Global Oil Balances Are Overwhelmingly Bullish

- WTI rose more than 44% in past six weeks

- Possible Russian invasion of Ukraine pricing into crude costs

- Inventories under pressure

- Natural gas futures have record short squeeze

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

West Texas Intermediate (WTI) crude oil futures were priced about $61.60 per barrel during the week ended Dec. 24, 2021. They reached $89.10 on Friday, Jan. 28 before recording a small loss for the day. WTI gained $27.50 for the six weeks, more than 44.5% higher overall.

The setback itself was likely the result of US dollar strength, making oil (priced in dollars) more expensive overseas, depressing demand. The underlying dynamics of global petroleum balances, however, remain overwhelmingly higher. Powerhouse has noted many times that both supply and demand are bullish with little to indicate longer-term weakness developing any time soon. This has been the basis of recent adjustments to forecasts of $100 crude oil in the not-too-distant future. Global demand has recovered to near-pre-pandemic levels notwithstanding weakening risk sentiment elsewhere in the economy.

The situation developing in Ukraine has thrown a spanner into price planning already fraught with uncertainty. The massing of troops on Ukraine/Russia borders has heighted tensions. Further escalation of military activity could result in a European oil supply shock. (Russia has denied plans to invade.) Traders appear to be pricing in a political risk premium of around five dollars.

Crude oil supply remains hobbled by problems in OPEC+ oil production. Libyan, Nigerian and Angolan availability offer little more than question marks. Overall, OPEC+ providers have not provided even the amounts of crude oil expected in their promised expansion of supply.

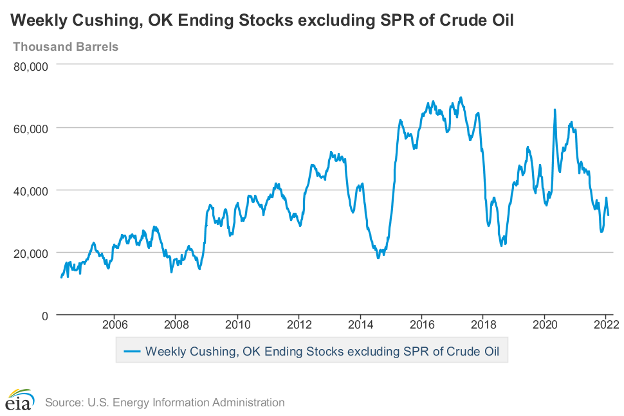

Cushing Crude Stocks 2006 – 2022 Source: EIA

Higher demand has eaten into inventories at Cushing OK. Stocks at this key location have fallen to the lowest level for this time of year, reportedly, in a decade.

Supply/Demand Balances

Supply/demand data in the United States for the week ended Jan. 21, 2022, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 4.1 million barrels during the week ended January 21, 2022.

Commercial crude oil supplies in the United States increased by 2.4 million barrels from the previous report week to 416.2 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Up 0.2 million barrels to 6.9 million barrels

PADD 2: Down 1.4 million barrels to 112.3 million barrels

PADD 3: Plus 2.4 million barrels to 222.5 million barrels

PADD 4: Down 0.1 million barrels to 23.2 million barrels

PADD 5: Plus 1.4 million barrels to 49.0 million barrels

Cushing, Oklahoma, inventories were down 1.8 million barrels from the previous report week to 31.7 million barrels.

Domestic crude oil production was down 100,000 per day from the previous report week at 11.6 million barrels daily.

Crude oil imports averaged 6.236 million barrels per day, a daily decrease of 509,000 barrels. Exports increased 186,000 barrels daily to 2.796 million barrels per day.

Refineries used 87.7% of capacity; 0.4 percentage points lower from the previous report week.

Crude oil inputs to refineries increased 44,000 barrels daily; there were 15.497 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 71,000 barrels daily to 15.897 million barrels daily.

Total petroleum product inventories fell 6.5 million barrels from the previous report week.

Gasoline stocks increased 1.3 million barrels from the previous report week; total stocks are 247.9 million barrels.

Demand for gasoline rose by 281,000 barrels per day to 8.505 million barrels per day.

Total product demand increased 502,000 barrels daily to 22.417 million barrels per day.

Distillate fuel oil stocks decreased 2.8 million barrels from the previous report week; distillate stocks are at 125.2 million barrels. EIA reported national distillate demand at 4.754 million barrels per day during the report week, an increase of 198,000 barrels daily.

Propane stocks decreased 4.6 million barrels from the previous report week; propane stocks are at 54.1 million barrels. The report estimated current demand at 2.190 million barrels per day, a decrease of 63,000 barrels daily from the previous report week.

Natural Gas

Natural gas futures advanced slowly and without incident during the latter half of January, after a sharp drop earlier in the month. On Wednesday, January 26, the spot February natural gas contract settled at $4.277. Prices advanced further on January 28, last trading day, and at 2 pm EST, posted $4.838.

Last trading day has an extended close from 2 pm until 2:30 pm. During this time, what had been a relatively calm market turned explosive. A short squeeze developed. Traders not taking or making delivery are required to exit positions before 2:30 pm. Here, holders of short futures who needed to buy contracts (or make delivery) were hostage to longs without that obligation.

This happened when open interest in the February natural gas contract had virtually disappeared. One observer noted, “The gas futures market has grown increasingly vulnerable to an event such as Thursday’s in the last three months, as surging volatility prompted some investors to withdraw, reducing overall liquidity.”

At 2:15 pm, halfway through the closing, prices reached $7.346. This surge, more than 70 percent, receded. The Bebruary contract’s final settlement was $6.265, nearly $2.00 higher than the previous day and not seen since October 2021.

The CME confirmed the price spiked the most since the 1990 launch of the natural gas contract. On Friday the now-spot March contract settled at $4.639 but the challenge to $7.35 has altered the market’s dynamics. The possibility of a new challenge to that resistance cannot be ignored.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved