Oil Fundamentals Reassert Themselves

- Gasoline demand reached 9.9 million barrels per day

- Hurricane season picks up new prospects

- Crude oil stocks growing on Texas Gulf Coast

- Natural gas reaches record production rate

The Matrix

Broad economic factors have overwhelmingly influenced crude oil prices in recent months. The trade conflict between the United States and China has, in particular, shaped supply and price expectations.

Statistics within the petroleum sector strongly reasserted themselves last week. Gasoline demand reached 9.9 million barrels daily as reported in the EIA supply/demand data for the week ending August 9, 2019. This was a record level; the United States has never reached ten million barrels per day of gasoline usage. Jet fuel use challenged its record too, with use of 2.0 million barrels daily.

The explanation for record implied gasoline demand includes lower import levels. At the same time, however, RBOB inventories increased. This is a bearish sign that has held prices in check.

The current hurricane season has been quiet. Weather experts have attributed this to dry, dusty Saharan winds. This weather situation took moisture and wind shear from potential storms. These features are now gone, perhaps a precursor to a more active pattern as September approaches.

A more active pattern could still mean 10 to 17 named storms impacting petroleum interests in the Gulf of Mexico. And the Gulf is home to nearly half of U.S. refining.

Crude oil stocks on the Texas gulf coast are expanding. Exporters have proposed several offshore oil export terminals. These facilities can be found from Brownsville, Texas into Louisiana. Currently available locations are crowded with supplies from the Permian Basin and can’t load tankers efficiently. A crude oil backup has developed and pricing more resembles distress values which could last well into 2020.

Supply/Demand Balances

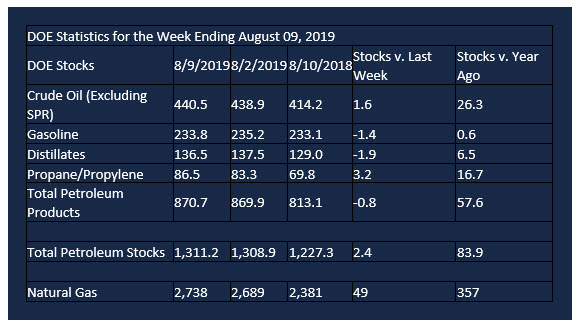

Supply/demand data in the United States for the week ending August 9, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose 2.4 million barrels during the week ending August 9, 2019.

There were draws in stocks of gasoline, K-jet fuel, distillate fuel, residual fuel, and propane. There were builds in stocks of fuel ethanol, crude oil and other oils.

Commercial crude oil supplies in the United States rose 1.6 million barrels from the previous report week to 440.5 million barrels.

Crude oil supplies decreased in one of the five PAD Districts. PAD District 2 (Midwest) crude oil stocks declined 3.4 million barrels. PADD 1 (East Coast) stocks rose 0.5 million barrels. PADD District 3 (Gulf Coast) crude stocks rose 1.8 million barrels, PADD 4 (Rockies) stocks increased 0.4 million barrels, and PADD 5 (West Coast) stocks grew 2.2 million barrels.

Cushing, Oklahoma inventories fell 2.6 million barrels from the previous report week to 44.8 million barrels.

Domestic crude oil production remained at 12.3 million barrels per day.

Crude oil imports averaged 7.714 million barrels per day, a daily increase of 566,000 barrels. Exports rose 818,000 barrels daily to 2.683 million barrels per day.

Refineries used 94.8 percent of capacity, down 1.6 percentage points from the previous report week.

Crude oil inputs to refineries fell 475,000 barrels daily; there were 17.302 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 291,000 barrels daily to 17.826 million barrels daily.

Total petroleum product inventories fell 3.8 million barrels from the previous report week.

Gasoline stocks dropped 1.4 million barrels daily from the previous report week; total stocks are 233.8 million barrels.

Demand for gasoline rose 281,000 barrels per day to 9.932 million barrels per day.

Total product demand increased 597,000 barrels daily to 22.078 million barrels per day.

Distillate fuel oil stocks fell 2.0 million barrels from the previous report week; distillate stocks are at 135.5 million barrels. EIA reported national distillate demand at 3.859 million barrels per day during the report week, a decrease of 27,000 barrels daily.

Propane stocks increased 3.2 million barrels from the previous report week; propane stocks are 86.5 million barrels. The report estimated current demand at 1.0 million barrels per day, an increase of 239,000 barrels daily from the previous report week.

Natural Gas

The best cure for low prices is low prices. This industry aphorism is apparently not working for natural gas just now. The Department of Energy reported that natural gas production is at record highs at the same time prices struggle to maintain $2.00 per mmBtu. A new daily record was reported on August 5 of 92.1 billion cubic feet. The Northeast provided most of the new production, accounting for 34 percent of national output.

Growing stocks of LNG appear to be adding to the inventory glut. Maritime observers note that LNG tankers are slow steaming. Voyages are apparently taking longer than usual to complete and could also mean storage of LNG at sea.

According to the Energy Information Administration:

Net injections into storage totaled 49 Bcf for the week ending August 9, compared with the five-year (2014–18) average net injections of 49 Bcf and last year’s net injections of 35 Bcf during the same week. Working gas stocks totaled 2,738 Bcf, which is 111 Bcf lower than the five-year average and 357 Bcf more than last year at this time.

The average rate of net injections into storage is 32% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.2 Bcf/d for the remainder of the refill season, total inventories would be 3,581 Bcf on October 31, which is 111 Bcf lower than the five-year average of 3,692 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.