Energy Futures Prices Push Higher

- Gasoline marks a new high

- ULSD stocks becoming tighter

- Crude oil producers add to supply

- Natural gas injections lag

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Core energy futures, traded on NYMEX, ended July trading pushing into resistance. RBOB set a new high, terminating the August futures contract at $2.3659. Futures have not reached this level since October 2014.

ULSD contracts were pulled higher. ULSD ended its term at $2.1994, just shy of $2.20 resistance. ULSD was last at this level in November 2018. Next resistance is at $2.45.

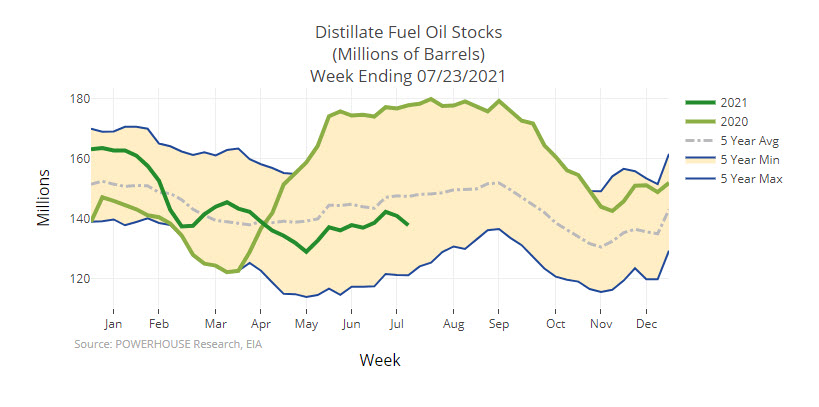

Distillate Fuel Oil Stocks – 5-Year Trend 2016 – 2021 Source: EIA, Powerhouse

Distillate fuel oil stocks have declined in 2021. Inventories started the year at 158.4 million barrels. They fell 20.5 million barrels by the end of July.

WTI, already trading a September contract, ended July at $73.95. Prices have now gained $6.30 in the prior nine trading days.

Evaluation of the market is never easy. The task has become more challenging. Prices have been moving higher for several months, reflecting satisfaction of a good deal of pent-up demand.

Refinery throughput declined significantly, falling to 67.4% of capacity in March 2021. Most recently, usage has recovered, clocking in at 91.6% of capacity, slightly lower than refining at this time in 2019. Current levels of distillate fuel oil stocks remain tight. ULSD supply is now 137.9 million barrels, more than 40 million barrels less than last year at this time.

Refinery Utilization – 4 Week Avg 1990 – 2021 Source: EIA

These data support a bullish view of prices, supported by Powerhouse for several months. Our expectations have been made more problematic by the pandemic and action by crude oil producers. The development of variant Delta has increased the likelihood of COVID-19 infection.

OPEC+ has announced an increase in crude oil supply. The increase is small but cannot be ignored as suggesting the next steps for OPEC+. North American producers appear to have settled in around 11.2 million barrels per day, always a possibility to policymakers looking for more crude oil output.

Supply/Demand Balances

Supply/demand data in the United States for the week ended July 23, 2021, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 6.5 million barrels during the week ended July 23, 2021.

Commercial crude oil supplies in the United States decreased by 4.1 million barrels from the previous report week to 435.6 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.4 to 9.3 million barrels

PADD 2: Down 0.4 million barrels to 118.6 million barrels

PADD 3: Plus 0.2 million barrels to 238.6 million barrels

PADD 4: Down 0.3 million barrels to 23.9 million barrels

PADD 5: Down 3.9 million barrels to 45.2 million barrels

Cushing, Oklahoma, inventories were down 1.3 million barrels from the previous report week to 35.4 million barrels.

Domestic crude oil production was down 0.2 million barrels per day from the previous report week to 11.2 million barrels daily.

Crude oil imports averaged 6.507 million barrels per day, a daily decrease of 590,000 barrels. Exports increased 26,000 barrels daily to 2.489 million barrels per day.

Refineries used 91.1% of capacity; 0.3 percentage points lower from the previous report week.

Crude oil inputs to refineries decreased 132,000 barrels daily; there were 15.875 million barrels of crude oil run to facilities per day. Gross inputs, which include blended stocks, fell 54,000 barrels daily to 16.569 million barrels daily.

Total petroleum product inventories fell 2.4 million barrels from the previous report week.

Gasoline stocks decreased 2.3 million barrels from the previous report week; total stocks are 234.2 million barrels.

Demand for gasoline rose 29,000 barrels per day to 9.325 million barrels per day.

Total product demand increased 542,000 barrels daily to 21.123 million barrels per day.

Distillate fuel oil stocks fell 3.1 million barrels from the previous report week; distillate stocks are at 137.9 million barrels. EIA reported national distillate demand at 4.356 million barrels per day during the report week, an increase of 430,000 barrels daily.

Propane stocks rose 1.9 million barrels from the previous report week; propane stocks are now 64.5 million barrels. The report estimated current demand at 622,000 barrels per day, a decrease of 162,000 barrels daily from the previous report week.

Natural Gas

Natural gas supply is failing to reach injection levels recorded last year or over the past five years. New demand is outstripping availability, especially for power.

According to the EIA:

The net injections [of natural gas] into storage totaled 36 Bcf for the week ended July 23, compared with the five-year (2016–2020) average net injections of 28 Bcf and last year’s net injections of 27 Bcf during the same week. Working natural gas stocks totaled 2,714 Bcf, which is 168 Bcf lower than the five-year average and 523 Bcf lower than last year at this time.

The average rate of injections into storage is 13% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.4 Bcf/d for the remainder of the refill season, the total inventory would be 3,551 Bcf on October 31, which is 168 Bcf lower than the five-year average of 3,719 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved