Oil prices and stock markets have been moving back up this week, though the country remains on tenterhooks over the U.S. presidential election. Former Vice President Joe Biden holds a narrow lead over President Donald Trump, but votes are still being counted. As this plays out, the country is freshly alarmed over surging COVID-19 cases. New daily cases of COVID-19 shattered records by topping 100,000 on both Wednesday and Thursday. Health experts warn that the coming of winter and the holiday season could worsen the spread as people visit family and socialize more indoors. Today, WTI crude futures prices opened at $38.54 a barrel today. Prices have been tapering down this morning, and they retreated below $38 a barrel. Still, oil prices appear to be heading for a finish in the black this week, recouping a portion of last week’s hefty losses. The Dow Jones Industrial Average also bounced back this week, though early indicators point to a slight pullback today.

COVID-19 cases are surging. Deaths exceed 1.23 million globally. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 48,600,362, with 1,232,209 deaths. Confirmed cases in the U.S. have risen to 9,606,369. U.S. deaths attributed to the disease have reached 234,911. The U.S. is in the grips of another surge. At this point, there is no state in the union that can claim to have the disease under control. Nationwide, new cases on Wednesday exceeded 103,000, a new record smashed the next day when new cases hit 116,255. According to the COVID Tracking Project, states reported that the Wednesday-to-Wednesday week brought a 20% increase in new cases, a 14% increase in hospitalizations, and an 8% increase in deaths.

The Bureau of Labor Statistics (BLS) released the Employment Situation Report, also known as the Jobs Report, for October this morning. Total nonfarm payroll employment grew by 638,000 in October. The unemployment rate fell to 6.9%. According to the BLS: “These improvements in the labor market reflect the continued resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. In October, notable job gains occurred in leisure and hospitality, professional and business services, retail trade, and construction. Employment in government declined.”

initial weekly unemployment claims declined modestly last week. According to data collected by the Department of Labor, initial claims totaled 751,000 during the week ended October 24, down by 7,000 from the prior week’s upward-revised figure of 758,000. Initial weekly claims finally subsided below the one-million mark at the end of August, but they had been stuck stubbornly above 800,000 until just the past three weeks. Prior to the pandemic, initial claims were typically 200,000–220,000 each week.

Shell announced that it has been unable to sell its 240,000-bpd refinery in Convent, Louisiana, and the company has decided to close it by February 2021. The refinery still will be listed for sale in case a buyer can be found. Shell’s strategic plan globally has been to cut standalone refineries in favor of facilities that integrate refining, petrochemicals, and biofuels. The Louisiana refinery has suffered from poor margins, and it has been battered by hurricanes and storms.

WTI crude futures prices opened at $38.54 a barrel today, up by $2.47 a barrel (6.8%) from last Friday’s open of $36.07 a barrel. WTI futures prices are in the neighborhood of $37.50-$38.50 a barrel currently. Prices are heading for a finish in the red. Our weekly price review covers hourly forward prices from Friday, October 30 through Friday, November 6. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

Gasoline Prices

Gasoline futures prices opened at $1.114 a gallon today on the NYMEX, compared with $1.0264 a gallon last Friday. This was a recovery of 8.76 cents (8.5%,) climbing back after last week’s collapse of 10.53 cents (9.1%). The beginning of COVID-19 shelter-in-place programs in March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. October brought a price retreat. U.S. average retail prices for gasoline declined by 0.31 cents to average $2.112/gallon during the week ended November 2. Retail prices reclaimed the territory above $2 per gallon during the first week of June. Gasoline futures are trading in the range of $1.0848/gallon to $1.114/gallon. The week is heading for a finish in the black, recovering some of last week’s losses. The latest price is $1.0942/gallon.

Source: Prices as reported by DTN Instant Market

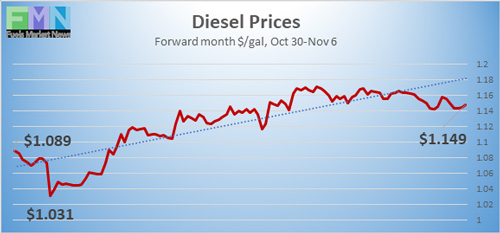

Diesel Prices

Diesel opened on the NYMEX today at $1.1675/gallon, up significantly by 8.21 cents, or 7.6%, from last Friday’s open of $1.0854/gallon. This almost completely reversed last week’s loss of 8.11 cents. U.S. average retail prices for diesel fell by 1.3 cents per gallon during the week ended November 2 to average $2.372/gallon. Diesel prices generally have weakened this year, missing some of the price recovery seen in crude and gasoline markets. The week is headed for a finish in the black. Currently, diesel is trading in the range of $1.1378-$1.1675/gallon. The latest price is $1.1522/gallon.

