Excerpted from This Week in Petroleum

Release date: December 18, 2019

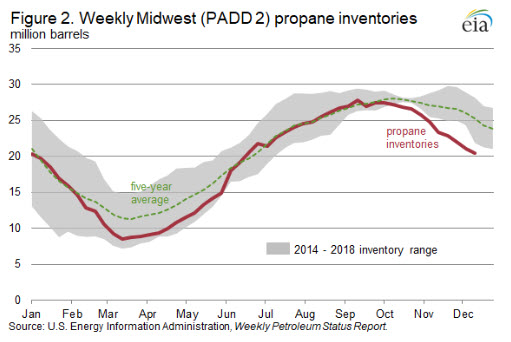

Propane inventories in the Midwest totaled 20 million barrels as of December 13, or 4.7 million barrels (19%) below the previous five-year (2014-18) average. Lower-than-average propane inventories were driven by both higher consumption and lower supply. A late and wet corn harvest in the Midwest resulted in increased agricultural propane demand, while supply of propane was lower because of disruptions to rail shipments from Canada. This situation is similar to the events of winter 2013-14 when extremely tight propane supplies in the Midwest led to record-level spot and retail prices.

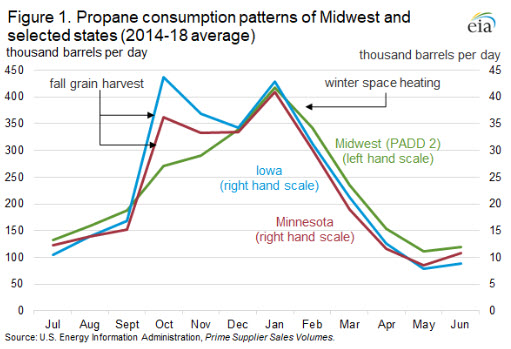

In the Midwest, or Petroleum Administration for Defense District (PADD) 2, propane is used for both agriculture and heating in homes and businesses. Midwest propane demand generally has two peaks: in the late summer and early autumn for grain drying (in the agricultural sector) and again during winter for space heating. In some states, such as Iowa and Minnesota, propane consumption during the grain harvest typically nears or exceeds consumption in the peak of the winter heating season (Figure 1).

However, the infrastructure to supply propane to the Midwest from other regions and to distribute propane within the Midwest are designed to provide steady flows throughout the year, not to meet its highly seasonal peaks in propane demand. Intra-regional pipelines, originating in the processing and storage hub of Conway, Kansas, account for most of the capacity to distribute propane within the Midwest. In addition, rail shipments from western Canada and some limited pipeline capacity bring supplies into the Midwest from other regions. As a result, local inventories, which build up in low-demand summer months and draw down in high-demand fall and winter months, act to balance the market

Retail propane markets in the Upper Midwest, such as in Iowa, Minnesota, Wisconsin, and Michigan, especially rely on supplies brought in from other areas. As such, local storage levels at the secondary and tertiary levels (such as small retail distributors and end-user storage tanks) determine immediate availability of propane to the local market. Therefore, inventory refilling activity during the summer is just as important to the region’s ability to meet heating-season demand as winter weather patterns.

The corn harvest is one of the largest drivers of agricultural demand for propane in the Midwest. For corn to be stored, it must first be dried either by leaving it in the fields (allowing the grain to dry) or by using large-scale heaters that often use propane or natural gas for fuel. If corn harvests are large and the weather is wet, propane demand may surge. If local propane inventories are lower than normal going into the second period of peak propane demand for residential space heating, the supply chain can become strained resulting in shortages and higher prices.

This year, the corn planting season was delayed as a result of cold, wet weather in the spring, and cooler summer weather resulted in a later-than-normal harvest and grain that had a high moisture content. According to the U.S. Department of Agriculture (USDA), this year’s corn crop was delayed by about three to four weeks compared to normal and only reached maturity in northern Midwest states by about the first week of November—the latest since 2009. The wet, cool weather during the harvest required accelerated drying in commercial dryers, often fueled by propane or natural gas, rather than drying in the field.

