By Josh Mikels, Lockton

How can representations and warranties (R&W) and pollution legal liability insurances indemnify environmental risks and protect potential buyers in a robust mergers and acquisition (M&A) environment?

Imagine that you are in the process of buying a company with potential environmental issues. While finalizing the purchase of the target company, you procure a representations and warranties insurance policy to enhance the limited indemnity given by the seller. Six months after the transaction closes, an environmental issue arises at one of the acquired sites. The matter was undisclosed, and the clean-up costs will exceed $1 million.

Is there insurance available to cover your loss? The answer may not be that simple.

What environmental issues?

Whether a business is a manufacturing operation, healthcare facility, fuel distributor or real estate developer—these operations have varying degrees of environmental exposures. Potential acquirers consider environmental issues during diligence. Any quantified liabilities can impact buyers and even put the brakes on a transaction. As part of a typical diligence process, buyers engage environmental consultants, environmental counsel and insurance specialists to conduct assessments. Environmental assessments range from desktop reviews of benign locations (i.e. leased warehouse and office space) to Phase I and Phase II assessments of owned or leased manufacturing locations. Additionally, as part of the diligence process, consultants determine what environmental insurances are in place (if any) to protect the assets in the underlying transaction.

What does the representations and warranties insurance cover?

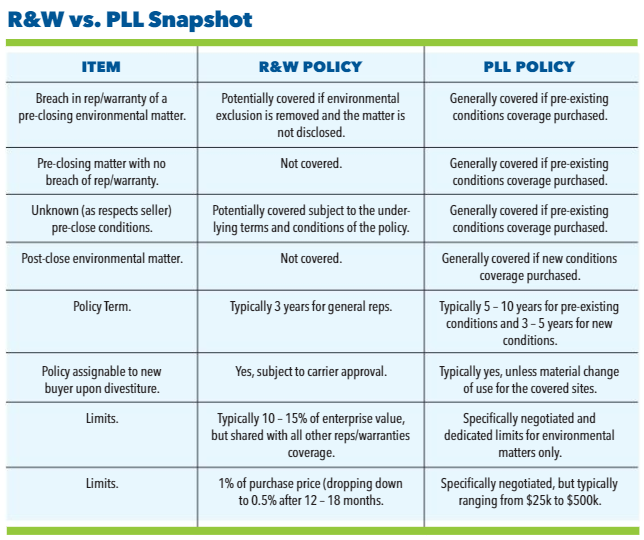

Every R&W insurance placement is subject to an insurer’s underwriting of a buyer’s underwriting process. Depending on the underlying risks of the target business, insurers may, at times, exclude environmental matters. Why? Because if there is an inherent risk to an underlying business, the R&W insurer would expect that the target business has a stand-alone pollution legal liability (PLL) policy to protect against these environmental risks. In certain circumstances, the environmental exclusion can be modified to sit excess of underlying pollution legal liability insurances. In these situations, an R&W insurer would consider providing excess coverage even if the proposed buyer were to put the insurance in place in conjunction with the closing. Lastly, with some tech and distribution businesses where the environmental risk is more benign, an insurer may remove the pollution exclusions altogether and excess coverage is a non-issue.

In each of the above-referenced situations, parties in a transaction need to consider what an R&W insurance policy covers: a breach in a representation or warranty made by the seller in an underlying transaction agreement. For example, if there is an environmental condition that the company knew about but did not disclose and made a representation that there were no environmental issues, this could be considered a breach and a claim filed for damages under an R&W policy.

Assuming in the above example that the environmental matter is a covered claim under the R&W policy, the R&W policy is subject to a retention (the amount before which insurance will pay). Typical R&W policy retentions are between 0.5 and 1 percent (depending on when during the policy period a claim is made). As such, on a $200 million purchase price transaction, the initial retention would be $2 million before insurance kicks in. If the claim is brought 12 months from closing, the retention will drop to $1 million. In either scenario, the R&W retention is significant and usually much higher than the retention for a stand-alone pollution legal liability policy.

What the R&W insurance policy won’t cover

There may be environmental conditions that a seller did not know about, and therefore, no specific representations or warranty was made. In such a circumstance, coverage is not triggered as there is no breach. Furthermore, there could be new environmental conditions that occur post-closing; in which case, the R&W policy would also not respond. The buyer would be on the hook for any damages or cleanup costs related to the environmental issue(s). For situations where there was a representation or warranty made, the typical R&W insurance policy covers only three years from the closing date for environmental matters. Occurrences that take place beyond this period would not be insured.

My R&W insurance policy won’t cover all the environmental issues—now what?

When R&W policies don’t cover certain issues, a pollution legal liability (PLL) policy may be something to consider. If a target company has potential environmental exposures, they may already have a PLL policy in place. If one exists, that policy would be evaluated during due diligence to ensure that it provides appropriate coverages for the underlying business. A PLL policy can be written if one does not exist. Terms could be structured to cover pre-existing conditions or known conditions for up to 10 years and new conditions for up to five years. The typical PLL policy term is a more prolonged survival period than the usual coverage afforded under an R&W insurance policy. Again, while known conditions are exclusions on R&W policies, a PLL policy can be tailored to cover specific known conditions. During underwriting of a PLL policy, schedule Phase I or Phase II reports to cover known conditions to the policy. Please note that more material known conditions may be specifically excluded and other exclusions could also apply, such as voluntary investigation and capital improvements. Therefore, even if there is no coverage in an R&W policy, a PLL policy could respond for covered claims for pre-existing and new conditions for third-party bodily injury, property damage and clean-up.

In addition, the PLL policy can also be structured to cover new conditions that arise post-close. Since it is a new environmental condition that didn’t exist pre-closing, it cannot be covered by R&W insurance. The PLL policy, however, can provide new conditions coverage if elected by the buyer when purchasing the policy.

For transactions where environmental or potential environmental issues are of concern, it is important to understand the roles that both R&W and PLL insurance can play in the transaction. While every situation is unique, both types of policies, if purchased, can play a role. Lockton can work with buyers in the due diligence process to not only help examine the environmental risks, but also in the procurement of PLL or R&W insurance, or both, depending on the situation and goals of the buyer.

More than 6,000 professionals at Lockton provide 50,000 clients around the world with risk management, insurance and employee benefits consulting services that improve their businesses. For more information, contact Greg Cushard, Sr. Vice President Lockton Insurance Brokers at cell: 916-730-4849 or office: 415-568-4115, email: [email protected]