MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

April 17, 2020: Oil prices are continuing their downward march, as the excitement of the OPEC++ meetings fades, and focus returns to a grossly oversupplied oil market. Last week, buying interest was stoked by the idea that global producers, led by the OPEC+ group, would agree to cut production by 10-15 million barrels per day. The quotas were somewhat less, and their impact less because of the baselines from which they were calculated. The main issue remains the COVID-19 pandemic and demand destruction. OPEC forecasts that 2020 demand will drop by 6.8 mmbpd, with a contraction of 12 mmbpd in the second quarter, including a drop of 20 mmbpd in April. The International Energy Agency (IEA) foresees a much more serious drop in demand: a massive drop of 9.3 mmbpd in 2020, including a plunge of 29 mmbpd in April. U.S. markets sagged dramatically midweek on news of a truly gargantuan addition to crude and product inventories: 19.248 mmbbls of crude, 4.914 mmbbls of gasoline, and 6.28 mmbbls of diesel, totaling 30.442 mmbbls.

The COVID-19 pandemic continues to devastate the world, with cases in the U.S. soaring to 671,425. The U.S. death toll has risen to 33,286—more than twice the total just before the Good Friday holiday last week, which in turn were up from 6,058 the week before. Global confirmed cases have risen to 2,173,432, with 146,201 deaths. The Trump administration has created a plan for U.S. Governors to re-open their economies in a phased approach. The plan is one where the authority of the governors is acknowledged, and the re-opening is phased. Experts overwhelmingly favor a gradual approach with proper metrics, rather than a “flip the switch” approach. Stock markets are reacting favorably to this news, though oil prices remain depressed. WTI crude futures prices opened at $26.28/b Thursday morning, falling to an open of $20.00/b today. This week is heading for a finish in the red, with little to stimulate buying interest in the near term.

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Thursday, April 9, at $26.28/b. Markets were closed on April 10 in observance of the Good Friday holiday. Prices fell each day since to open at $20.00/b on Friday, April 17. Prices this morning dipped as low as $17.31/b (the lowest price in over 22 years). Currently, prices have regained the territory above $18/b. Our weekly price review covers hourly forward prices from Thursday, April 9th, through Friday, April 17th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

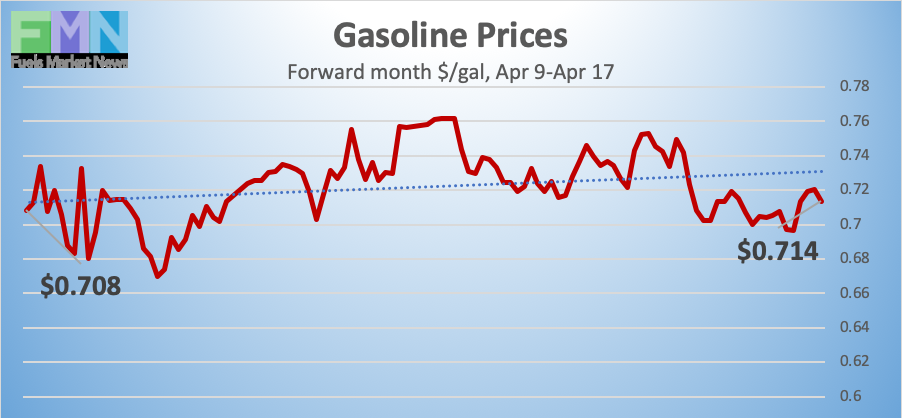

GASOLINE PRICES

Gasoline opened on the NYMEX at $0.705/gallon on Thursday, April 9, and prices crept up slightly to open at $0.7135/gallon on Friday, April 17. This was an increase of 0.85 cents (1.2%). Prices have been limping back after the month of March brought a crippling collapse of nearly 87 cents per gallon. U.S. average retail prices for gasoline dropped by 7.1 cents/gallon during the week ended April 13th. Gasoline futures prices are strengthening today in anticipation that various states soon will begin to relax shelter-in-place rules, and a finish in the black is possible for the week. Crude oil prices are weak today, however, so it may be difficult for gasoline futures to hold. Gasoline futures prices are trading in the range of $0.68/gallon to $0.73/gallon. The latest price is $0.7311/gallon.

