2022 Demand Boom to Continue

- Global demand to reach 99.5 MMb/d

- U.S. demand not record-shattering

- Crude oil supply concerns

- LNG exports reach record levels

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Prices for West Texas Intermediate crude oil futures continued their recovery in 2021 as the economy responded to an improved pandemic situation. (The current Omicron variant appears to have had a mixed impact. Hospitalizations are near peak but deaths are steady and even falling in some jurisdictions.)

The year began with WTI futures at $48.40, ended at $75.21 last week, just $10 off the annual high of $85.41 seen in October.

Analysts are taking a bullish pose for 2022 too as consumption data surge, opening a possibility of a new global demand record this year.

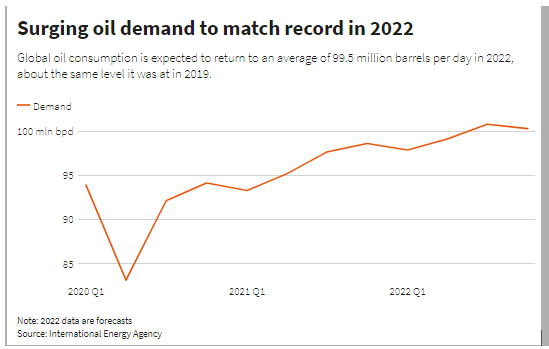

Oil Demand Projection 2021- Q1 2022 Source: International Energy Agency

The International Energy Agency (IEA) expects crude oil demand to reach 99.53 million barrels daily, an increase from 2021’s 96.2 million barrels per day.

Global demand growth is expected to center in Asia. Indonesia and Thailand are seen as strong candidates for increasing consumption. Asian demand for gasoline could grow by 350,000 barrels daily.

Demand for petroleum products in the United States was robust in 2021, but not record-shattering. The four weeks ended Dec. 24 showed demand at 21.4 million barrels per day, an increase over the same period in 2020 of 12.4%. This was well short of the record 21.7 million barrels per day in August 2019.

Jet fuel demand clocked in at 1.2 million daily barrels, 20.6% higher than last year at that time. This gain is a stark reminder of how devastating the pandemic has been on the aviation sector. (K-jet fuel demand fell to 648,000 barrels daily at its lowest during the four weeks ended June 5, 2020.)

Expectations of demand growth this year raise new concerns about the ability of producers to provide adequate supply. President Biden has called on OPEC+ to raise its output now after the group restrained supply for months. Underinvestment has plagued efforts to raise production. In November, OPEC+ provided even less than its reduced supply schedule. Some new supplies should come from Canada, Norway, Guyana and Brazil.

U.S. shale producers have recovered to some degree. EIA reported output at 11.8 million barrels per day, still below the maximum pre-Covid 13 million daily barrels previously reached in 2019. EIA expects U.S. production to weigh in at 11.9 million barrels per day in 2022.

Supply/Demand Balances

Supply/demand data in the United States for the week ended Dec. 24, 2021, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose 4.2 million barrels during the week ended Dec. 24, 2021.

Commercial crude oil supplies in the United States decreased by 3.6 million barrels from the previous report week to 420 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.6 million barrels to 8.2 million barrels

PADD 2: Plus 1.1 million barrels to 115 million barrels

PADD 3: Down 4.3 million barrels to 226.5 million barrels

PADD 4: Down 0.3 million barrels to 24.1 million barrels

PADD 5: Down 0.6 million barrels to 46.2 million barrels

Cushing, Oklahoma, inventories were up 1 million barrels from the previous report week to 34.7 million barrels.

Domestic crude oil production was up 200,000 barrels per day from the previous report week to 11.8 million barrels daily.

Crude oil imports averaged 6.759 million barrels per day, a daily increase of 565,000 barrels. Exports increased 50,000 barrels daily to 2.929 million barrels per day.

Refineries used 89.7% of capacity; 0.1 percentage points higher from the previous report week.

