Mixed Signals on The Economy and Oil Supply/Demand Press Prices Lower

- Uncertainty abounds on oil price trends

- Trade war with China heats up

- Consumer Sentiment falls to recent lows

- Natural gas bullish divergence may be developing

The Matrix

Petroleum prices are reacting to a wide range of factors in the economy and the industry. Efforts to limit Iranian crude oil exports, instability in Libya, deep cuts in Venezuelan production support the bull case. Expanding crude oil and natural gas production in the United States provide a bearish counter.

Robust involvement from the White House has thrown a spanner into the works. China threatened to impose tariffs on imports of crude oil from the U.S. This pressured prices lower. The President responded by ordering U.S. companies to close their operations in China, a power he does not have. The oil markets reacted vigorously, prices trending lower overall.

The trading community reacted uncertainly. Volatilities expanded and option premiums expanded. Prices moved generally lower, but the possibility of bullish news could not be ignored.

This has become a classic example of why one hedges. The industry cannot influence the elements that create price trends, but it can be affected by them. The proper financial instrument allows a hedger to at least fix a price with a futures contract, cap purchase prices with a call or, conversely, establish a floor for supply already owned and priced with a put.

The Consumer Sentiment Index reportedly fell to its second-lowest level since before the 2016 election, evidence of anxiety over the direction of the economy. Tariffs in the trade war are being seen as inflationary. Consumers should expect reduced buying power and lower spending.

Consumer Sentiment, when measured by political affiliation, can be an important economic indicator. Recent data show both Republicans and independents losing confidence in the economy at sharp rates of decline. Independents were optimistic at the beginning of the Trump era. That level has fallen to its lowest level of this administration.

Ironically, loss of confidence in the economy comes while demand for petroleum in the United States was strong. Through July, total demand reached 20.4 million barrels daily. This was the highest since 2007 according to the American Petroleum Industry.

Supply/Demand Balances

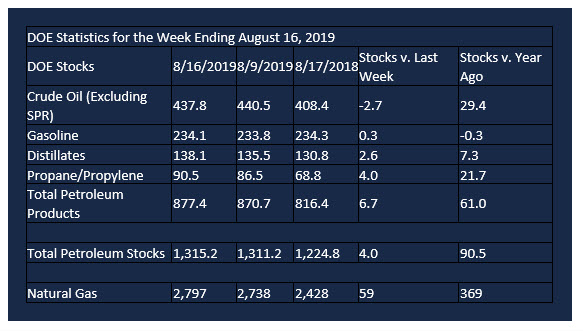

Supply/demand data in the United States for the week ending August 16, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum increased by 4.0 million barrels during the week ending August 16, 2019.

There were builds in stocks of gasoline, distillate fuel, other oils, and propane. There were draws in stocks of fuel ethanol, K-jet fuel, and residual fuel oil.

Commercial crude oil supplies in the United States rose 2.7 million barrels from the previous report week to 437.8 million barrels.

Crude oil supplies increased in two of the five PAD Districts. PAD District 1 (East Coast) crude oil stocks rose 0.5 million barrels and PAD District 3 (Gulf Coast) crude stocks rose 0.6 million barrels. PADD 2 (Midwest) stocks fell 2.6 million barrels, and PADD 5 (West Coast) stocks fell 1.3 million barrels. PADD 4 (Rockies) storage was unchanged at 20.5 million barrels.

Cushing, Oklahoma inventories fell 2.5 million barrels from the previous report week to 42.3 million barrels.

Domestic crude oil production remained at 12.3 million barrels daily for the third consecutive week.

Crude oil imports averaged 7.218 million barrels per day, a daily decrease of 497,000 barrels. Exports rose 120,000 barrels daily to 2.803 million barrels per day.

Refineries used 95.9 percent of capacity, up 1.1% from the previous report week.

Crude oil inputs to refineries increased 400,000 barrels daily; there were 17.702 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, added 212,000 barrels daily to reach 18.038 million barrels daily.

Total petroleum product inventories rose 6.8 million barrels from the previous report week.

Gasoline stocks increased 0.3 million barrels daily from the previous report week; total stocks are 234.1 million barrels.

Demand for gasoline fell 305,000 barrels per day to 9.626 million barrels per day.

Total product demand dropped 1.091 million barrels daily to 20.987 million barrels per day.

Distillate fuel oil stocks increased 2.6 million barrels from the previous report week; distillate stocks are at 138.1 million barrels. EIA reported national distillate demand at 3.758 million barrels per day during the report week, a decrease of 101,000 barrels daily.

Propane stocks increased 4.0 million barrels from the previous report week; propane stocks are 90.5 million barrels. The report estimated current demand at 938,000 barrels per day, a decrease of 62,000 barrels daily from the previous report week.

Natural Gas

Last week’s EIA storage report showed injections of 59 Bcf. The pattern of current storage slowly erasing its deficit against previous years continues. Powerhouse’s David Thompson, CTA has issued a technical note suggesting that natural gas bullish divergence may be developing. This situation occurs when price moves lower while a supporting statistic like MACD starts to establish a bottom.

David notes: “The divergence between the price action and the technical indicator may highlight the decay of the existing market dynamic. For example, the bears have been in control for some time, but each push lower in price occurs with less intensity. Identifying these changing internal characteristics of a market can be useful for market participants in their decision-making.”

According to the Energy Information Administration:

Net injections into storage totaled 59 Bcf for the week ending August 16, compared with the five-year (2014–18) average net injections of 51 Bcf and last year’s net injections of 47 Bcf during the same week. Working gas stocks totaled 2,797 Bcf, which is 103 Bcf lower than the five-year average and 369 Bcf more than last year at this time.

The average rate of net injections into storage is 31% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.4 Bcf/d for the remainder of the refill season, total inventories would be 3,589 Bcf on October 31, which is 103 Bcf lower than the five-year average of 3,692 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.