Forecast Highlights

Release Date: August 6, 2019

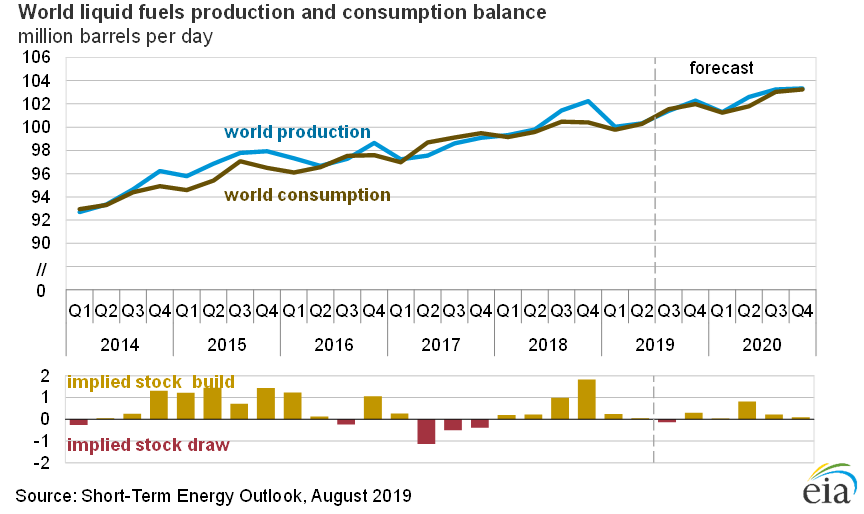

Global liquid fuels

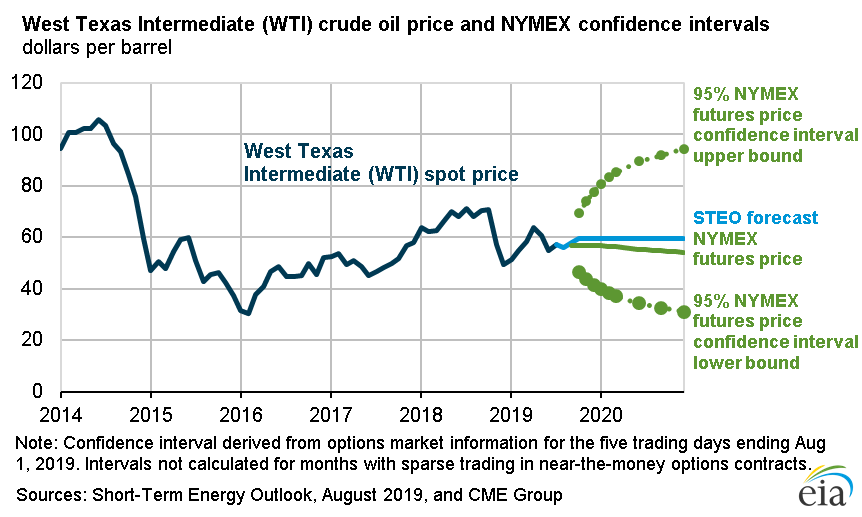

- Brent crude oil spot prices averaged $64 per barrel (b) in July, almost unchanged from the average in June 2019 but $10/b lower than the price in July of last year. EIA forecasts Brent spot prices will average $64/b in the second half of 2019 and $65/b in 2020. The forecast of stable crude oil prices is the result of EIA’s expectations of a relatively balanced global oil market. EIA forecasts global oil inventories will increase by 0.1 million barrels per day (b/d) in 2019 and 0.3 million b/d in 2020.

- EIA expects West Texas Intermediate (WTI) crude oil prices will average $5.50/b less than Brent prices during the fourth quarter of 2019 and in 2020, narrowing from the $6.60/b spread during July. The narrowing spread reflects EIA’s assumption that crude oil pipeline transportation constraints from the Permian Basin to refineries and export terminals on the U.S. Gulf Coast will ease in the coming months. In the July STEO, EIA forecast the Brent-WTI spread to average $4.00/b in 2020. The updated differential forecast reflects EIA’s revised assumptions about the marginal cost of moving crude oil via pipeline from Cushing, Oklahoma, to the Gulf Coast.

