MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

September 06, 2019: Markets were closed on Monday in honor of Labor Day. Tuesday started with WTI crude prices dropping below the $53/b mark on reports of an unexpected crude inventory build and concerns over the U.S.-China trade war. However, prices rebounded on Wednesday when official statistics showed instead an across-the-board drawdown from crude and product inventories. On Thursday, China and the U.S. announced that a deputy-level trade talk was planned, restoring some market optimism. Today, the Bureau of Labor Statistics released the August Jobs Report, reporting that the non-farms payroll increased by 130,000 jobs, and that the unemployment rate remained unchanged at 3.7%. The BLS downwardly revised July’s jobs report to 159,000. Although the jobs formation was respectable, both figures fell short of economist forecasts. Today, prices are weakening. Our weekly price review covers hourly forward prices from 9AM EST Friday August 30th through Friday September 6th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.5784/gallon on Friday August 30th, and prices opened at $1.5461/gallon on Friday September 6th. This was a drop of 3.23 cents (2.0%.) U.S. average retail prices also fell during the week ended September 2nd. This week brought an inventory drawdown, which strengthened prices midweek. Gasoline prices are trending down this morning, and the week appears to be heading for an end in the red. Trades are occurring mainly in the range of $1.50-$1.55/gallon. The latest price is $1.5241/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.8671/gallon on Friday August 30th and opened on Friday September 6th at $1.8868/gallon, up by 1.97 cents (1.1%.) This week brought a surprise drawdown in diesel inventories, which strengthened prices midweek. Diesel forward prices have opened higher for four consecutive weeks. Prices this morning have weakened. Contracts currently are trading in the $1.84-$1.89/gallon range. The latest price is $1.8556/gallon.

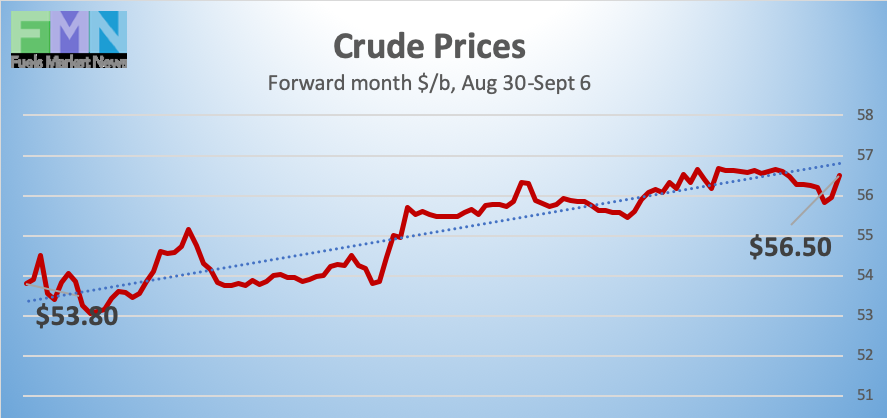

WEST TEXAS INTERMEDIATE PRICES

PRICE MOVERS THIS WEEK : BRIEFING

Markets were closed on Monday in honor of Labor Day. Oil prices opened on Tuesday at $55/b, but they shed more than a dollar when the American Petroleum Institute (API) reported a crude inventory addition of 0.4 million barrels (mmbbls.) This was contrary to market expectations of a 2.6-mmbbl stock draw. The API reported stock draws of 0.877 mmbbls from gasoline inventories and 1.2 mmbbls from diesel inventories. Market experts had predicted a larger draw from gasoline stockpiles, but also an addition to diesel inventories.

Prices recovered on Wednesday when the Energy Information Administration (EIA) instead reported across-the-board drawdowns from stockpiles. EIA reported drawdowns of 4.771 mmbbls of crude, 2.396 mmbbls of gasoline, and 2.538 mmbbls of diesel. The net stock draw was a significant 9.705 mmbbls.

The EIA also reported that during the week ended August 30th, U.S. crude oil production declined to 12.4 million barrels per day (mmbpd) from the prior week’s record high of 12.5 mmbpd. Official forecasts still foresee growth in output in the coming year, but there also is a note of caution, since many U.S. companies have struggled to maintain profitability. Baker Hughes reported that the U.S. active oil and gas rig count fell by 12 during the week ended August 30th. The rig count has fallen by 179 so far this year, dropping from 1083 at the end of December to 904 during the week ended August 30th.

The U.S.-China trade war continues to swing markets. Last week, China announced retaliatory tariffs on $75 billion worth of U.S. goods, including agricultural products, and also added a 5% levy on imports of U.S. crude oil. In 2018, China imported 228,000 bpd of crude from the U.S. During the January-May 2019 period, this fell to 111,000 bpd, in part because Chinese buyers feared that tariffs could be launched at any time. Some buyers hedged the risk by adding transport options to alternative ports to cover cargoes at sea. Some cargoes en-route to China now reportedly are being re-routed to India and South Korea. Yesterday, plans were announced that the U.S. and China would hold a deputy-level trade meeting, which caused a bounce-back in market optimism.

The U.S. Bureau of Labor Statistics (BLS) released the August Employment Situation report, showing non-farm payroll employment rising by 130,000 jobs and the unemployment rate staying unchanged at 3.7%. The BLS noted that some of the new jobs were temporary hires by the federal government for the 2020 Census. The BLS downwardly revised July’s jobs report to 159,000. Both figures fell short of economist forecasts, which had predicted the July figure to be 164,000 jobs and the August figure to be 158,000 jobs.

Hurricane Dorian wrought massive destruction in the Bahamas, and now is weakening as it brushes the North Carolina Coast. The National Hurricane Center lists it as a Category 1 hurricane. Dorian is bringing rain, storm surges, and wind.