ULSD Holds to Its Upward Course

- Inventories of liquid oils show little improvement

- Crude oil released from Strategic Petroleum Reserve continues a pattern

- Oil exports are expanding

- The United States is now the largest LNG exporter in the world.

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

Futures prices of ULSD rallied last week. A new high in price for the rally that began on August 9th was made on Thursday and the market finished out the week by holding on to the lion’s share of the advance.

Inventory remains tight, as it has all year. Days of distillate fuel oil supply remain below the five-year minimum. Early indications of a colder winter ahead are price supportive. And September is commonly a time for ULSD prices to advance.

Fig1

Product flows also conduce to higher price. Exports of distillate fuel oil reached 1.6 million barrels daily, higher than last year at this time, when outflows reached 1.1 million barrels per day, while domestic demand held steady at 3.9 million daily barrels.

More generally, the supply situation has shown little sign of improvement. Inventories of crude oil took a real shock when commercial supplies fell 3.3 million barrels daily for the week ended August 19. More significant, withdrawals from the Strategic Petroleum Reserve reached 8.1 million barrels daily during the report week.

Analysts have been attributing some of the drop in oil prices seen in recent months on planned releases from the SPR. The Ukrainian invasion by Russia six months ago has had many ramifications. Among them are needs to shift American oil to the EU, replacing Russian supplies. The SPR oil release may also have contributed to cooling inflation fears and helped gasoline prices continue to ease.

The SPR held 453 million barrels of crude oil last week, reportedly the lowest level since early 1985. The Reserve has lost more than 160 million barrels this year. The withdrawal is planned to continue.

The United States has urged other nations to contribute to the new supply. The IEA has estimated contributions to supply form others will add 60 million barrels to global supply. In all, 260 million barrels will have been added to markets by October.

The United States has urged other nations to contribute to the new supply. The IEA has estimated contributions to supply form others will add 60 million barrels to global supply. In all, 260 million barrels will have been added to markets by October.

Supply/Demand Balances

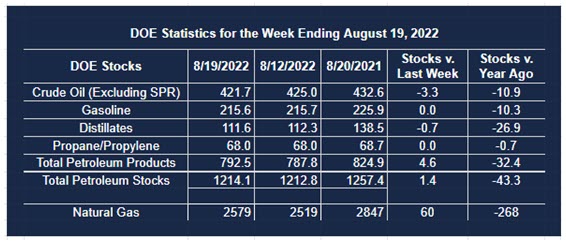

Supply/demand data in the United States for the week ended August 19, 2022, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose 1.4 million barrels during the week ended August 19, 2022.

Commercial crude oil supplies in the United States decreased by 3.3 million barrels from the previous report week to 421.7 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.1 million barrels to 8.0 million barrels

PADD 2: Plus 0.9 million barrels to 109.4 million barrels

PADD 3: Down 1.8 million barrels to 233.1 million barrels

PADD 4: Down 0.6 million barrels to 22.7 million barrels

PADD 5: Down 2.0 million barrels to 50.4 million barrels

Cushing, Oklahoma, inventories were up 0.4 million barrels from the previous report week to 25.8 million barrels.

Domestic crude oil production was down 100,000 barrels per day from the previous report week to 12.1 million barrels daily.

Crude oil imports averaged 6.171 million barrels per day, a daily increase of 40,000 barrels. Exports decreased 823,000 barrels daily to 4.177 million barrels per day.

Refineries used 93.8% of capacity; 0.3 percentage points higher than the previous report week.

Crude oil inputs to refineries decreased 168,000 barrels daily; there were 16.255 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 43,000 barrels daily to 16.826 million barrels daily.

Total petroleum product inventories rose by 4.7 million barrels from the previous report week, rising to 795.8 million barrels.

Total product demand decreased 1,882,000 barrels daily to 19.339 million barrels per day.

Gasoline stocks were unchanged from the previous report week; total stocks are 215.6 million barrels.

Demand for gasoline fell 914,000 barrels per day to 8.434 million barrels per day.

Distillate fuel oil stocks decreased 0.7 million barrels from the previous report week; distillate stocks are at 111.6 million barrels. EIA reported national distillate demand at 3.888 million barrels per day during the report week, a decrease of 37,000 barrels daily.

Propane stocks were UNCH from the previous report week at 68.0 million barrels. The report estimated current demand at 763,000 barrels per day, an decrease of 202,000 barrels daily from the previous report week.

Natural Gas

On Tuesday, August 23, spot futures moved briefly above $10 before finishing the day just off its lows. Ten dollars per MMBtu was a new high for the contract, reportedly the highest price recorded in about fourteen years

Higher prices reflected surging European anxiety about winter gas supply. The reversal came in response to news that recovery of supply from Freeport LNG has been put off until mid-November, when two Bcf/d of new supply is expected to become available. The balance of the week had small ranges and no directionality. Near-term weather events might move prices, but no other large-scale action is on the horizon.

An improved US supply situation is expected, looking further out. EIA has reported that the seventh US LNG export facility, Calcasieu Pass LNG has placed all its liquefaction trains in service.

The United States is now the largest LNG exporter in the world. Exports averaged 11.1 Bcf/d in the first six months of 2022. The worrisome situation in the EU has opened a large market for American natural gas. Asia is still a large off taker.

According to the EIA:

Net injections [of natural gas] into storage totaled 60 Bcf for the week ended August 19, compared with the five-year (2017–2021) average net injections of 46 Bcf and last year’s net injections of 32 Bcf during the same week. Working natural gas stocks totaled 2,579 Bcf, which is 353 Bcf (12%) lower than the five-year average and 268 Bcf (9%) lower than last year at this time.

The average rate of injections into storage is 6% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 9.8 Bcf/d for the remainder of the refill season, the total inventory would be 3,292 Bcf on October 31, which is 353 Bcf lower than the five-year average of 3,645 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2022 Powerhouse Brokerage, LLC, All rights reserved