Oil Price Situation Resolves Bearishly

- Heating Degree Days fall short by 11 percent

- Biological threat to demand seen

- Ocean shippers raise demand for ULSD

- Natural gas price breaks two bucks.

The Matrix

Last week’s Weekly Energy Market Situation focused on contrary economic factors on which petroleum was being priced: for example, EIA projected higher WTI crude oil prices (bullish,) while domestic production was likely to grow (bearish,) among other things.

These contradictions lasted for many weeks. Economic activity is cyclical, and global events took a turn toward the bearish as they unfolded. Warmer weather has plagued oil sellers this winter. NOAA’s heating degree day data for the Degree Day year starting July 1, 2019 through January 18, 2020, shows HDDs lagging Normal by eleven percent for the United States. This was true for the Mid-Atlantic states too. The South Atlantic region has fallen 20 percent below normal HDDs. There is little in the forecasts to suggest colder weather in the offing.

Warmer weather comes at a time when dealers can more readily protect their profit margin from falling with weather hedges. Ironically, Powerhouse saw less interest in such contracts this heating season than in previous years.

The emergence of a coronavirus in China was another event that caused prices to move lower. Prices under pressure reflected concerns that the virus could spread globally, cutting into demand. The impact on China itself has been powerful. The government reported declines of nearly 42 percent in civil air travel and in rail travel and 25 percent in road transport. If the virus spreads further, the bearish implications for transportation fuels loom stronger.

Concerns long expressed that the IMO requirement to use low-sulfur fuels in ocean shipping could create shortages in ULSD stocks have turned out to be overstated. Low Sulfur Fuel Oil sales in Southeast Asia are reportedly rising, pointing toward implementation by ocean shippers. There has been little evidence of product shortfalls.

The combination of these events, failure of HDDs, concern that a virus might reduce demand and observance of the IMO sulfur requirements coalesced to pressure prices lower. ULSD futures broke long-standing triple bottom support at $1.74. The next major support is around $1.6425. Gasoline futures were caught in the downdraft, breaking their support at $1.5230, heading now towards $1.4475. Crude oil alone is holding support at $54.35. Next support is $50.52.

Supply/Demand Balances

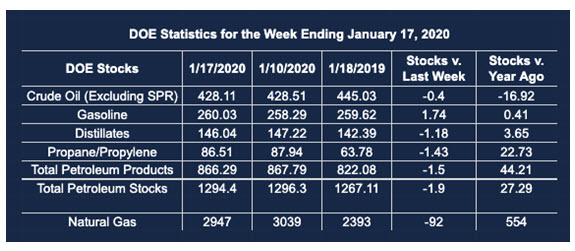

Supply/demand data in the United States for the week ending Jan. 17, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 1.9 million barrels during the week ending Jan. 17, 2020.

Commercial crude oil supplies in the United States decreased by 0.4 million barrels from the previous report week to 428.1 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.4 million barrels to 10.3 million barrels

PADD 2: Down 0.3 million barrels to 125.9 million barrels

PADD 3: Plus 0.8 million barrels to 219.2 million barrels

PADD 4: Down 0.4 million barrels to 21.5 million barrels

PADD 5: Down 1.0 million barrels to 51.1 million barrels

Cushing, Oklahoma inventories down 0.9 million barrels from the previous report week to 34.9 million barrels.

Domestic crude oil production was unchanged from the previous report week at 13.0 million barrels daily.

Crude oil imports averaged 6.432 million barrels per day, a daily decrease of 120,000 barrels. Exports fell 67,000 barrels daily to 3.414 million barrels per day.

Refineries used 90.5 percent of capacity, down 1.7% from the previous report week.

Crude oil inputs to refineries decreased 116,000 barrels daily; there were 16.857 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 312,000 barrels daily to reach 17.021 million barrels daily.

Total petroleum product inventories fell 1.5 million barrels from the previous report week.

Gasoline stocks increased 1.7 million barrels daily from the previous report week; total stocks are 260.0 million barrels.

Demand for gasoline rose 104,000 barrels per day to 8.662 million barrels per day.

Total product demand increased 2.461 million barrels daily to 21.504 million barrels per day.

Distillate fuel oil stocks decreased 1.2 million barrels from the previous report week; distillate stocks are at 146.0 million barrels. EIA reported national distillate demand at 4.389 million barrels per day during the report week, an increase of 1.204 million barrels daily.

Propane stocks decreased 1.4 million barrels from the previous report week; propane stocks are 86.5 million barrels. The report estimated current demand at 1.492 million barrels per day, an increase of 2,000 barrels daily from the previous report week.

Natural Gas

Weather continues to drive natural gas prices lower. A break below $2.00 is powerfully bearish. A new gap at $1.97 is a new point of resistance to any price advance. The prospect of a significant rally diminishes as winter wears on.

Withdrawals lag the five-year average by 22 percent leaving considerable supply available.

According to EIA:

The net withdrawal [of natural gas] from storage totaled 92 Bcf for the week ending January 17, compared with the five-year (2015–19) average net withdrawal of 194 Bcf and last year’s net withdrawal of 152 Bcf during the same week. Working natural gas stocks totaled 2,947 Bcf, which is 251 Bcf more than the five-year average and 554 Bcf more than last year at this time.

The average rate of withdrawal from storage is 22% lower than the five-year average so far in the withdrawal season (November through March). If the rate of withdrawal from storage matched the five-year average of 13.5 Bcf/d for the remainder of the withdrawal season, the total inventory would be 1,948 Bcf on March 31, which is 251 Bcf higher than the five-year average of 1,697 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.