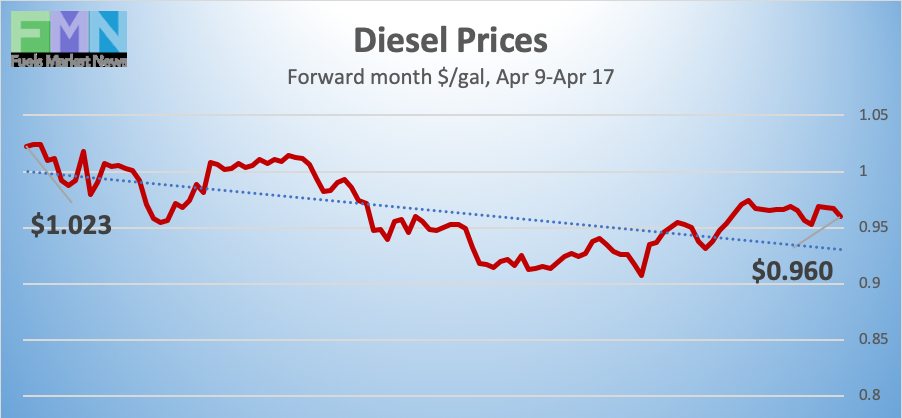

DIESEL PRICES

Diesel opened on the NYMEX at $1.03/gallon on Thursday, April 9, and opened on Friday, April 17, at $0.9619/gallon, a drop of 6.81 cents (6.6%). U.S. average retail prices for diesel fell by 4.1 cents/gallon during the week ended April 13th. Retail prices for diesel have fallen for fourteen consecutive weeks. Diesel futures prices fell sharply midweek on news of major additions to inventories. Diesel futures prices appear to be heading for a finish in the red this week. Currently, diesel is trading in the range of $0.95-$0.98/gallon. The latest price is $0.9529.

