MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

October 25, 2019: Crude prices rose mid-week, largely in response to a drawdown in oil inventories, OPEC discussions concerning deeper production cuts, and perceived progress on Brexit and the U.S-China trade war. WTI futures crude prices opened on Friday, October 18 at $54.09/b, and prices rose to an open of $56.07/b today, an increase of nearly $2/b. Brexit was not successfully concluded, however. The truce in the U.S.-China trade war is not considered potent enough to reduce the risk of recession, and additional data emerged showing signs of global economic slowdown. This appeared to end the rally, but the Pentagon just announced that it was considering sending armored vehicles to Syria to help U.S. troops defend oil fields. This may elevate geopolitical risks and stimulate interest in oil buying today. Currently, prices are strong, and WTI is back above $56/b. This week appears to be heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, October 18 through Friday, October 25. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.622/gallon on Friday, October 18, and prices opened at $1.6595/gallon on Friday, October 25. This was an increase of 3.75 cents (2.3%.) Prices have risen for three consecutive weeks. U.S. average retail prices rose by 0.9 cents/gallon during the week ended October 21st. Futures prices for gasoline are still trending up this morning in a three-day rally. The week appears to be heading for a finish in the black. Trades are occurring mainly in the range of $1.65-$1.67/gallon. The latest price is $1.669/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.9534/gallon on Friday, October 18 and opened on Friday, October 25 at $1.9841/gallon, up by 3.04 cents (1.6%.) Diesel prices have risen for three consecutive weeks. Diesel forward prices had surged in the aftermath of the attacks on Saudi oil facilities, dropped as production capacity was restored, then surged again after news of the attack on an Iranian-owned oil tanker. Diesel prices rose in early morning trades, but the upward momentum is now slowing. The week appears to be heading for a finish in the black. Contracts currently are trading in the $1.97-$1.99/gallon range. The latest price is $1.9728/gallon.

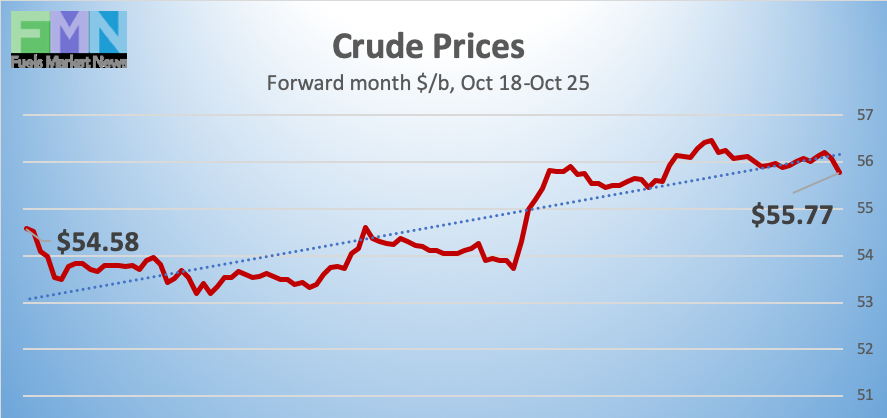

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, October 18 at $54.09/barrel and rose to an open of $56.07/barrel on Friday, October 25, a significant gain of $1.98/b (3.7%.) Prices flattened in early morning trades, and WTI prices sagged below $56/b. However, the possibility that the U.S. will send armored vehicles into Syria to help U.S. troops defend oil fields may increase geopolitical tensions and oil buying today. The week appears to be heading for a finish in the black. WTI crude is trading mainly in the range of $55.75/b-$56.25/b. The latest price is $56.09/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices staged a three-day rally midweek, and the week appears to be heading for a finish in the black. WTI crude prices have recovered the $56/b level. Market optimism was boosted by strong earnings reports, progress in U.S.-China talks, a long-awaited breakthrough in Brexit, OPEC discussions concerning additional production cuts, and a surprise drawdown from U.S. crude and product inventories. The price rally then slowed, as additional signs of global economic slowdown emerge. Germany reported that private sector employment fell for the first time in six years. Japanese factory activity fell to the lowest level in three years. South Korean economic expansion is slowing. The temporary truce in the U.S.-China trade war is not considered potent enough to overcome the risk of recession in the U.S. Moreover, the Brexit deal could not be concluded. U.K. Prime Minister Boris Johnson announced that he would seek a general election on December 12th for a national vote.

Oil buying interest may rise today based on increased geopolitical tension. After abruptly pulling troops out of Northern Syria to allow a Turkish invasion, the Pentagon announced that it was weighing the possibility of deploying armored vehicles to Syria to help U.S. troops defend oil fields. The situation is far from resolved, and it should be noted as a source of geopolitical risk.

Fuel prices weakened Tuesday when the American Petroleum Institute (API) reported an addition of 4.5 million barrels (mmbbls) to U.S. crude stockpiles. The API reported a drawdown of 0.702 mmbbls from gasoline inventories plus 3.5 mmbbls from diesel inventories. Market experts had predicted a crude build of approximately 2.5 mmbbls, outweighed by drawdowns of 2.2 mmbbls of gasoline and 2.8 mmbbs of diesel. The API’s net inventory build was 0.298 mmbbls.

The EIA released much more bullish official statistics on Wednesday. The EIA reported across-the-board draws from inventory: 1.699 mmbbls of crude, 3.107 mmbbls of gasoline, and 2.715 mmbbls of diesel. The net result was an inventory drawdown of 7.521 mmbbls.

The EIA also reported that U.S. crude production was maintained at its record-high level of 12.6 mmbpd for the third week running. Official forecasts still foresee growth in the coming year. There is a note of caution, however, with some analysts warning that the shale boom cannot continue. Russia’s Energy Minister, Alexander Novak, stated his prediction this week that U.S. shale output will peak in the next few years. One school of thought believes that it might be in Saudi Arabia’s best interest to launch another oil price war, since OPEC’s work to maintain oil prices benefits U.S. producers.