Vaccine Changes the Economic Outlook

- COVID-19 vaccines highly effective in early trial

- Crude oil production recovering

- OPEC+ ready to balance oil markets

- Natural gas price expected to be $3.14 in 2021

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Serious traders know that there is no price too high or too low to which a commodity might go. Energy markets have had their share of both over the years. Last week showed the possibility of either.

Price bulls responded to news of an efficacious vaccine for COVID-19 and assurances that OPEC+ production quotas could be adjusted to “balance” the market.

Price bears were left with evidence that the economy-killing virus had yet to be controlled. COVID-19 health and safety regulations were being reimposed by many states.

A week that opened on Monday, November 9, with a WTI crude oil low of $37.16 rallied nearly five dollars by Wednesday, reaching $43.06. Data released by the Energy Information Administration at that time showed an increase of 4.3 million barrels of supply. Oil markets responded bearishly, just barely holding on to $40.

The bullish vaccine news could eventually power prices higher. There are still challenges of near-term soft demand and expanding crude oil supply to be overcome.

Demand for petroleum products in the United States had moved solidly above twenty million barrels daily since 2018. The first economy-shutdown last spring cut demand briefly to fifteen million barrels daily. Consumption has recovered, but still struggles to reach recent highs. European demand continues to falter as well, affecting bars, restaurants and travel.

Crude oil production has suffered from the extended train of Gulf Coast hurricanes this year. One estimate put the loss of Gulf crude oil at more than 500,000 barrels per day since August 22nd. Globally, this loss has been offset by higher production in Libya and Iraq.

The weakness in oil prices brought on by a lagging economy and recovering crude oil supply sees support for ULSD around $1.06. If distillate fuel oil breaks the buck, further support could be found at $0.85.

The COVID-19 vaccines recently announced gives us many reasons to be optimistic longer-term. Their 90+ percent rates of preventing symptomatic Covid-19 is much higher than had been expected. This could lead to greater acceptance of vaccinations in the United States, a healthy population and demand recovery.

Supply/Demand Balances

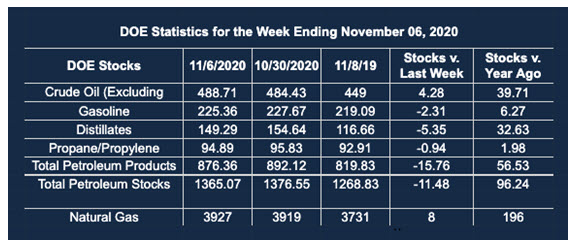

Supply/demand data in the United States for the week ended Nov. 6, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 11.5 million barrels during the week ended Nov. 6, 2020.

Commercial crude oil supplies in the United States increased by 4.3 million barrels from the previous report week to 488.7 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.4 million barrels to 10.0 million barrels

PADD 2: Down 0.6 million barrels to 146.0 million barrels

PADD 3: Plus 5.1 million barrels to 258.5 million barrels

PADD 4: Plus 1.7 million barrels to 24.6 million barrels

PADD 5: Down 1.6 million barrels to 49.5 million barrels

Cushing, Oklahoma inventories were down 0.5 million barrels from the previous report week to 60.4 million barrels.

Domestic crude oil production was unchanged from the previous report week at 10.5 million barrels daily.

Crude oil imports averaged 5.499 million barrels per day, a daily increase of 470,000 barrels. Exports increased 500,000 barrels daily to 2.765 million barrels per day.

Refineries used 74.5% of capacity, down 0.8% from the previous report week.

Crude oil inputs to refineries decreased 105,000 barrels daily; there were 13.447 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 146,000 barrels daily to reach 13.873 million barrels daily.

Total petroleum product inventories fell 15.8 million barrels from the previous report week.

Gasoline stocks decreased 2.3 million barrels daily from the previous report week; total stocks are 225.4 million barrels.

Demand for gasoline rose 426,000 barrels per day to 8.762 million barrels per day.

Total product demand increased 1.819 million barrels daily to 20.180 million barrels per day.

Distillate fuel oil stocks decreased 5.4 million barrels from the previous report week; distillate stocks are at 149.3 million barrels. EIA reported national distillate demand at 4.054 million barrels per day during the report week, an increase of 292,000 barrels daily.

Propane stocks decreased 0.9 million barrels from the previous report week; propane stocks are 94.9 million barrels. The report estimated current demand at 1.297 million barrels per day, an increase of 49,000 barrels daily from the previous report week.

Natural Gas

The Energy Information Administration released its Short-Term Energy Outlook. EIA projects a monthly average price of natural gas at Henry Hub to be $3.42 in January 2021. The Administration estimates the calendar 2021 price to be $3.14. EIA is anticipating space heating needs, LNG exports and lower production to balance the natural gas market.

According to the EIA:

The net [natural gas] injections into storage totaled 8 Bcf for the week ending November 6, compared with the five-year (2015–19) average net injections of 33 Bcf and last year’s net injections of 12 Bcf during the same week. Working natural gas stocks totaled 3,927 Bcf, which is 176 Bcf more than the five-year average and 196 Bcf more than last year at this time.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2020 Powerhouse Brokerage, LLC, All rights reserved