From The Desk Of The Publisher

We’ve listened to input by our readers and are making a few changes to our format. First, we’re changing from a daily fuels analysis to a more in-depth and nuanced weekly publishing schedule. We will still offer the exclusive analysis of the entire downstream fuel industry by Dr. Nancy Yamaguchi that you’ve come to trust and as you can see, we’ve actually expanded the analysis.

If you would like to subscribe to our free Friday newsletter, please click here!

Sincerely,

Gary Bevers, Publisher

MARKET SNAPSHOT

Oil prices surged at the opening of the week on news that the U.S. would end waivers on Iranian crude purchases. Prices began to ease midweek on additions to oil inventories. By Friday, rumors that the OPEC+ coalition will raise output caused a sharp downward correction, now stabilizing. Our weekly price review covers hourly forward prices from 9AM EST Thursday April 18 (Markets were closed on Good Friday) through 9AM EST Friday April 26. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $2.0484/gallon on Thursday April 18th and opened on Friday April 26th at $2.1298, up strongly by 8.14 cents (4.0%.) Tuesday April 23rd brought the week’s highest opening price of $2.1389/gallon, the highest price since July 2nd, 2018. Gasoline forward prices currently are stabilizing after a sharp downward correction, with trades occurring mainly in the range of $2.09-$2.13/gallon. The latest price is $2.1111/gallon.

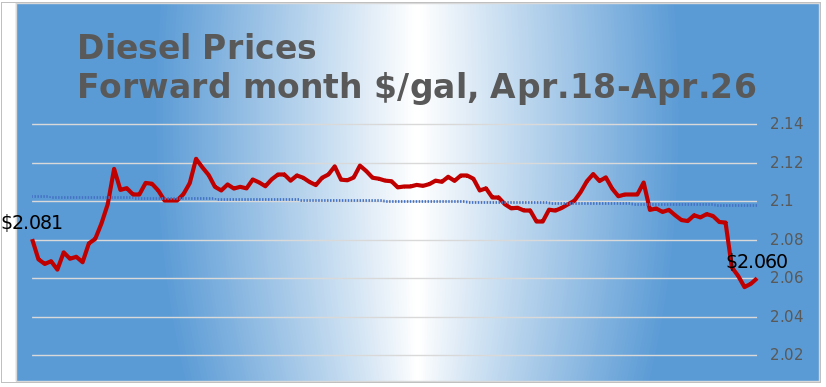

DIESEL PRICES

Diesel opened on the NYMEX at $2.0701/gallon on Thursday April 18th and opened on Friday April 26th at $2.0947, up by 2.46 cents (1.2%.) Wednesday April 24rd brought the week’s highest opening price of $2.1125/gallon, the highest price since December 24th, 2014. Diesel prices currently are stabilizing after a sharp downward correction, trading mainly in the $2.05-$2.10/gallon range. The latest price is $2.0636/gallon.

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX at $63.85/barrel on Thursday April 18th and opened on Friday April 26th at $65.13/barrel, up by $1.28/b (2.0%.) Wednesday April 24rd brought the week’s highest opening price of $66.17/barrel, the highest price since October 24th, 2018. Prices currently are stabilizing after a sharp downward correction, which brought a low point of $63.61/b. WTI is trading mainly in the range of $63.75/b-$64.50/b. The latest price is $64.39/b.

PRICE MOVERS THIS WEEK : BRIEFING

Prices began moving up quickly this week when the White House announced that it would end all waivers on purchases of Iranian crude. The U.S. declared that it would reimpose sanctions on Iranian crude when President Trump pulled out of the 2015 nuclear accord. Oil prices began the rise in the months leading up to November 2018, when the sanctions were scheduled to begin. Eager to avoid high prices in an election year, President Trump first pressured Saudi Arabia to ramp up its production to replace the lost supplies. The Saudis increased production by approximately 650,000 bpd between July and November. Yet the U.S. then also issued six-month waivers to China, India, Taiwan, Japan, South Korea, Italy, Greece, and Turkey. This greatly softened the market impact of the sanctions. Until this week, it was unclear whether the U.S. would extend the waivers. The White House wants to push Iranian exports to as close to zero as possible from current levels of around 1,000,000 bpd. However, Iranian crude exports are likely to continue in the at 400,000-500,000 bpd despite U.S. actions.

Midweek, it appeared that the supply situation could grow tighter, since Saudi Arabia has stated that it would not relax its production cuts before the Iranian sanctions kick in. Saudi Arabia indicated that it would raise production modestly by 200,000-300,000 bpd.

The upward price momentum slowed midweek when the American Petroleum Institute (API) and the U.S. Energy Information Administration (EIA) both published data showing increases in U.S. crude oil inventories. The API reported additions of 6.9 million barrels (mmbbls) to crude inventories and 2.2 mmbbls to gasoline inventories, with a drawdown of 0.9 mmbbls from diesel inventories. The net addition to inventories was 8.2 mmbbls. Official statistics from the EIA later placed the crude inventory addition at 5.5 mmbbls, and also showed a 2.1-mmbbl drawdown from gasoline inventories and a 0.7-mmbbl drawdown from diesel inventories. The net addition to oil inventories was 2.7 mmbbls, a less bearish picture.

Working to moderate rising prices, the International Energy Agency (IEA) released a statement noting that supplies were adequate, and that OPEC spare capacity is at 3.3 million barrels per day (mmbpd.) According to the IEA: “As a result of OPEC’s high compliance rate with the agreed supply cuts in the OPEC+ group, global spare production capacity has risen to 3.3 mb/d, with 2.2 mb/d held by Saudi Arabia and around 1 mb/d by the United Arab Emirates, Iraq and Kuwait.” By Friday morning, prices dropped sharply on rumors that the OPEC+ coalition, chiefly Saudi Arabia, UAE, Iraq and Russia, may elevate production. Prices are currently stabilizing after the sharp downward correction.