Competing Supply and Demand Forces Stall Oil Price Rally; Offer Options for Marketers

1. China’s crude oil buying spree may be coming to an end as OPEC+ eases supply cuts modestly

2. COVID-19 affects the refined products export market

3. Fuel marketers can use options to address commercial customers’ concerns

The Matrix

Recent analysis from the commodities desks of various banks has painted a mixed fundamental picture for the global energy market. One strategy team expressed concern about changing demand patterns in China. Led by the state-owned oil companies, China went on a crude oil buying spree as markets were oversupplied, and prices depressed in early Spring of this year. Chinese crude oil demand rose by approximately 3 million barrels/day or 34% from the low point in March 2020. However, Chinese crude oil buying may slow as prices are no longer as attractive and local storage has filled up.

Another bank analyst focuses on the export market for U.S. refined products. Historically, products exports have accounted for 25% of total demand. The export market’s ‘return to normal,’ to create incremental demand, will be contingent on Latin American countries’ abilities to check the spread of the virus.

On the supply side, the consensus view is that OPEC+ has maintained strong overall compliance with their planned oil output cuts. The recently announced easing of these cuts should be offset by increased domestic Middle East demand as Gulf states burn additional crude for power generation during the summer months.

These competing market forces have largely played out as sideways price action over the last six weeks. A sharp contrast from the March through May period that saw significant price rallies in both gasoline and distillates.

The most common question asked of POWERHOUSE recently has come from commercial diesel fuel buyers. They want to know how to take advantage of historically favorable prices but still be able to benefit if prices collapse again.

Last year at this time Q4 ULSD futures prices were approximately $1.98 per gallon—68 cpg more than at present. Yet the diesel market has already rallied more than 60 cpg from its low back in April. Fuel managers can still come in dramatically under last year’s budget numbers but they are anxious about buying now because of the possible return of COVID-19 related shut-downs driving prices lower once again.

A call option can offer the best of both possible worlds. Commercial buyers could protect their Q4 diesel fuel budgets against NYMEX prices above $1.30/gal. for a cost of $0.13 cpg. This makes their break even costs $1.43/gal.—still far better than last year’s comparables. But instead of being locked in at $1.30/gal, the call option allows fuel managers to benefit should NYMEX prices move lower.

A call option offers a cap against higher prices without the concern of locking in a fixed price. Please reach out to Powerhouse to learn more about strategies that can help you protect your margins and grow your business.

Supply/Demand Balances

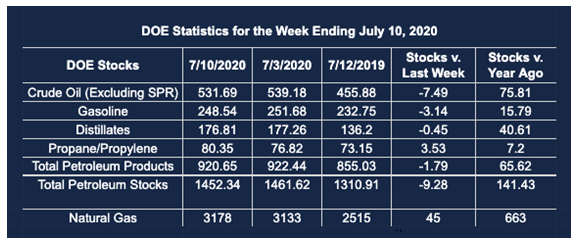

Supply/demand data in the United States for the week ended July 10, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 9.3 million barrels during the week ended July 10, 2020.

Commercial crude oil supplies in the United States decreased by 7.5 million barrels from the previous report week to 531.7 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 1.0 million barrels from previous report week to 13.1 million barrels

PADD 2: Plus 0.9 million barrels to 137.2 million barrels

PADD 3: Down 7.9 million barrels to 301.1 million barrels

PADD 4: UNCH from the previous report week at 25.6 million barrels

PADD 5: Down 1.5 million barrels to 54.7 million barrels

Cushing, Oklahoma inventories were up 0.9 million barrels from the previous report week to 48.7 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.0 million barrels daily.

Crude oil imports averaged 5.567 million barrels per day, a daily decrease of 1.827 million barrels. Exports rose 156,000 barrels daily to 2.543 million barrels per day.

Refineries used 78.1% of capacity, plus 0.6% from the previous report week.

Crude oil inputs to refineries decreased 38,000 barrels daily; there were 14.309 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 128,000 barrels daily to reach 14.826 million barrels daily.

Total petroleum product inventories fell 1.8 million barrels from the previous report week.

Gasoline stocks decreased 3.1 million barrels daily from the previous report week; total stocks are 248.5 million barrels.

Demand for gasoline fell 118,000 barrels per day to 8.648 million barrels per day.

Total product demand increased 361,000 barrels daily to 18.480 million barrels per day.

Distillate fuel oil stocks decreased 0.5 million barrels from the previous report week; distillate stocks are at 176.8 million barrels. EIA reported national distillate demand at 3.692 million barrels per day during the report week, an increase of 673,000 barrels daily.

Propane stocks increased 3.5 million barrels from the previous report week; propane stocks are 80.3 million barrels. The report estimated current demand at 913,000 barrels per day, an increase of 266,000 barrels daily from the previous report week.

Natural Gas

According to EIA:

The net injections into storage totaled 45 Bcf for the week ending July 10, compared with the five-year (2015–19) average net injections of 63 Bcf and last year’s net injections of 67 Bcf during the same week. Working natural gas stocks totaled 3,178 Bcf, which is 436 Bcf more than the five-year average and 663 Bcf more than last year at this time.

The average rate of injections into storage is 12% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.7 Bcf/d for the remainder of the refill season, the total inventory would be 4,159 Bcf on October 31, which is 436 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.