Analysis by Dr. Nancy Yamaguchi

Overview and COVID-19 Apparent Demand Response

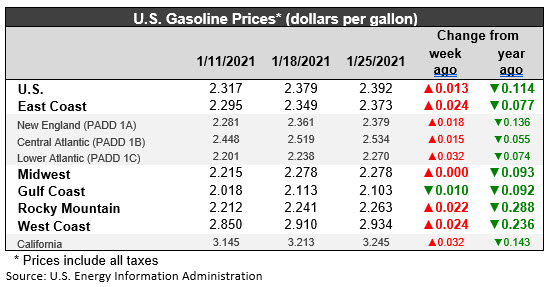

The U.S. Energy Information Administration (EIA) released its weekly data on diesel and gasoline retail prices for the week ended January 25. Retail prices continued to rise for both fuels, though at a more sedate pace. Gasoline prices rose by 1.3 cents per gallon, while diesel prices rose by 2.0 cents per gallon. Retail prices for gasoline averaged $2.392/gallon. Diesel prices averaged $2.716/gallon. The COVID-19 pandemic caused severe demand destruction, which has not been reversed fully. COVID-19 infections continue to rise, with global cases approaching 100 million. The U.S. accounts for more than one fourth of the global total, with over 25 million cases. Over 420,000 U.S. deaths are now attributed to the disease. At last, the U.S. seems to have reached a turning point, and the Johns Hopkins Coronavirus Resource Center reports that the most recent 7-day moving average of U.S. cases is trending down. More progress is expected for the first quarter of 2021. While this argues for continued increases in retail fuel prices, futures market prices now are moving more cautiously, suggesting that the upward trend in retail prices may slow down this week.

Retail diesel prices have now risen for the past 12 weeks. Retail gasoline prices have risen for nine consecutive weeks.

The EIA publishes weekly “product supplied” data as its proxy for demand. These data show gasoline demand crashing from 9,696 barrels per day (kbpd) during the week ended March 13 to just 5,065 kbpd during the week ended April 3, a huge hit of 4,631 kbpd in just four weeks. That was the low point. Demand thereafter trended generally up until it reached 8,608 kbpd during the week ended June 19. Since then, demand has cycled up and down, but it has never regained its March 13 level. Demand has been in the range of 7,400-8,900 kbpd. Gasoline product supplied rose to 8,128 kbpd during the week ended December 25, dropped sharply to 7,441 kbpd during the week ended January 1, 2021, then crept back up to 8,112 kbpd during the most recent week ended January 15. The EIA points out that “product supplied” is not a precise measure of demand, but these data provide the most up-to-date numbers publicly available.

Diesel demand dropped sharply in response to COVID-19. It began to recover in fits and starts. Diesel demand stagnated at first, recovered moderately, then began to vacillate between approximately 3,000 kbpd and 3,800 kbpd. The EIA reported that distillate fuel oil demand plunged by 1,256 kbpd between the week ended March 13 and the week ended April 10, slumping from 4,013 kbpd to 2,757 kbpd in a four-week period. Demand has been cycling up and down, rising strongly to 3,958 kbpd during the week ended August 21, then retreating to bottom out at 2,809 kbpd during the week ended September 11. This was the lowest reported level since the week ended April 10, reinforcing the concern that demand would not fully recover to pre-COVID-19 levels this calendar year. The EIA data for the week ended January 1, 2021, showed diesel demand plunging to 2,941 kbpd. Diesel supplied bounced back partway to 3,831 kbpd during the most recent week ended January 15.

It now has been 45 weeks since the week of March 13, before widespread COVID-19 lockdowns caused demand to collapse. As of the week ended January 15, 2021, gasoline product supplied was 84% of its pre-pandemic level. Diesel product supplied was 95% of its pre-pandemic level.

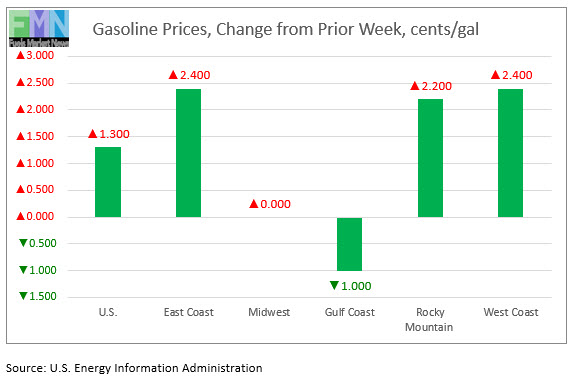

For the week ended January 25, retail prices for gasoline rose by 1.3 cents/gallon. Retail prices for diesel rose by 2.0 cents/gallon.

