MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

September 27, 2019: Crude prices fell daily this week, shedding approximately $4/b. WTI futures crude prices opened on Monday at levels over $59/b, and prices fell each day this week, dipping as low as $54.75/b. WTI prices currently have recovered to levels above $55.50/b. Weekly supplies expanded as U.S. crude production and inventories grew, and as Saudi oil production capability began to be restored after the prior week’s attacks. Iran’s President claimed that the U.S. offered to remove sanctions in exchange for talks. This morning, President Trump denied this. Still, the possibility of relaxation of sanctions could add to future supply. Our weekly price review covers hourly forward prices from Friday September 20th through Friday September 27th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

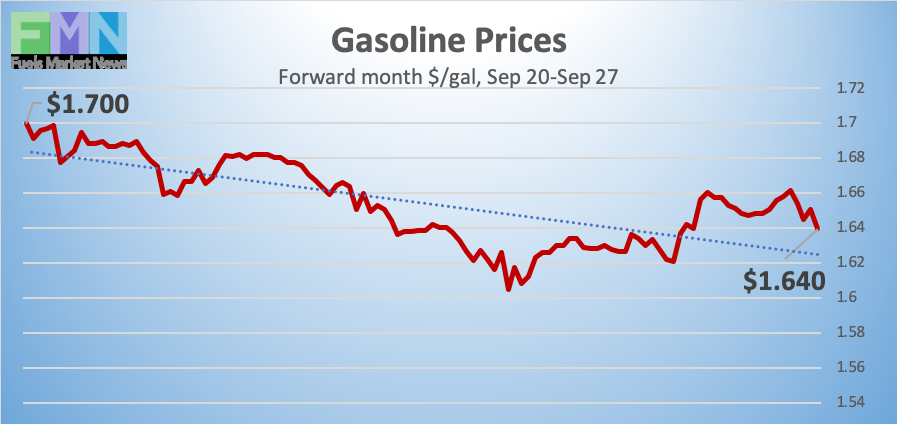

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.702/gallon on Friday September 20th, and prices opened at $1.6575/gallon on Friday September 27th. This was a drop of 4.45 cents (2.6%.) U.S. average retail prices jumped by 10.2 cents/gallon during the week ended September 23rd, and retail fuel prices have not yet followed crude prices down. Futures prices for gasoline dropped and then stabilized this morning. The week appears to be heading for a finish in the red. Trades are occurring mainly in the range of $1.62-$1.66/gallon. The latest price is $1.6385/gallon.

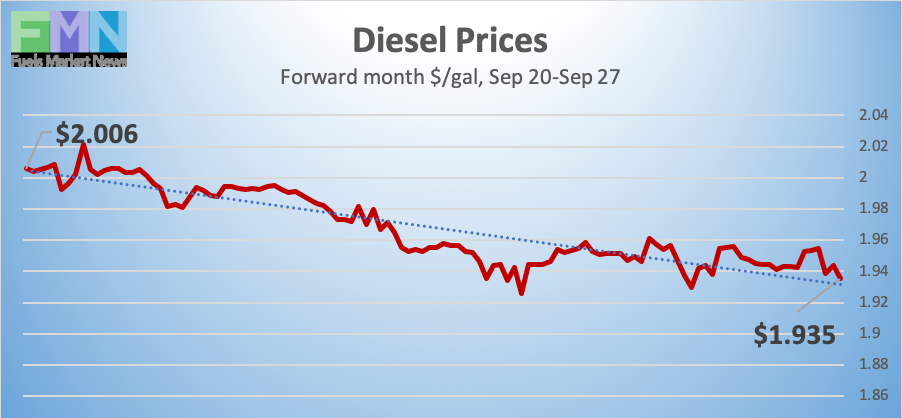

DIESEL PRICES

Diesel opened on the NYMEX at $2.0129/gallon on Friday September 20th and opened on Friday September 27th at $1.9563/gallon, a decline of 5.66 cents (2.8%.) Until this week, diesel forward prices had opened higher for six consecutive weeks. Last week’s diesel prices spiked above $2/gallon, when product prices followed crude up in the aftermath of attacks on Saudi oil facilities. Prices this morning dropped and then stabilized. Contracts currently are trading in the $1.92-$1.96/gallon range. The latest price is $1.9410/gallon.

