Global Supply Tightening; Demand Slowing

- OPEC+ production cut successful

- Purposeful crude oil cut supplemented by operational problems

- Economic growth in China is slowing

- Rally in natural gas seems unlikely

The Matrix

Oil prices react to a steady stream of bullish supply news. At the same time, however, analysts are showing concern for the continuing health of consumption. Supply constraints are appearing in overseas producing areas with some surprises.

The production cut of OPEC + has been in place for some time and has been remarkably successful. Notably, Saudi Arabia cut its production in March, 2019 to 9.9 million barrels daily. The Kingdom’s baseline for measuring its cut performance is 10.6 million barrels per day. On that basis, Saudi Arabia’s reduction yields a compliance cut of 733,000 barrels per day.

In all, OPEC reported reduced production of 1.099 million barrels daily compared with October, 2018. The group had pledged to reduce production by 812,000 barrels daily. This yields a compliance of 135 per cent.

Not all of the decline was attributable to OPEC compliance. Venezuela experienced production declines estimated by some to as low as 650,000 daily barrels.

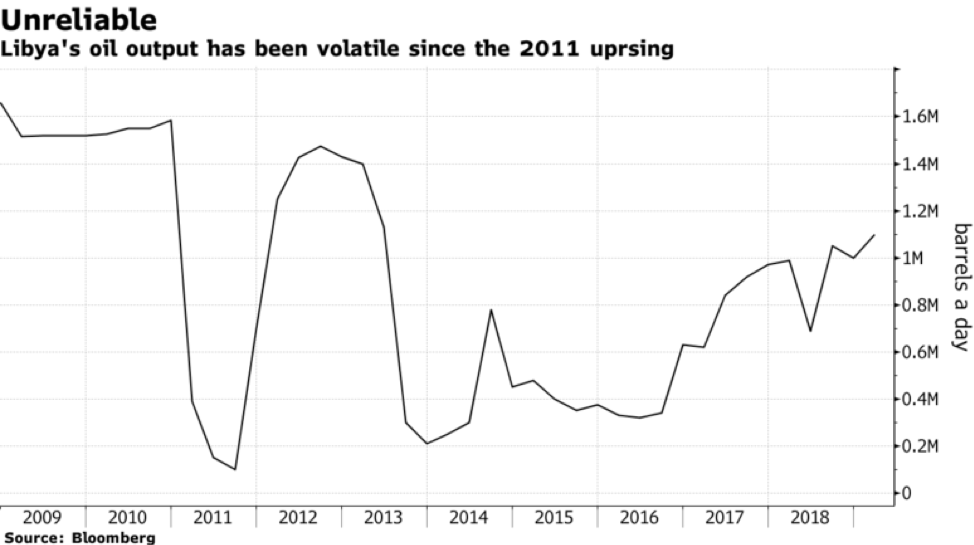

OPEC’s largest March production gain came from Libya, reflecting restart of El Sharara, the country’s largest oilfield. Ironically, one month later, in April, the news was all about Libya’s renewed fighting, threatening that same supply.

Libyan Oil Output 2009 – 2019 source: Bloomberg Global demand for fuels is coming largely from Asia. But Chinese economic growth is forecast to slow to 6.2 per cent. This would be China’s lowest growth rate in “nearly” thirty years. The IEA has pointed to consumption in developed nations falling in the fourth quarter of 2018 for the first time since 2014.

The U.S.’s general economy could also be affected negatively by higher oil prices. The U.S. government has been urging OPEC to expand production to reduce the effect of lower output in Venezuela and Iran.

Supply/Demand Balances

Supply/demand data in the United States for the week ending April 5, 2019 were released by the Energy Information Administration.

Total commercial stocks of petroleum increased 4.1 million barrels during the week ending April 5, 2019.

There were draws in stocks of gasoline, fuel ethanol, distillates, and residual fuel. There were builds in stocks of K-jet fuel, propane, and other oils.

Commercial crude oil supplies in the United States increased 7.0 million barrels from the previous report week to 456.6 million barrels.

Crude oil supplies increased in three of the five PAD Districts. PADD 3 (Gulf Coast) stocks rose 5.4 million barrels, PADD 4 (Rockies) stocks grew 0.8 million barrels, and PADD 5 (West Coast) stocks increased 1.7 million barrels. PAD District 1 (East Coast) crude oil stocks fell 0.5 million barrels and PADD 2 (Midwest) crude stocks declined 0.4 million barrels.

Cushing, Oklahoma inventories decreased 1.1 million barrels from the previous report week to 46.0 million barrels.

Domestic crude oil production was unchanged from the previous report week at 12.2 million barrels per day.

Crude oil imports averaged 6.599 million barrels per day, a daily decrease of 164,000 barrels. Exports decreased 374,000 barrels daily to 2.349 million barrels per day.

Refineries used 87.5 per cent of capacity, an increase of 1.1 percentage points from the previous report week.

Crude oil inputs to refineries increased 251,000 barrels daily; there were 16.100 million barrels per day of crude oil run to facilities.

Gross inputs, which include blending stocks, rose 329,000 barrels daily to 16.407 million barrels daily.

Total petroleum product inventories fell 2.9 million barrels from the previous report week.

Gasoline stocks decreased 7.7 million barrels daily from the previous report week; total stocks are 229.1 million barrels.

Demand for gasoline increased 676,000 barrels per day to 9.806 million barrels per day.

Total product demand increased 317,000 barrels daily to 20.316 million barrels per day.

Distillate fuel oil stocks decreased 0.1 barrels from the previous report week; distillate stocks are at 128.1 million barrels. National distillate demand was reported at 3.779 million barrels per day during the report week. This was a weekly decrease of 378,000 barrels daily.

Propane stocks increased 1.2 million barrels from the previous report week; propane stock are 54.4 million barrels. Current demand is estimated at 941,000 barrels per day, an increase of 93,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 25 Bcf for the week ending April 5, compared with the five-year (2014–18) average net injections of 5 Bcf and last year’s net withdrawals of 20 Bcf during the same week. Working gas stocks totaled 1,155 Bcf, which is 485 Bcf lower than the five-year average and 183 Bcf lower than last year at this time.

Working natural gas in storage in the Lower 48 states as of March 31, the traditional end of the heating season (November 1–March 31), totaled 1,137 billion cubic feet (Bcf.) As of March 31, working natural gas stocks were 491 Bcf (30%) lower than the five-year (2014–18) average for the end of the heating season. This heating season ended at the lowest level for working natural gas stocks since 2014, when working natural gas stocks totaled 837 Bcf. Last year, working natural gas stocks ended the winter at 1,360 Bcf.

This week’s natural gas injection was bullish – less than expected. It did not, however, lead to a price rally. Analysts are questioning whether natural gas will trade over $3 per mmBtu this summer. And as offtake capacity becomes available, even more price pressure can be expected. These analysts estimate that the “breakeven figure for production is around 92 Bcf per day.” Higher output could set up the next natural gas glut.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this memo helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.