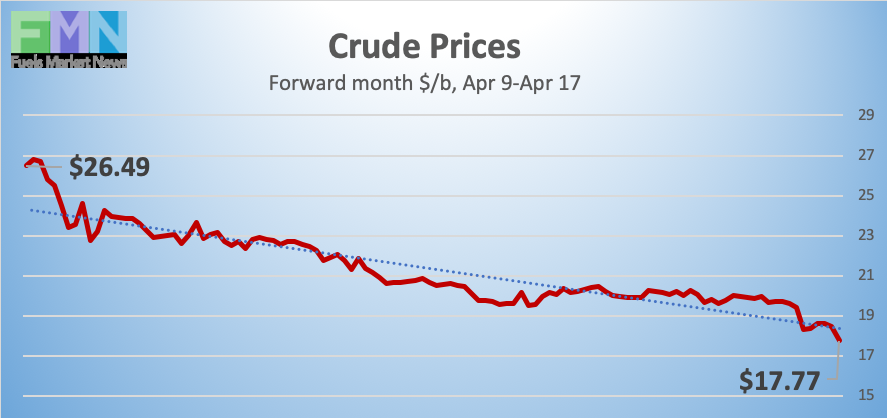

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Thursday, April 9, at $26.28/b. Buying interest had risen before the Good Friday holiday in anticipation of the OPEC++ meeting. The meeting results fell short of what had been hoped for, but even a high-end agreement would have fallen short of coping with the extensive demand destruction. Prices fell every day since to open at $20.00/b on Friday, April 17. The Thursday-to-Friday closure week brought a loss of $6.28/b (23.9%). WTI futures prices dipped to a low of $19.20/b on Wednesday upon news of a huge inventory build. Today, even this low point has been broken, with WTI prices dipping to $17.31/b. WTI prices are hovering around $18/b currently. The latest price is $18.02/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices are continuing their downward march, as the excitement of the OPEC++ meetings fades, and focus returns to a grossly oversupplied oil market. The week leading to the OPEC++ meetings was full of drama, and prices crept up to highs of over $28/b. U.S. President Donald Trump indicated that Saudi Arabia would end the oil price war, and that the OPEC+ group was close to a deal to , would agree to cut production by 10-15 million barrels per day. The quotas were somewhat less, and their impact less because of the baselines from which they were calculated. The main issue remains the COVID-19 pandemic and demand destruction. OPEC forecasts that 2020 demand will drop by 6.8 mmbpd, with a contraction of 12 mmbpd in the second quarter, including a drop of 20 mmbpd in April. The International Energy Agency (IEA) foresees a much more serious drop in demand: a massive drop of 9.3 mmbpd in 2020, including a plunge of 29 mmbpd in April. U.S. markets sagged dramatically midweek on news of a truly gargantuan addition to crude and product inventories: 19.248 mmbbls of crude, 4.914 mmbbls of gasoline, and 6.28 mmbbls of diesel, totaling 30.442 mmbbls.

The COVID-19 pandemic continues to devastate the world, with cases in the U.S. soaring to 671,425. The U.S. death toll has risen to 33,286—more than twice the total just before the Good Friday holiday last week, which in turn were up from 6,058 the week before. Cases in the U.S. are pulling away from the numbers reported in Spain (184,948) and Italy (168,941). Global confirmed cases have risen to 2,173,432, with 146,201 deaths. These numbers are updated constantly by Johns Hopkins University. The Trump administration has created a plan for U.S. Governors to re-open their economies in a phased approach and better testing capabilities is viewed as key.

Stock markets have been volatile, with optimistic reports of successful social distancing and curve flattening vying with the still-growing number of cases and deaths. The Dow Jones Industrial Average has been gradually recovering, but in spurts of two steps forward and one step back. The Dow opened above 24,000 today, signaling what is likely to be a positive day in the stock market. However, WTI crude futures prices opened at $26.28/b Thursday, April 9, falling to an open of $20.00/b today, and even sagging below $18/b in today’s early trading. Crude prices this morning are reviving slightly in anticipation of a relaxation of shelter-in-place rules, and they have regained the territory above $18/b. Still, this week is heading for a finish in the red, with only a minimal buying interest in the near term. In the longer term, the pullback in the oil industry could cause another supply disruption and price spike, but the sudden onset of the COVID-19 pandemic has hit the industry harder than any other modern-day event.

The reality of demand destruction was brought home sharply this week when the American Petroleum Institute (API) released information showing a huge crude inventory build of 13.1 mmbbls. The API also reported a build of 2.2 mmbbls of gasoline and 5.6 mmbbls of diesel. The API’s net inventory build was a massive 20.9 mmbbls. Market analysts had predicted across-the-board inventory additions similar to the API’s, with a total addition to inventories of 19.919 mmbbls.

U.S. Energy Information Administration (EIA) official statistics went further than the API’s, showing a truly gargantuan stockpile build. The addition to crude stocks was 19.248 mmbbls, the addition to gasoline stocks was 4.914 mmbbls, and the addition to distillate stockpiles was 6.28 mmbbls. The EIA net result was an astounding inventory build of 30.442 mmbbls.

U.S. crude production now is in decline, but at a slow pace as of the week ended April 10th. The EIA reported that U.S. crude production during the week ended April 10th fell to 1234 mmbpd, down 0.1 mmbpd from the prior week’s level of 12.4 mmbpd. According to this weekly data series, U.S. crude production averaged 13.025 mmbpd in February 2020, the highest total ever. April should bring a significant drop. Although the U.S. as a country is not deliberately trying to reduce production as part of any global pact, the collapse of prices is making many oil projects uneconomical. Moreover, the slump in demand is creating pressure on infrastructure. Distressed cargoes already are being priced at steep discounts.