Release Date: Nov. 7, 2023

Forecast overview

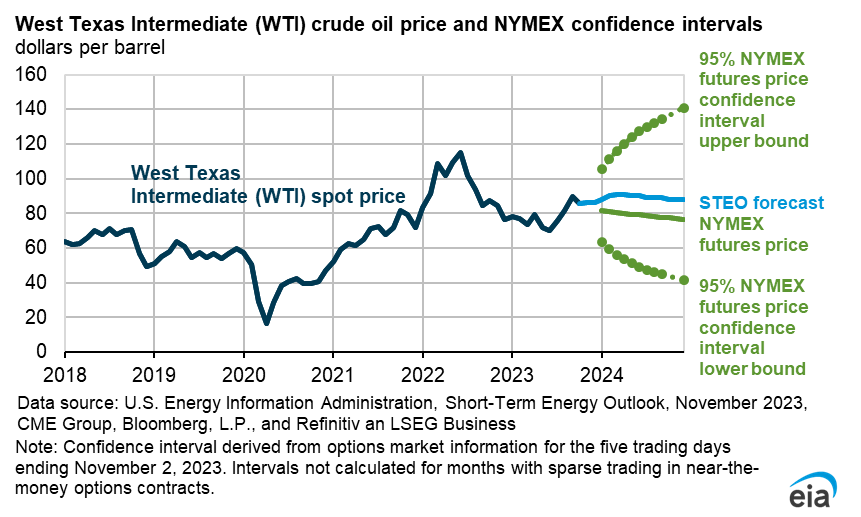

- Global oil supply. We forecast global liquid fuels production will increase by 1.0 million barrels per day (b/d) in 2024. Ongoing OPEC+ production cuts will offset production growth from non-OPEC countries and help maintain a relatively balanced global oil market next year. Although the conflict between Israel and Hamas has not affected physical oil supply at this point, uncertainties surrounding the conflict and other global oil supply conditions could put upward pressure on crude oil prices in the coming months. We forecast the Brent crude oil price will increase from an average of $90 per barrel (b) in the fourth quarter of 2023 to an average of $93/b in 2024.

- U.S. gasoline consumption. U.S. gasoline consumption declines by 1% in 2024 in our forecast, which would result in the lowest per capita gasoline consumption in two decades. An increase in remote work in the United States, improvements in the fuel efficiency of the U.S. vehicle fleet, high gasoline prices, and persistently high inflation have reduced per capita gasoline demand.

- Natural gas inventories. We estimate that U.S. natural gas inventories totaled 3,835 billion cubic (Bcf) feet at the end of October, 6% more than the five-year (2018–2022) average. We forecast U.S. natural gas inventories will end the winter heating season (November–March) 21% above the five-year average with almost 2,000 Bcf in storage. Inventories are full because of high natural gas production and warmer-than-average winter weather, which reduces demand for space heating in the commercial and residential sectors. We forecast the Henry Hub spot price to average near $3.20 per million British thermal units (MMBtu) in November, down from a price of almost $5.50/MMBtu a year earlier.

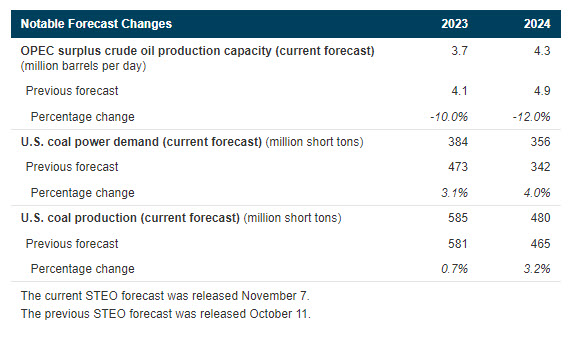

- Coal markets. U.S. coal exports have returned to pre-pandemic levels, driven by record-high global coal demand stemming primarily from Europe and Asia. We forecast that exports will rise to 97 million short tons (MMst) in 2023, because of increases in both steam and metallurgical coal exports. We expect steam coal exports to rise by 6 MMst compared with2022 to 45 MMst in 2023 and metallurgical coal exports to increase by 6 MMst to reach 52 MMst over the same period. Despite this increase in coal exports, we expect U.S. production to fall by more than 100 MMst in 2024 due to reduced demand from the electric power sector. The decline in electricity generation from coal will be offset by an increase in electricity generation from renewable resources.

- OPEC production capacity. Despite rising OPEC spare production capacity in 2023 and in 2024, we lowered our estimate of Iraq’s spare capacity by about 0.4 million b/d compared with last month’s STEO. We removed Iraq’s total production capacity assets in northern Iraq that relied on the northern Iraq-to-Türkiye pipeline for access to global markets. The pipeline has been out of commission since March 2023.