The late harvest (which is still ongoing in some states) means demand for propane from grain drying is overlapping with propane demand for space heating, resulting in larger-than-normal drawdowns of propane in the Midwest. Between the week ending October 4 and the week ending December 13, Midwest propane inventories decreased by 7.0 million barrels, compared with the five-year average decrease of 2.6 million barrels for the same time period (Figure 2).

A railway workers strike at Canada’s largest rail operator, CN Rail, put additional pressure on Midwest propane markets in November. The strike halted rail movements of propane from western Canada into the Midwest between November 19 and 27, when harvest-related propane demand was highest. Although the trains are now moving, the one-week delay in rail shipments impeded the ability of Midwest retailers to rebuild local inventories after the harvest-related draws earlier in the season.

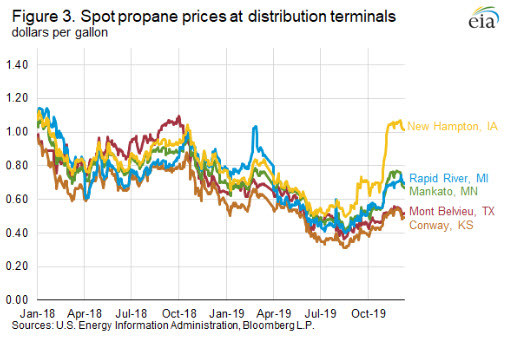

As a result of tight propane supplies, wholesale propane prices at several of the large propane distribution terminals in the Midwest have increased. Between September 3 and September 12, wholesale propane prices at the New Hampton, Iowa distribution terminal increased by $0.13 per gallon (gal) to $0.69/gal as a result of the corn harvest and associated grain drying that began in Iowa. Once states farther north began to draw on the same supplies, prices at other terminals in the Midwest also increased. On November 7, the wholesale propane price at Conway, Kansas, exceeded the price at Mont Belvieu, Texas, for the first time since June 2019. Prices rose throughout the region in response; from October 30 to November 8, the price at Mankato, Minnesota, was up by $0.15/gal, and the price at Rapid River, Michigan, was $0.11/gal higher. New Hampton, Iowa wholesale propane prices responded by rising again by another $0.23/gal during that period and have remained at more than $1.00/gal since then (Figure 3).

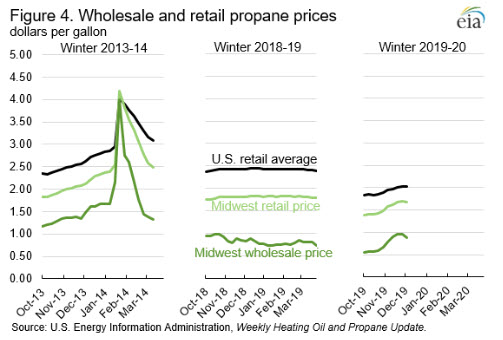

These higher wholesale prices have resulted in higher retail propane prices in the Midwest. The Midwest average retail propane price was $1.68/gal on December 9, an increase of nearly $0.30/gal since October 7, the start of the heating season (October to March) (Figure 4). However, retail propane prices are still lower than at the same time last year; the propane price at Conway is about $0.13/gal lower, and the Midwest average retail price is similarly $0.14/gal lower.

This year’s increased harvest-related demand for propane, lower-than-normal inventories, and supply chain disruptions are similar to what happened during the 2013–14 winter. In the fall of 2013, a large, late, and wet corn harvest required large amounts of propane for drying, reducing local inventories and raising prices. Not long after, a polar vortex arrived in the Midwest bringing temperatures that were significantly lower-than-normal to the area and resulting in a spike in propane demand for space heating. These events caused propane prices at Conway to increase rapidly and peak at $5.00/gal on January 23, 2014; supply chains were strained and widespread shortages were reported.