MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

November 22, 2019: Crude prices are rebounding after a midweek slump. News of continued oversupply and continued record-high (12.8 mmbpd) U.S. production depressed prices midweek, but prices began to recover upon less-bearish official statistics. The OPEC+ group, including a standoffish Russia, is likely to extend its production cut agreement through June 2020. Markets continue to feel optimistic about the U.S.-China trade war, although optimism may be tempered by the possibility that U.S.-China relations will suffer strain over U.S. support for pro-democracy protests in Hong Kong. In the Middle East, protests in Iran and Iraq have grown more deadly. Geopolitical risk may add support to oil prices. WTI futures crude prices opened on Friday, November 15, at $56.91/b, and prices strengthened to an open of $58.31/b today, up by $1.40/b. Currently, WTI futures prices are maintaining strength above the $58/b level. This week appear to be heading for a finish with oil prices in the black. Gasoline and diesel prices are following crude up today. Our weekly price review covers hourly forward prices from Friday, November 15, through Friday, November 22. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

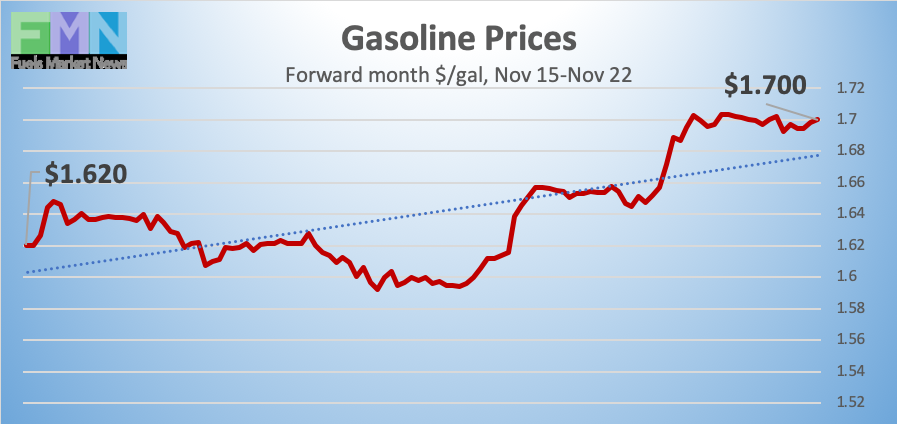

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.6191/gallon on Friday, November 15, and prices opened at $1.6971/gallon on Friday, November 22. This was a strong increase of 7.8 cents (4.8%) after last week’s decline of 2.08 cents (1.3%.) U.S. average retail prices fell by 2.3 cents/gallon during the week ended November 18th. Gasoline futures prices dropped significantly midweek when both the API and the EIA reported additions to inventories, but gasoline prices are following crude back up. Prices are currently stable, and the week appears to be heading for a finish in the black. Trades are occurring mainly in the range of $1.69-$1.71/gallon. The latest price is $1.7012/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.918/gallon on Friday, November 15, and opened on Friday, November 22, at $1.9401/gallon, up by 2.21 cents (1.2%.) This overwhelmed last week’s small loss of 0.11 cents (0.1%.) U.S. average retail prices for diesel rose fractionally 0.1 cent/gallon during the week ended November 18th. Diesel futures prices dropped midweek based on API and EIA reports of crude and gasoline inventory additions, despite the fact that diesel inventories themselves shrank. Diesel prices followed crude back up on Thursday and today, and prices currently are holding the gains. The week appears to be heading for a finish in the black. Contracts currently are trading in the $1.93-$1.96/gallon range. The latest price is $1.9473/gallon.

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, November 15, at $56.91/b, and prices strengthened to an open of $58.31/b today, up by $1.40/b (2.5%.) Currently, WTI futures prices are maintaining strength above the $58/b level. Crude prices are stable this morning in early trades, holding above the $58/b level and potentially reaching for $58.50/b. This week appear to be heading for a finish in the black. WTI crude is trading mainly in the range of $58.00/b-$58.75/b. The latest price is $58.24/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices are rebounding after a midweek slump based on yet another addition to oil inventories. U.S. crude production also remained at its new record-high level of 12.8 million barrels per day. Oil prices began to rebound upon positive economic sentiment combined with news that the OPEC+ group, including Russia, would likely extend its production cut agreement until June 2020. Russia has been standoffish about committing to the agreement, but on Wednesday, Russian President Putin stated that Russia and OPEC shared a “common goal” of keeping the oil market balanced, and that Russia would continue to cooperate. There may be, or at least should be, an element of geopolitical risk based on protests in Iran and Iraq. The impacts may be muted by the fact that Iran’s exports already have been stifled by sanctions. Nonetheless, violent protests can spread. WTI crude prices are showing strength this morning. Prices currently are holding above the $58/b level.

U.S. and Chinese officials continue to issue positive statements about progress on the trade war, which appear to be supporting market optimism despite the potential strain on U.S.-China relations caused by U.S. support for pro-democracy protesters in Hong Kong. Chinese President Xi Jinping, who largely has refrained from making statements on the negotiations, said that China wanted to work toward a Phase 1 agreement on the “basis of mutual respect and equality.” The situation is being described as “upbeat,” but given the protracted nature of the U.S.-China trade war, even this constructive statement can be taken as cryptic.

On Tuesday, the American Petroleum Institute (API) reported a larger-than-expected crude stock build of 5.9 million barrels (mmbbls.) Industry experts had anticipated a build of 1.318 mmbbls. Prices weakened. The API also reported an addition of 3.4 mmbbls to gasoline inventories, partly countered by a drawdown of 2.2 mmbbls from diesel stockpiles. Industry experts had anticipated a gasoline stock build of 0.754 mmbbls and a drawdown of 0.857 mmbbls from diesel inventories. The API’s net inventory build was a hefty 7.1 mmbbls.

The EIA released official statistics on Wednesday, showing instead a less-bearish crude build of 1.379 mmbbls. The EIA also reported a gasoline stock build of 1.756 mmbbls and a diesel stock draw of 0.974 mmbbls. The net result was a much smaller inventory build of 2.161 mmbbls.

The EIA also reported that U.S. crude production maintained its new record-high level of 12.8 mmbpd for the week ended November 15th. This has been accomplished despite a steady downward trend in active oil and gas rigs. The Baker Hughes rig count showed a weekly drop of 11 active rigs during the week ended November 15th. For the year to date, 269 rigs have exited the field.