MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

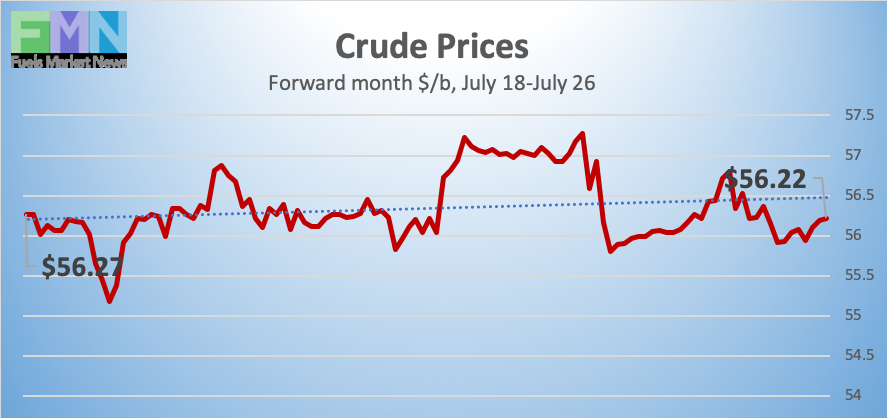

Oil prices rose then retreated this week, resulting in very little change. WTI crude prices have retreated to the $55-$56.50/b neighborhood, after a mid-July rally that brought prices to the $60/b level for the first time in seven weeks. Prices were supported midweek by reduced supplies, inventory drawdowns, and economic optimism. These forces were countered by a reduction in geopolitical tension and declines in several key markets around the world, which relaxed oil prices yesterday and today. Our weekly price review covers hourly forward prices from 9AM EST Friday July 19th through market opening Friday July 26th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

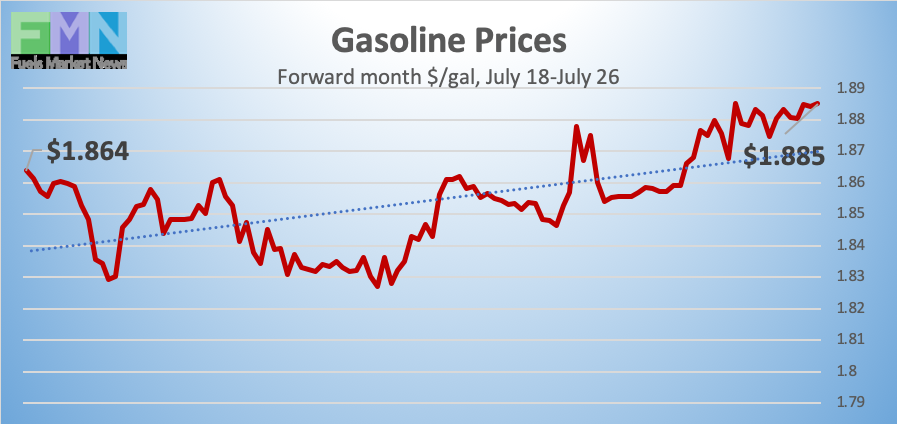

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.8486/gallon on Friday July 19th, and they opened at $1.8803/gallon on Friday, July 26th. This was a recovery of 3.17 cents (1.7%) following last week’s price collapse of 14.09 cents (7.1%.) This week brought a small drawdown in inventories, which bumped prices up midweek, and gasoline prices are holding some of the gains. Gasoline prices are stable with an upward tilt this morning, with trades occurring mainly in the range of $1.87-$1.89/gallon. The latest price is $1.8852/gallon.

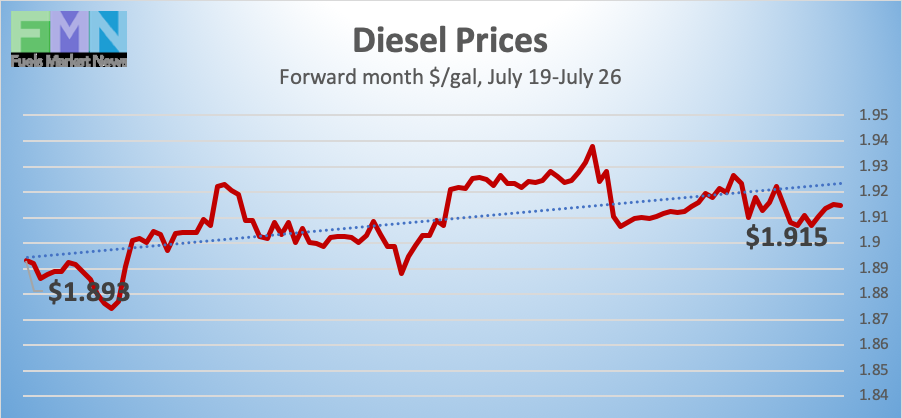

DIESEL PRICES

Diesel opened on the NYMEX at $1.8857/gallon on Friday July 19th and opened on Friday July 26th at $1.907/gallon, a small weekly recovery of 2.13 cents (1.1%), following the prior week’s sharp drop of 9.85 cents (5.0%.) Diesel prices are stable this morning, with contracts currently trading in the $1.90-$1.92/gallon range. The latest price is $1.9146/gallon.

WEST TEXAS INTERMEDIATE PRICES

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices rose and fell midweek, as bullish supply numbers created market interest. Price strength was reinforced by a number of U.S. corporate reports showing solid earnings. Late in the week, however, U.S. stocks slid upon disappointing corporate reports and forecasts. Many came in the technology sector, including PayPal, Microsoft, Apple, and Facebook, which was slapped with a $5 billion fine on Thursday by the Federal Trade Commission. Disappointing results also were handed in by vehicle and air travel companies including Ford, Tesla, American Airlines, and Boeing.

Geopolitical tensions also began to ease when Iranian President Hassan Rouhani suggested that Iran might release the U.K.-flagged Stena Impero if the U.K. released the Panama-flagged Grace 1 tanker seized off Gibraltar, which was suspected of smuggling oil to Syria in violation of EU sanctions. Suggesting a swap of sorts may be a way to improve relations between Iran and the U.K. under the U.K.’s new Prime Minister, Boris Johnson. Gibraltar was given the power to detain the tanker for another month.

U.S. oil supply, demand and trade were influenced by the aftereffects of Tropical Storm Barry. The U.S. Energy Information Administration (EIA) reported that U.S. crude oil production fell to 11.3 million barrels per day (mmbpd) during the week ended July 19th, as production facilities in the Gulf region were shut down in preparation. The weekly record-high was 12.4 mmbpd reported for the week ended May 31st.

Oil inventories also were affected by the storm, which not only shut in production, but also kept tankers offshore. On Tuesday, the American Petroleum Institute (API) reported a major drawdown of 11.0 million barrels (mmbbls) from crude oil inventories. Market experts had expected gasoline inventories to be drawn down, but the API reported a surprise stock build of 4.4 mmbbls instead, while diesel inventories rose by 1.4 mmbbls. Prices strengthened when official statistics were more bullish. EIA reported a crude stock drawdown of 10.835 mmbbls, very close to the API numbers, plus a small drawdown of 0.226 mmbbls from gasoline inventories, and a relatively small addition of 0.613 mmbbls to diesel inventories. The net stock drawdown was 10.448 mmbbls.