Cold Winter Seen on Tap

- Polar vortex splits in thirds

- Winds aloft shift to North South from West East

- Shale oil production aims at 13 mmb/d in 2020

- LNG exports reach new record

DOE statistics week of january 11 2019

The Matrix

Energy prices are influenced by many factors. Weather is perhaps the most important of these, influencing, as it does, electric power generation, home heating oil and propane. Weather impacts in the United States include the polar vortex, a feature seen in the Arctic. The vortex has recently split in three parts. Weather east-of-the-Rockies has been unusually warm but the change in the polar vortex projects a dramatic mover to colder weather for the rest of winter. When the polar fracture occurs, winds aloft shift more northerly. This allows Arctic air to move more easily in North America and Europe. Meteorologists expect colder weather to build slowly for the rest of January.

As strong as the January cold is expected to be, “what’s coming at the tail end of January into early February will be a lot more impressive. This is about the coldest planetary-scale pattern you can ask for.” Weather experts expect greater potentials for snow, reflecting the El Nino event now also underway. This pattern is expected to remain through February.

Strength in ULSD brought prices from $1.64 to $1.92 in eight trading sessions as 2019 began. A small retracement now opens a path higher, looking toward $2.10. It also reduces the likelihood of new lows developing in the near term. Nonetheless, price bulls cannot ignore the EIA expectation that U.S. crude oil production will rise to 12 million barrels daily in 2019 and nearly 13 million barrels per day in 2020. The country has become the world’s largest producer of crude oil, reflecting continuing gains in shale oil output. Other non-OPEC producers have exhibited gains too, presenting new facets to global petroleum geopolitics. In particular, Iran’s status on the global stage remains uncertain. And the likelihood of OPEC-Russia sustaining output cuts remains to be tested.

Supply/Demand Balances

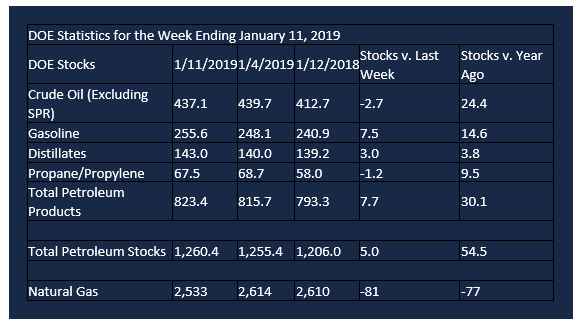

Supply/demand data in the United States for the week ending January 11, 2019 were released by the Energy Information Administration.

Total commercial stocks of petroleum increased 5.0 million barrels during the week ending January 11, 2019.

There were builds in stocks of gasoline, fuel ethanol, and distillates. There were draws in stocks of propane and other oils. Stocks of K-jet fuel and residual fuel were unchanged from the previous week.

Commercial crude oil supplies in the United States decreased 2.7 million barrels from the previous report week to 437.1 million barrels.

Crude oil supplies decreased in three of the five PAD Districts. PADD 1 (East Coast) stocks declined 2.5 million barrels, PADD 2 (Midwest) stocks fell 0.5 million barrels, and PADD 5 (West Coast) stocks retreated 0.1 million barrels. PADD 3 (Gulf Coast) crude oil stocks increased 0.5 million barrels. PADD 4 (Rockies) crude oil stocks were unchanged from the previous report week.

Cushing, Oklahoma inventories decreased 0.8 million barrels from the previous report week to 41.5 million barrels.

Domestic crude oil production was rose 200,000 barrels daily from the previous report week to 11.9 million barrels per day.

Crude oil imports averaged 7.527 million barrels per day, a daily decrease of 319,000 barrels per day. Exports rose 901,000 barrels daily to 2.966 million barrels per day.

Refineries used 94.6 per cent of capacity, a decrease of 1.5 percentage points from the previous report week.

Crude oil inputs to refineries decreased 343,000 barrels daily; there were 17.223 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, declined 234,000 barrels daily to 17.599 million barrels daily.

Total petroleum product inventories grew 7.7 million barrels from the previous report week.

Gasoline stocks increased 7.5 million barrels from the previous report week; total stocks are 255.6 million barrels.

Demand for gasoline decreased 170,000 barrels per day to 8.565 million barrels per day.

Total product demand increased 1.1 million barrels daily to 20.864 million barrels per day.

Distillate fuel oil stocks increased 3.0 million barrels from the previous report week; distillate stocks are at 143.0 million barrels. National distillate demand was reported at 4.449 million barrels per day during the report week. This was a weekly increase of 1.494 million barrels daily.

Propane stocks decreased 1.2 million barrels from the previous report week; propane stock are 67.5 million barrels. Current demand is estimated at 1.574 million barrels per day, an increase of 48,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net withdrawals from storage totaled 81 Bcf for the week ending January 11, compared with the five-year (2014–18) average net withdrawals of 218 Bcf and last year’s net withdrawals of 208 Bcf during the same week. Working gas stocks totaled 2,533 Bcf, which is 327 Bcf lower than the five-year average and 77 Bcf lower than last year at this time.

The average rate of net withdrawals from storage is 31% lower than the five-year average so far in the withdrawal season (November through March). If the rate of withdrawals from storage matched the five-year average of 15.5 Bcf/d for the remainder of the withdrawal season, total inventories would be 1,309 Bcf on March 31, which is 327 Bcf lower than the five-year average of 1,636 Bcf for that time of year.

Liquified Natural Gas (LNG) has steadily advanced as an important part of the country’s energy balance. Analysts expect the United States to become a globally important LNG exporter in 2019. We would join Qatar and Australia as a major supplier of LNG to global users. The effect is likely to be most felt in Asia. One important geopolitical impact could be the use of LNG in eastern Europe to blunt the effects of reliance on Russia as a supplier of natural gas. U.S. LNG outflows reportedly set consecutive monthly records, exporting 32 and 36 cargoes in November and December respectively.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved