Price Vector for Second Half 2019 RBOB Uncertain

- RBOB prices typically trend lower after Memorial Day

- IMO 2020 could impact RBOB prices this year

- NOAA projects a “near-normal” hurricane season

- Natural gas stocks 137 Bcf more than last year at this time

The Matrix

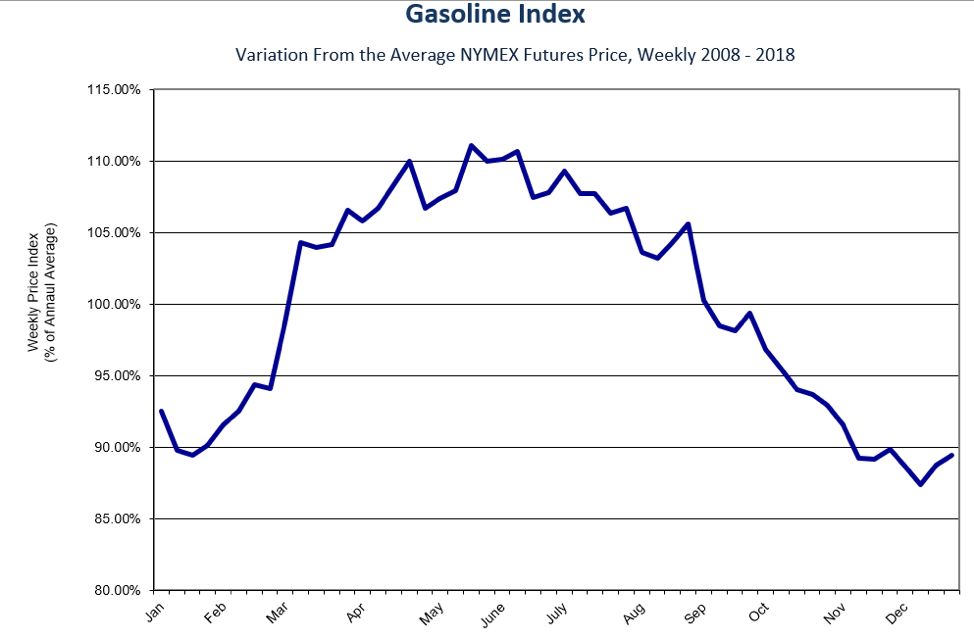

RBOB prices found their 2019 bottom on January 2 at $1.2685. They vaulted higher during the next three and one-half months, advancing 70 percent to reach a top at $2.1489. Prices have since retreated, reaching the Memorial Day holiday around $1.90.

The apparent top in RBOB prices should not come as a surprise. Powerhouse has measured typical pricing in gasoline. The resulting Gasoline Index shows the high average price occurring early in May. Subsequent months experience a generally weakening pattern.

U.S. Natural Gas Weekly Underground Storage 2014 – 2019 source: EIA

Several factors fueled the RBOB rally. Demand proved better than expected (but did not break ten million barrels daily – an objective not yet reached in the United States.) Refinery turnarounds that reduced gasoline output extended longer than usual.

The impact of IMO 2020 will likely hold the key to the gasoline situation in the second half of 2019. Ship owners may opt to use 0.5% Marine Gasoil (MGO) to comply with the low Sulphur mandate. An additional supply of RBOB would be produced incidental to refining in this situation, This would be bearish for RBOB prices.

Refiners may be asked to provide ultra-low sulfur fuel oil (ULSFO) for compliance. Gasoline production would be curtailed as feedstock was diverted. The effect on gasoline prices would then be bullish.

Weather always has an impact on prices. Hurricane season is about to begin, bringing its implications for summer/autumn gasoline prices. The Climate Prediction Center of the National Oceanic Atmospheric Administration expects a 40 percent chance of a near-normal Atlantic hurricane season. CPC puts the chance of an above-normal season at 30 percent.

The meteorologists predict between nine and 15 named storms. Named storms have winds of 39 mph or higher. An average hurricane season has “12 named storms of which six become hurricanes, including three major hurricanes.” An ongoing El Niño could suppress the intensity of the hurricane season.

Supply/Demand Balances

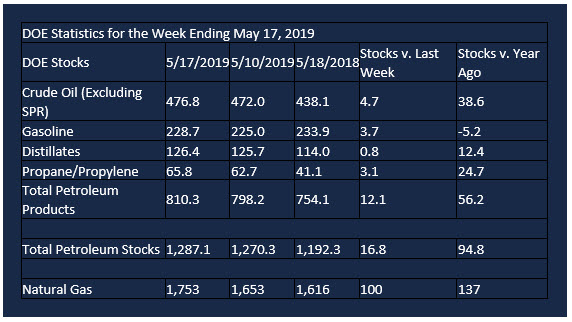

U.S. crude oil refinery inputs averaged 16.6 million barrels per day during the week ending May 17, 2019, which was 98,000 barrels per day less than the previous week’s average.

Refineries operated at 89.9% of their operable capacity last week.

U.S. crude oil imports averaged 6.9 million barrels per day last week, down by 669,000 barrels per day from the previous week. Over the past four weeks, crude oil imports averaged about 7.2 million barrels per day, 9.4% less than the same four-week period last year.

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 4.7 million barrels from the previous week. At 476.8 million barrels, U.S. crude oil inventories are about 4% above the five year average for this time of year.

Total motor gasoline inventories increased by 3.7 million barrels last week and are at the five year average for this time of year.

Finished gasoline and blending components inventories both increased last week.

Distillate fuel inventories increased by 0.8 million barrels last week and are about 4% below the five year average for this time of year. Propane/propylene inventories increased by 3.1 million barrels last week and are about 22% above the five year average for this time of year.

Total commercial petroleum inventories increased last week by 16.8 million barrels last week.

Finished gasoline and blending components inventories both increased last week.

Distillate fuel inventories increased by 0.8 million barrels last week and are about 4% below the five year average for this time of year. Propane/propylene inventories increased by 3.1 million barrels last week and are about 22% above the five year average for this time of year.

Total commercial petroleum inventories increased last week by 16.8 million barrels last week.

Total products supplied over the last four-week period averaged 19.9 million barrels per day, down by 2.7% from the same period last year. Over the past four weeks, motor gasoline product supplied averaged 9.4 million barrels per day, down by 1.1% from the same period last year.

Distillate fuel product supplied averaged 4.0 million barrels per day over the past four weeks, down by 4.0% from the same period last year.

Jet fuel product supplied was up 2.5% compared with the same four-week period last year.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 100 Bcf for the week ending May 17, compared with the five-year (2014–18) average net injections of 88 Bcf and last year’s net injections of 93 Bcf during the same week. Working gas stocks totaled 1,753 Bcf, which is 274 Bcf lower than the five-year average and 137 Bcf more than last year at this time.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this memo helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.

You are receiving this e-mail as a friend of Powerhouse