- EIA estimates that U.S. crude oil production averaged 11.7 million b/d in July, down by 0.3 million b/d from the June level. The declines were mostly in the Federal Gulf of Mexico (GOM), where operators shut platforms for several days in mid-July because of Hurricane Barry. EIA estimates that GOM crude oil production fell by more than 0.3 million b/d in July. Those declines were partially offset by the Lower 48 States onshore region, which is mostly tight oil production, where supply rose by more than 0.1 million b/d. EIA expects monthly growth in Lower 48 onshore production to slow during the rest of the forecast period, averaging 50,000 b/d per month from the fourth quarter of 2019 through the end of 2020, down from an average of 110,000 b/d per month from August 2018 through July 2019. EIA forecasts U.S. crude oil production will average 12.3 million b/d in 2019 and 13.3 million b/d in 2020, both of which would be record levels.

- U.S. regular gasoline retail prices averaged $2.74 gallon (gal) in July, up 2 cents/gal from June but 11 cents/gal lower than the average in July of last year. EIA expects that monthly average gasoline prices peaked for the year in May at an average of $2.86/gal and will fall to an average of $2.64/gal in September. EIA expects regular gasoline retail prices to average $2.62/gal in 2019 and $2.71/gal in 2020.

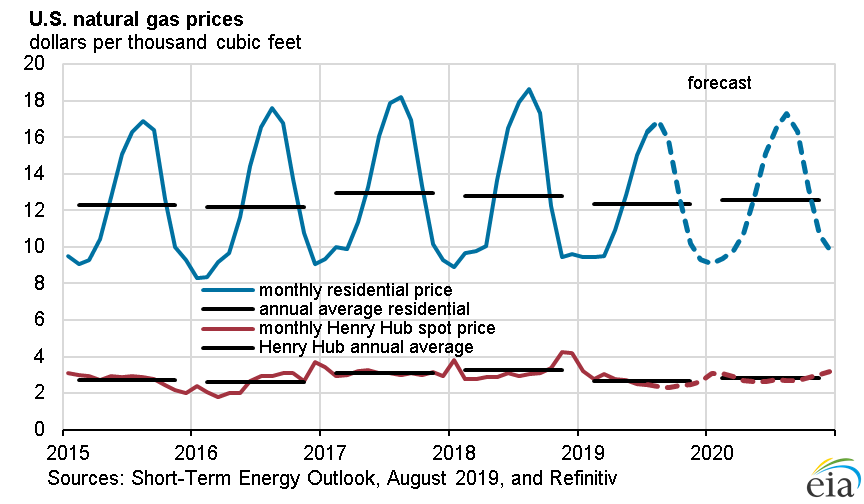

Natural gas

- The Henry Hub natural gas spot price averaged $2.37/million British thermal units (MMBtu) in July, down 3 cents/MMBtu from June. However, by the end of the month, spot prices had fallen below $2.30/MMBtu. Based on this price movement and EIA’s forecast of continued strong growth in natural gas production, EIA lowered its Henry Hub spot price forecast for the second half of 2019 to an average of $2.36/MMBtu. In the July STEO, EIA expected prices to average $2.50/MMBtu during this period. EIA expects natural gas prices in 2020 will increase to an average of $2.75/MMBtu. EIA’s natural gas production models indicate that rising prices are required in the coming quarters to bring supply into balance with rising domestic and export demand in 2020.

- EIA forecasts that U.S. dry natural gas production will average 91.0 billion cubic feet per day (Bcf/d) in 2019, up 7.6 Bcf/d from 2018. EIA expects monthly average natural gas production to grow in late 2019 and then decline slightly during the first quarter of 2020 as the lagged effect of low prices in the second half of 2019 reduces natural gas-directed drilling. However, EIA forecasts that growth will resume in the second quarter of 2020, and natural gas production in 2020 will average 92.5 Bcf/d.

- EIA estimates that natural gas inventories ended July at 2.7 trillion cubic feet (Tcf), 13% higher than levels from a year earlier and 4% lower than the five-year (2014–18) average. EIA forecasts that natural gas storage injections during the 2019 April-through-October injection season will outpace the previous five-year average and that inventories will rise to more than 3.7 Tcf at the end of October, which would be 16% higher than October 2018 levels and slightly above to the five-year average.