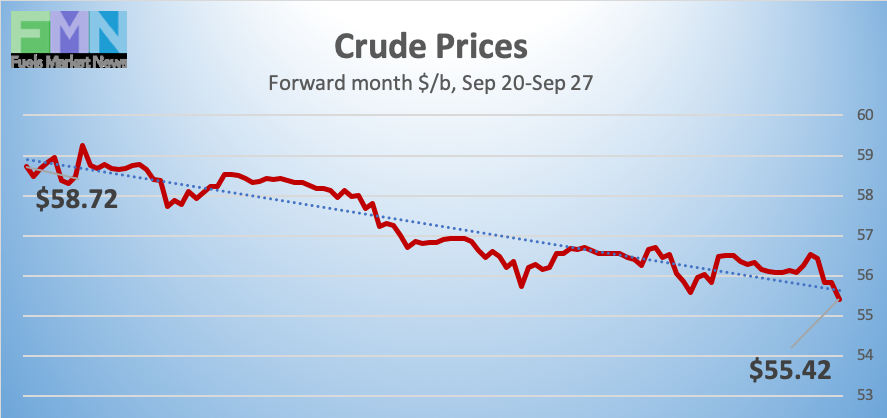

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday September 20th at $58.69/barrel and backslid to an open of $56.51/barrel on Friday September 27th, a decline of $2.18/b (3.7%.) Futures prices declined each day from Tuesday through Friday. Crude oil production and inventories expanded during the week. Saudi Arabian infrastructure is being repaired. The issue of Iranian exports continues to loom: Iran’s President stated that the U.S. might remove sanctions in exchange for talks, and prices dropped. U.S. President Trump then denied this, and prices quickly rebounded. This morning, prices are creeping back up, though the week appears to be heading for a finish in the red. WTI crude is trading mainly in the range of $54.75/b-$56.60/b. The latest price is $55.82/b.

PRICE MOVERS THIS WEEK : BRIEFING

Markets have been on edge, with uncertainty feeding volatility. Equities markets have gone up and down continually, though other factors have been at play. The Dow Jones Industrial Average has had near-daily reversals, dropping last Thursday and Friday, recovering slightly on Monday, dropping on Tuesday, bouncing back on Wednesday, and dropping again on Thursday. The overall trend has been down; the DJIA on Thursday the 26th was 200 points below the average the prior Thursday. Markets are expected to rise today based partly on news that the U.S. and China have scheduled trade talks for October 10th.

Oil prices already were relaxing, as supplies expanded and demand growth was forecast to be moderate. The expansion of supply has been driven by progress on repairs to Saudi Arabian oil infrastructure, plus a bump-up in U.S. crude production and inventories. The issue of Iranian exports continues to loom: Iran’s President stated that the U.S. might remove sanctions in exchange for talks, and prices dropped. This morning, U.S. President Trump denied this, and prices quickly began to rebound.

On the demand side, the International Energy Agency (IEA) cut its forecast of global growth to 2.9% this year, a significant drop from its forecast four months ago of 3.2%. The European Commission’s monthly indicator of economic sentiment dropped to its lowest level since 2015.

Oil inventory movements were more bearish than expected. Market experts had expected small draws on crude, gasoline, and diesel inventories this week. On Tuesday the American Petroleum Institute (API) an addition of 1.4 million barrels (mmbbls) to crude inventories plus an addition of 1.9 mmbbls to gasoline inventories, countered by a drawdown of 2.2 mmbbls from diesel inventories. The API’s net inventory build was 1.1 mmbbls.

The Energy Information Administration (EIA) released official statistics on Wednesday, showing a larger addition of 2.412 mmbbls to crude inventories, but this was more than countered by a large drawdown of 2.978 mmbbls of diesel. Gasoline inventories grew by 0.519 mmbbls. The net result was a small inventory draw of 0.047 mmbbls.

The EIA also reported that during the week ended September 20th, U.S. crude oil production rose again to 12.5 million barrels per day (mmbpd,) tying the weekly record achieved during the week of August 23rd.