Principal contributor: Jesse Barnett

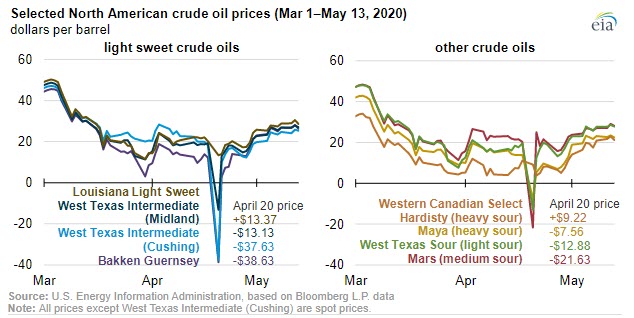

The New York Mercantile Exchange (NYMEX) front-month futures contract for West Texas Intermediate (WTI), the most heavily used crude oil price benchmark in North America, saw its largest and swiftest decline ever on April 20, 2020, dropping as low as -$40.32 per barrel (b) during intraday trading before closing at -$37.63/b. Prices have since recovered, and even though the market event proved short-lived, the incident is useful for highlighting the interconnectedness of the wider North American crude oil market.

Changes in the NYMEX WTI price can affect other price markers across North America because of physical market linkages such as pipelines—as with the WTI Midland price—or because a specific price is based on a formula—as with the Maya crude oil price. This interconnectedness led other North American crude oil spot price markers to also fall below zero on April 20, including WTI Midland, Mars, West Texas Sour (WTS), and Bakken Clearbrook. However, the usefulness of the NYMEX WTI to crude oil market participants as a reference price is limited by several factors.

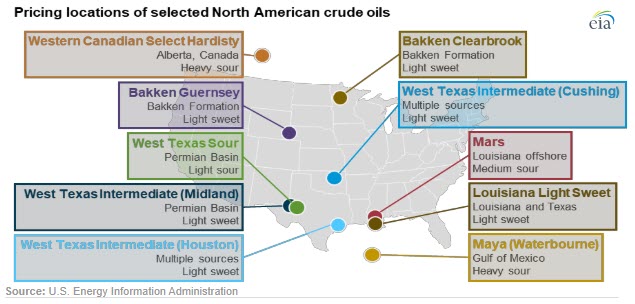

First, NYMEX WTI is geographically specific because it is physically redeemed (or settled) at storage facilities located in Cushing, Oklahoma, and so it is influenced by events that may not reflect the wider market. The April 20 WTI price decline was driven in part by a local deficit of uncommitted crude oil storage capacity in Cushing. Similarly, while the price of the Bakken Guernsey marker declined to -$38.63/b, the price of Louisiana Light Sweet—a chemically comparable crude oil—decreased to $13.37/b.

Second, NYMEX WTI is chemically specific, meaning to be graded as WTI by NYMEX, a crude oil must fall within the acceptable ranges of 12 different physical characteristics such as density, sulfur content, acidity, and purity. NYMEX WTI can therefore be unsuitable as a price for crude oils with characteristics outside these specific ranges.

Finally, NYMEX WTI is time specific. As a futures contract, the price of a NYMEX WTI contract is the price to deliver 1,000 barrels of crude oil within a specific month in the future (typically at least 10 days). The last day of trading for the May 2020 contract, for instance, was April 21, with physical delivery occurring between May 1 and May 31. Some market participants, however, may prefer more immediate delivery than a NYMEX WTI futures contract provides. Consequently, these market participants will instead turn to shorter-term spot price alternatives.

Taken together, these attributes help to explain the variety of prices used in the North American crude oil market. These markers price most of the crude oils commonly used by U.S. buyers and cover a wide geographic area.