary. Also, it is helpful to remember other strains have been detected before, without serious outcomes. Officials say new travel bans were initiated out of “an abundance of caution.” As new information emerges, it very well may be Black Friday’s sale was one to buy.

Supply/Demand Balances

Supply/demand data in the United States for the week ended Nov. 19, 2021, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 6 million barrels during the week ended Nov. 19, 2021.

Commercial crude oil supplies in the United States increased by 1 million barrels from the previous report week to 434 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.7 million barrels to 8.9 million barrels

PADD 2: Plus 1.3 million barrels to 110.8 million barrels

PADD 3: Down 2.6 million barrels to 240.0 million barrels

PADD 4: Plus 0.1 million barrels to 23.8 million barrels

PADD 5: Plus 3 million barrels to 50.6 million barrels

Cushing, Oklahoma, inventories were up 0.8 million barrels from the previous report week to 27.4 million barrels.

Domestic crude oil production was up 100,000 barrels per day from the previous report week to 11.5 million barrels daily.

Crude oil imports averaged 6.436 million barrels per day, a daily increase of 245,000 barrels. Exports decreased 1,021,000 barrels daily to 2.605 million barrels per day.

Refineries used 88.6% of capacity; 0.7 percentage points higher from the previous report week.

Crude oil inputs to refineries increased 243,000 barrels daily; there were 15.640 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 118,000 barrels daily to 16.058 million barrels daily.

Total petroleum product inventories fell 7 million barrels from the previous report week.

Gasoline stocks decreased 0.6 million barrels from the previous report week; total stocks are 211.4 million barrels.

Demand for gasoline rose by 92,000 barrels per day to 9.334 million barrels per day.

Total product demand increased 123,000 barrels daily to 21.752 million barrels per day.

Distillate fuel oil stocks declined 2 million barrels from the previous report week; distillate stocks are at 121.7 million barrels. EIA reported national distillate demand at 4.391 million barrels per day during the report week, an increase of 41,000 barrels daily.

Propane stocks decreased 1 million barrels from the previous report week; propane stocks are at 73.6 million barrels. The report estimated current demand at 1.624 million barrels per day, an increase of 431,000 barrels daily from the previous report week.

Natural Gas

December natural gas futures expired on Friday at $5.447, finishing $0.38 higher on the day. Last week, the EIA’s storage report reported the first withdraw of the 2021-2022 season, a draw of 21 Bcf. Strong demand for U.S. LNG exports from Europe and Asia added support to prices. Natural Gas Intelligence (NGI) reported, “LNG feed gas volumes held above 11 Bcf throughout the abbreviated trading week – within striking distance of record levels around 12 Bcf.”

According to the EIA:

Working gas in storage was 3,623 Bcf as of Friday, Nov. 19, 2021, according to EIA estimates. This represents a net decrease of 21 Bcf from the previous week. Stocks were 320 Bcf less than last year at this time and 58 Bcf below the five-year average of 3,681 Bcf. At 3,623 Bcf, total working gas is within the five-year historical range.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved