Is There a Bottom in Distillate Fuel Oil Prices?

- Annual low in distillate fuel oil prices typically occurs in January

- ULSD Futures Open Interest rapidly growing from its lows

- Inventories of distillates grew 9.5 million barrels in most recent report

- Natural gas support is around $2.79

The Matrix

Petroleum futures market price action does not always conform to expectations. And sometimes, expectations themselves can generate mixed ideas of where prices might go. The Ultra-Low Sulfur Diesel (ULSD) futures contract offers a good example of this complexity.

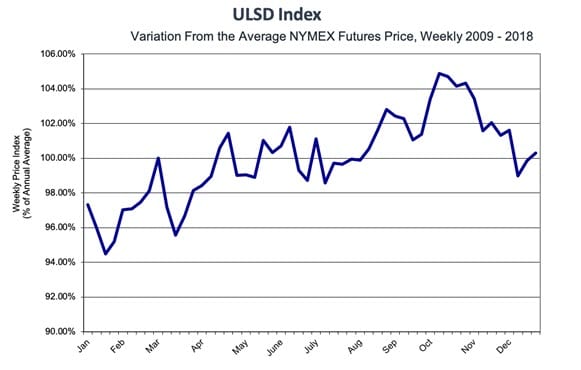

Diesel prices have typically reached their lows early in the year, a time when many dealers seek to establish futures positions for the year. The average annual low was set during winter in the ten years from 2009 through 2018. This included the months of December through February. The ULSD Index chart shown below shows how much variation exists between weekly NYMEX ULSD futures prices and the average NYMEX ULSD futures price. These data are shown as percentages.

ULSD Seasonal Price Index 2009-2018

Source: Powerhouse

Not surprisingly, the greatest downside variation occurs in January. This is consistent with history and supports the idea that ULSD prices bottom at this time.

Another indicator of a possible bottom in ULSD prices may be found in Open Interest. Open interest measures the number of working futures contracts. And if open interest rises while prices are rising, traders see a bullish situation. (Rising open interest in a rising market means that bulls are adding in to profitable positions.) As 2018 ended, Open Interest of ULSD contracts was 367,000. A mere three days later, open interest added more than 9,000 contracts. Prices rose more than six cents. (On Friday, January 04, 2019, prices added yet another three-and-one-half cents.)

This rally occurred in the face of remarkably bearish inventory for the week ending December 28, 2018. Petroleum stocks added 14.6 million barrels to supply. Notably, gasoline stocks rose 6.9 million barrels and distillate fuel oil inventories added 9.5 million barrels. In part this reflected reduced exports of 1.2 million barrels across both crude oil and products. This has all occurred during the year-end holiday period and will likely adjust in the next several days.

One ignores these signs at their peril.

Supply/Demand Balances

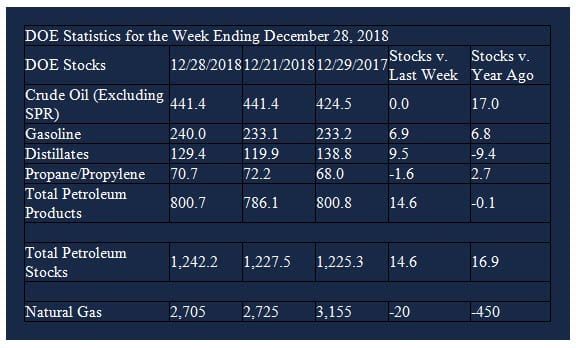

Supply/demand data in the United States for the week ending December 28, 2018 were released by the Energy Information Administration.

Total commercial stocks of petroleum increased 14.6 million barrels during the week ending December 28, 2018.

There were builds in stocks of gasoline, K-jet fuel, distillates, and residual fuel. There were draws in stocks of propane and other oils. Stocks of fuel ethanol were unchanged from the previous report week.

Commercial crude oil supplies in the United States was unchanged from the previous report week at 441.4 million barrels.

Crude oil supplies increased in three of the five PAD Districts. PADD 1 (East Coast) crude oil stocks grew 1.4 million barrels, PADD 2 (Midwest) stocks rose 1.1 million barrels, and PADD 3 (Gulf Coast) stocks. PADD 4 (Rockies) stocks declined 0.2 million barrels and PADD 5 (West Coast) stocks decreased 2.9 million barrels.

Cushing, Oklahoma inventories increased 0.6 million barrels from the previous report week to 41.9 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.7 million barrels per day.

Crude oil imports averaged 7.392 million barrels per day, a daily decrease of 264,000 barrels per day. Exports fell 732,000 barrels daily to 2.237 million barrels per day.

Refineries used 95.1 per cent of capacity, a decrease of 0.3 percentage points from the previous report week.

Crude oil inputs to refineries increased 410,000 barrels daily; there were 17.760 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 383,000 barrels daily to 18.077 million barrels daily.

Total petroleum product inventories grew 14.6 million barrels from the previous report week.

Gasoline stocks increased 6.9 million barrels from the previous report week; total stocks are 233.1 million barrels.

Demand for gasoline decreased 726,000 barrels per day to 8.623 million barrels per day.

Total product demand decreased 1.685 million barrels daily to 19.056 million barrels per day.

Distillate fuel oil stocks decreased 9.5 million barrels from the previous report week; distillate stocks are at 129.4 million barrels. National distillate demand was reported at 3.203 million barrels per day during the report week. This was a weekly decrease of 1.039 million barrels daily.

Propane stocks decreased 1.6 million barrels from the previous report week; propane stock are 70.7 million barrels. Current demand is estimated at 1.586 million barrels per day, a increase of 449,000 barrels daily from the previous report week.

Natural Gas

According to the EIA:

Working gas in storage was 2,705 Bcf as of Friday, December 28, 2018, according to EIA estimates. This represents a net decrease of 20 Bcf from the previous week. Stocks were 450 Bcf less than last year at this time and 560 Bcf below the five-year average of 3,265 Bcf. At 2,705 Bcf, total working gas is below the five-year historical range.

Natural gas prices reacted bearishly to these data. Technical analysts place support around $2.79. Break of this level opens the way to around $2.50.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2019 Powerhouse, All rights reserved.