Crude oil inputs to refineries decreased 115,000 barrels daily; there were 15.703 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 20,000 barrels daily to 16.287 million barrels daily.

Total petroleum product inventories fell 15.3 million barrels from the previous report week.

Gasoline stocks decreased 1.5 from the previous report week; total stocks are 222.7 million barrels.

Demand for gasoline rose by 739,000 barrels per day to 9.724 million barrels per day.

Total product demand increased 1,764,000 barrels daily to 22.218 million barrels per day.

Distillate fuel oil stocks decreased 1.7 million barrels from the previous report week; distillate stocks are at 122.4 million barrels. EIA reported national distillate demand at 4.051 million barrels per day during the report week, an increase of 229,000 barrels daily.

Propane stocks decreased 3.6 million barrels from the previous report week; propane stocks are at 66.5 million barrels. The report estimated current demand at 1.746 million barrels per day, an increase of 552,000 barrels daily from the previous report week. Supply/demand data in the United States for the week ended Dec. 3, 2021, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose 4.2 million barrels during the week ending Dec. 3, 2021.

Commercial crude oil supplies in the United States decreased by 0.2 million barrels from the previous report week to 432.9 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 1.3 million barrels to 7.8 million barrels

PADD 2: Plus 1.1 million barrels to 114.4 million barrels

PADD 3: Plus 0.7 million barrels to 237.9 million barrels

PADD 4: Plus 0.3 million barrels to 23.9 million barrels

PADD 5: Down 1.2 million barrels to 48.8 million barrels

Cushing, Oklahoma, inventories were up 2.4 million barrels from the previous report week to 30.9 million barrels.

Domestic crude oil production was up 100,000 barrels per day from the previous report week to 11.7 million barrels daily.

Crude oil imports averaged 6.499 million barrels per day, a daily increase of 105,000 barrels. Exports decreased 434,000 barrels daily to 2.270 million barrels per day.

Refineries used 89.8% of capacity; 1 percentage points higher from the previous report week.

Crude oil inputs to refineries increased 154,000 barrels daily; there were 15.785 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 192,000 barrels daily to 16.287 million barrels daily.

Total petroleum product inventories rose 4.4 million barrels from the previous report week.

Gasoline stocks increased 3.9 million barrels from the previous report week; total stocks are 219.3 million barrels.

Demand for gasoline rose by 167,000 barrels per day to 8.963 million barrels per day.

Total product demand decreased 385,000 barrels daily to 19.837 million barrels per day.

Distillate fuel oil stocks increased 2.7 million barrels from the previous report week; distillate stocks are at 126.6 million barrels. EIA reported national distillate demand at 3.578 million barrels per day during the report week, a decrease of 631,000 barrels daily.

Propane stocks increased 0.6 million barrels from the previous report week; propane stocks are at 73.3 million barrels. The report estimated current demand at 1.615 million barrels per day, a decrease of 58,000 barrels daily from the previous report week.

Natural Gas

Natural gas futures made a third attempt to break support at $3.60 last Thursday. The down thrust was repulsed on the last trading day of 2021 by a half-hearted rally that became an inside day but held nearby support.

2021 was a strong year for natural gas prices overall, ranging from an opening of $2.414 to their close at $3.73. Prices reached $6.406 in October.

Part of natural gas’s recovery reflected the remarkable growth of LNG exports during the year. Exports reached record highs in the first half of 2021. New export capacity was commissioned at Freeport, Cameron, and Corpus Christi. Total export capacity peaked at 10.8 Bcf/d.

According to the EIA:

Working gas in storage was 3,226 Bcf as of Friday, Dec. 24, 2021, according to EIA estimates. This represents a net decrease of 136 Bcf from the previous week. Stocks were 250 Bcf less than last year at this time and 19 Bcf above the five-year average of 3,207 Bcf. At 3,226 Bcf, total working gas is within the five-year historical range.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved