Oil Stocks Under Pressure Despite OPEC Easing

- Cushing OK crude stocks halve last year’s level

- Potential tariff impost is a wild card

- Reduced hurricane threat this season

- Snowy winter projected

The Matrix

The possible range of oil price trajectories going forward this year is unusually wide. Record U.S. production and the prospect of expanding OPEC/Russian output are bearish. At the same time, booming global demand and shrinking oil inventories are concerning from the bulls’ point of view.

Supplies of crude oil at Cushing, Oklahoma were 32.6 million barrels for the week ending June 15. Last year at this time there were 61.1 million barrels. Heavily discounted U.S. oil prices translate into attractive stocks for export, adding to concerns for domestic supply.

A major uncertainty resides in the government’s threats of imposing protective tariffs. Duties, real or anticipated have reportedly led to postponements of expansion plans and higher material costs. It’s also possible that talk of tariff increases is just that – talk, a negotiating ploy.

If that’s not enough to encourage establishing hedged positions, the weather continues to supply more fodder for traders. This time it concerns hurricanes and an unusually early look at next winter.

The hurricane season is now underway. One of the causes of hurricanes is the water temperature in the tropical Atlantic Ocean. And this year, sea surface temperatures (SSTs) have become unexpectedly cold. SSTs are the coldest they’ve been since the early 1980’s. Warm waters fuel hurricanes.

Now, as summer begins, the days get shorter and average temperatures start to fall. Precursors to a snowy winter, according to private forecasters, are a “‘weak to moderate’ El Niño, a warm Pacific Ocean and a quiet sun.”

An El Niño watch has been established by the National Weather Service. Most computer models are projecting such an event this winter. Expectations in the northeast Pacific Ocean, especially in the Gulf of Alaska, favor above-normal SSTs in winter. Finally, we are experiencing a very quiet solar cycle with lower sunspot activity. Taken together, these elements could deliver more snow next winter.

Supply/Demand Balances

Supply/demand data in the United States for the week ending June 15, 2018 were released by the Energy Information Administration.

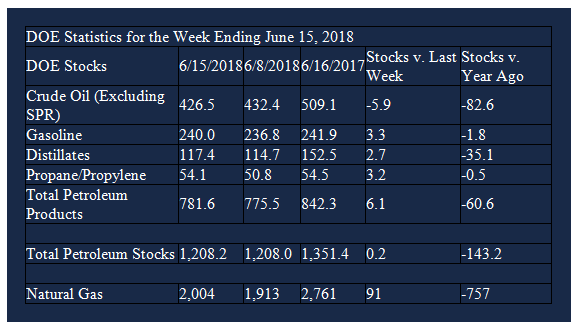

Total commercial stocks of petroleum rose 0.2 million barrels during the week ending June 15, 2018.

There were builds in stocks of gasoline, distillate fuel oil, residual fuel, and propane. There were draws in stocks of fuel ethanol, K-jet fuel, and other oils.

Commercial crude oil supplies in the United States decreased to 426.5 million barrels, a draw of 5.9 million barrels.

Crude oil supplies decreased in all five PAD Districts. PAD District 1 (East Coast) crude oil stocks fell 0.2 million barrels, PADD 2 (Midwest) stocks declined 4.2 million barrels, PADD 3 (Gulf Coast) crude oil stocks decreased 0.7 million barrels, PADD 4 (Rockies) stocks fell 0.5 million barrels, and PADD 5 (West Coast) stocks retreated 0.3 million barrels.

Cushing, Oklahoma inventories decreased 1.5 million barrels from the previous report week to 33.9 million barrels.

Domestic crude oil production was unchanged from the previous report week at 10.900 million barrels per day.

Crude oil imports averaged 8.242 million barrels per day, a daily increase of 143,000 barrels per day. Exports increased 344,000 barrels daily to 2.374 million barrels per day.

Refineries used 96.7 per cent of capacity, an increase of 1.0 percentage points from the previous report week.

Crude oil inputs to refineries increased 196,000 barrels daily; there were 17.701 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 185,000 barrels daily to 17.983 million barrels daily.

Total petroleum product inventories saw an increase of 5.9 million barrels from the previous report week.

Gasoline stocks increased 3.3 million barrels from the previous report week; total stocks are 240.0 million barrels.

Demand for gasoline fell 553,000 barrels per day to 9.326 million barrels per day.

Total product demand decreased 1.573 million barrels daily to 20.228 million barrels per day.

Distillate fuel oil supply increased 2.7 million barrels from the previous report week to 117.4 million barrels. National distillate demand was reported at 3.825 million barrels per day during the report week. This was a weekly decrease of 579,000 barrels daily.

Propane stocks rose 3.2 million barrels from the previous report week; propane stock are 54.1 million barrels. Current demand is estimated at 548,000 barrels per day, a decrease of 238,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections [of natural gas] rose higher than the five-year average. Net injections into storage totaled 91 Bcf for the week ending June 15, compared with the five-year (2013–17) average net injection of 83 Bcf and last year’s net injections of 63 Bcf during the same week.

Net injections averaged 13.7 Bcf/d and will have to average 12.6 Bcf/d for the remainder of the refill season to match the five-year average level (3,815 Bcf) by October 31. Working gas stocks totaled 2,004 Bcf, which is 499 Bcf lower than the five-year average and 757 Bcf lower than last year at this time.

Here is a current view of the Natural Gas price situation developed by POWERHOUSE’s David Thompson, CMT:

The breakout from the consolidation range that I highlighted on June 13th proceeded exactly to the target level of $3.14 just two days later.

Shortly after that initial price target was reached, selling pressure became much more intense and the market was pushed lower. However, the most recent bounce higher has started from within the previous area of price congestion. This indicates the price range between $3.03 – $3.08 for the winter strip remains a support zone.

From a seasonal perspective, it’s important to note that the rolling, front-month natural gas futures price tends to make an intermediate top in June (the ultimate high price for the year occurs typically in December). If the winter strip breaks below $3.03, I expect selling to intensify with the possibility to drive values under $2.95.

POWERHOUSE can make a natural gas chart showing seasonal tendencies. Contact us for more information.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2018 Powerhouse, All rights reserved.