Source: Prices as reported by DTN Instant Market

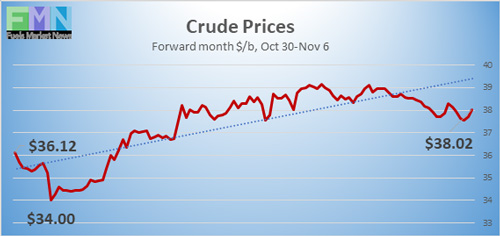

WTI Crude Prices

WTI crude futures prices opened at $38.54 a barrel today, a recovery of $2.47 a barrel (6.8%) from last Friday’s open of $36.07 a barrel. Prices today appear to be tapering down, though weekly gains are being held. Expectations of demand have fallen, both at home and abroad, with the alarming increase in COVID-19 cases. U.S. cases are surging faster than anywhere else in the world. Futures prices are hovering in the range of $37.50–$38.50 a barrel currently. The week appears to be headed for a finish in the black, recouping some of the losses from the prior week. WTI crude is trading in the $37.33–$38.61 a barrel range currently. The latest price is $37.86 a barrel.

PRICE MOVERS THIS WEEK: FULL BRIEFING

Oil prices and stock markets have been moving back up this week, though the country remains on tenterhooks over the U.S. presidential election. Former Vice President Joe Biden holds a narrow lead over President Donald Trump, but votes are still being counted. As this plays out, the country is freshly alarmed over surging COVID-19 cases. New daily cases of COVID-19 shattered records by topping 100,000 on both Wednesday and Thursday. Health experts warn that the coming of winter and the holiday season could worsen the spread as people visit family and socialize more indoors. Today, WTI crude futures prices opened at $38.54 a barrel today. Prices have been tapering down this morning. Still, oil prices appear to be heading for a finish in the black this week, recouping a portion of last week’s hefty losses. The Dow Jones Industrial Average also bounced back this week, though early indicators point to a slight pullback today.

COVID-19 cases are surging. Deaths exceed 1.23 million globally. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 48,600,362, with 1,232,209 deaths. Confirmed cases in the U.S. have risen to 9,606,369. U.S. deaths attributed to the disease have reached 234,911. The U.S. is in the grips of another surge. At this point, there is no state in the union that can claim to have the disease under control. Nationwide, new cases on Wednesday exceeded 103,000, a new record smashed the next day when new cases hit 116,255. According to the COVID Tracking Project, states reported that the Wednesday-to-Wednesday week brought a 20% increase in new cases, a 14% increase in hospitalizations, and an 8% increase in deaths.

The Bureau of Labor Statistics (BLS) released the Employment Situation Report, also known as the Jobs Report, for October this morning. Total nonfarm payroll employment grew by 638,000 in October. The unemployment rate fell to 6.9%. According to the BLS: “These improvements in the labor market reflect the continued resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. In October, notable job gains occurred in leisure and hospitality, professional and business services, retail trade, and construction. Employment in government declined.”

Initial weekly unemployment claims declined modestly last week. According to data collected by the Department of Labor, initial claims totaled 751,000 during the week ended October 24, down by 7,000 from the prior week’s upward-revised figure of 758,000. Initial weekly claims finally subsided below the one-million mark at the end of August, but they had been stuck stubbornly above 800,000 until just the past three weeks. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the week of March 28, initial jobless claims skyrocketed to hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. During the week ended August 8, claims finally fell below one million, but they were not able to sustain the downward trend. During the 33 weeks since U.S. states began to issue shelter-in-place orders, over 66.7 million Americans have filed initial jobless claims. Some are at the point where benefits are running out.

Shell announced that it has been unable to sell its 240,000-bpd refinery in Convent, Louisiana, and the company has decided to close it by February 2021. The refinery will still be listed for sale in case a buyer can be found. Shell’s strategic plan has been to cut standalone refineries in favor of facilities that integrate refining, petrochemicals, and biofuels. The Louisiana refinery has suffered from poor margins, and it has been battered by hurricanes and storms.

The U.S. Energy Information Administration (EIA) published official inventory data for the week ended October 30. The EIA reported a significant drain of 7.998 million barrels (mmbbls) from crude oil inventories. Gasoline inventories grew by 1.541 mmbbls. Distillate inventories were drawn down by 1.584 mmbbls. The EIA net result was a significant inventory drawdown of 8.041 mmbbls. These results meshed well with the data published a day earlier by the American Petroleum Institute (API,) which also reported an 8.0-mmbbl drawdown from crude oil stocks.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed in July through early August, sending Cushing stocks back up to 53,289 mmbbls during the week ended August 7. Cushing stocks have trended up in September and October. The week ended October 30 showed Cushing crude stocks at 60,931 mmbbls.

During the week ended October 23, U.S. crude production subsided to 10.5 mmbpd, down 0.6 mmbpd from the prior week’s 11.1 mmbpd. Some of the downturn was attributed to Hurricane Zeta. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. In August, however, production fell to an average of 10.475 mmbpd before rising to 10.575 mmbpd in September. October production averaged 10.6 mmbpd.