MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

Oil prices continued to dive mid-week, dropping below $51/b for the first time in nearly six months. Markets already were languishing under the prospect of a protracted trade war with China, and this was compounded with the threat of U.S. tariffs on Mexican goods. Wednesday brought news of a huge addition to U.S. oil inventories. The price decline was partly ameliorated by announcements from the Fed that it might cut interest rates this year if economic conditions warranted. Moreover, there are hopes that ongoing U.S.-Mexico trade talks will bring a resolution. WTI crude prices opened this morning $0.32/b (0.6%) below last Friday’s level. An unexpectedly weak Jobs Report this morning cast a pall on the economic outlook. Currently, crude prices are struggling to maintain a level of $53/b. Our weekly price review covers hourly forward prices from 9AM EST Friday May 31st through 9AM EST Friday June 7th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.8529/gallon on Friday May 31st, and prices opened at $1.724/gallon on Friday June 7th, a drop of 3.67 cents (2.1%.) Gasoline forward prices have dropped by 25.13 cents/gallon over the past three weeks. Gasoline prices regained ground yesterday, but prices are retreating again today, set back by a weak Jobs Report. The market may end the week in the red unless U.S.-Mexico trade talks show progress and/or the OPEC+ coalition makes further statements about production cuts. Gasoline trades are occurring mainly in the range of $1.70-$1.73/gallon. The latest price is $1.7087/gallon.

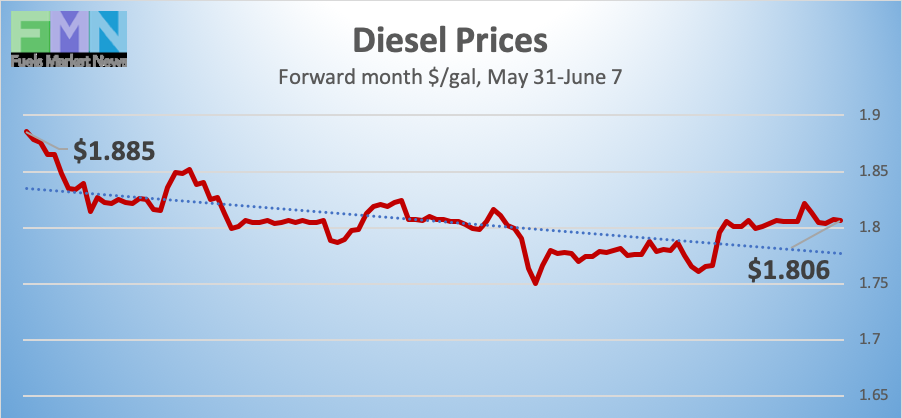

DIESEL PRICES

Diesel opened on the NYMEX at $1.9164/gallon on Friday May 31st and opened on Friday June 7th at $1.8011/gallon, a decline of 3.8 cents (2.1%.) Prices stabilized yesterday, but a weak Jobs Report is moving markets down again this morning. Diesel forward prices have plummeted by 24.89 cents/gallon over the last three weeks. Diesel contracts currently are trading in the $1.79-$1.82/gallon range. The latest price is $1.801/gallon.

WEST TEXAS INTERMEDIATE PRICES

PRICE MOVERS THIS WEEK : BRIEFING

Prices fell further on Tuesday when the American Petroleum Institute (API) reported across-the-board oil inventory additions: 3.6 million barrels (mmbbls) were added to crude oil inventories, 2.7 mmbbls were added to gasoline inventories, and 6.3 mmbbls were added to diesel inventories. The API net addition to inventories was 12.6 mmbbls.

Official statistics were even more bearish. The U.S. Energy Information Administration (EIA) reported across-the-board additions of: 6.771 mmbbls crude oil, 3.205 mmbbls gasoline, and 4.572 mmbbls diesel. The net addition was a massive 14.548 mmbbls. Oil prices fell to their lowest levels in nearly six months.

The Bureau of Labor Statistics (BLS) released the May Jobs Report. The BLS reported that non-farm payroll employment rose by only 75,000 in May, an unexpectedly weak result following the 224,000 jobs reportedly created in April. Economists had forecast employment to rise by 185,000 jobs. The unemployment rate remained unchanged at its already-low level of 3.6% (the lowest in 49 years.)

The jobs report is reason for concern, yet the downward spiral in oil prices appears to be leveling off. There are several possible factors supporting oil prices, including hope that U.S.-Mexico talks today will be productive. The Fed signaled that it could cut interest rates this year if needed. Saudi Arabia and Russia announced that they and the OPEC+ coalition remain committed to balancing the market, most likely extending their production cut agreement into the second half of the year. And the U.S. is tightening sanctions on Venezuela by restricting trade on diluents.