The national average price for gasoline was $2.392/gallon. This price was 11.4 cents/gallon below the price for the same week one year ago. Approximately 11 months ago in February 2020, retail prices for gasoline were higher than they had been in February 2019. The COVID-19 pandemic caused U.S. average gasoline prices to fall below $2/gallon throughout the months of April and May, regaining this average level in June. Retail gasoline prices are back above $2 a gallon in all five PADDs. The U.S. Gulf Coast PADD 3 was the last PADD to regain this price level. Prices are still below their levels of one year ago, but gasoline prices have now risen for nine consecutive weeks, and they are approaching their pre-pandemic levels.

Diesel prices also had been above last year’s level, but prices are now well below these levels. On a national basis, the retail price for diesel averaged $2.696/gallon—29.4 cents/gallon lower than the price in the same week last year.

Futures Prices and Retail Price Outlook

During the week January 19 to January 22, West Texas Intermediate (WTI) crude oil futures prices rose by $1.10 per barrel (2.1%.) Markets were closed on January 18 in observance of Martin Luther King Day. WTI futures closed the week at $52.27 a barrel. Recall that on October 30th, the market had slumped to close at $35.79 a barrel, the lowest level in approximately five months. As of Tuesday January 26, 2021, WTI crude futures prices are recovering after a market pullback, and prices are back in the range of $52.25-$53.25 a barrel. Crude oil prices may rise further this week, however, if trouble in Libya forces a force majeure declaration.

During the week January 19 to January 22, gasoline futures prices rose by 3.28 cents per gallon (2.2%.) Diesel futures prices rose by 3.46 cents per gallon (2.2%.) Futures prices for gasoline and diesel are recovering today after a pullback. Overall, prices have hovered in a narrow bandwidth over the past two weeks. While the relationship between futures prices and retail prices is not immediate or one-for-one, the strong upward futures price trend has flattened, suggesting that the upward momentum in retail prices will begin to slow.

Retail Diesel Prices

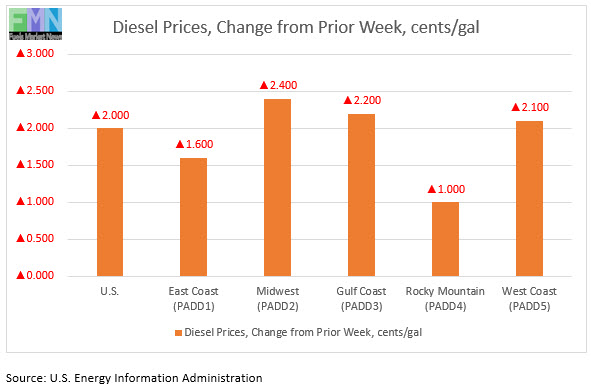

The week ended January 25 brought a 2.0 cents per gallon increase in the retail price for diesel to reach an average price of $2.716/gallon. Prices rose in all PADDs. The national average price for the week was 29.4 cents/gallon below where it was during the same week last year. Retail diesel prices have risen for twelve consecutive weeks. However, looking at 2020 in its entirety, prices dropped 44.4 cents per gallon between the first week of January and the last week of December.

In the East Coast PADD 1, diesel prices rose by 1.6 cents to reach an average of $2.763/gallon. Within PADD 1, New England prices rose by 1.7 cents to average $2.781/gallon. Central Atlantic diesel prices increased by 1.8 cents to average $2.942/gallon. Lower Atlantic prices rose by 1.5 cents to average $2.642/gallon. PADD 1 prices were 28.4 cents/gallon below their levels for the same week last year.

In the Midwest PADD 2 market, retail diesel prices rose by 2.4 cents to average $2.656/gallon. Prices were 24.5 cents below their level for the same week last year. PADD 2 joined PADD 3 during the week ended June 17, 2019, in having diesel prices fall below $3/gallon. Prices subsequently fell below $3/gallon in PADD 4 and PADD 1. Finally, PADD 5 prices also slid below the $3/gallon mark, though this reversed in November.

In the Gulf Coast PADD 3, retail diesel prices rose by 2.2 cents to average $2.483/gallon. PADD 3 continues to have the lowest diesel prices among the PADDs, currently 23.3 cents below the U.S. average. Prices were 29.0 cents below their level for the same week in the previous year.

In the Rocky Mountains PADD 4 market, retail diesel prices rose by 1.0 cent to average $2.613 gallon. PADD 4 prices were 37.1 cents lower than for the same week in the prior year.

In the West Coast PADD 5 market, retail diesel prices rose by 2.1 cents to average $3.176/gallon. PADD-5 is the only PADD where retail diesel prices are back above the $3 per gallon level. PADD 5 prices were 38.9 cents below their level from last year. Until December 2019, PADD 5 had been the only district where diesel prices were higher than they were in the same week last year. Subsequently, prices rose until this was true in all other PADDs. The pandemic caused a dramatic price drop, and the national average price is significantly below its level of last year despite the recent upward price trend. PADD 5 prices excluding California rose by 1.2 cents to average $2.816 gallon. This price was 38.2 cents below the retail price for the same week last year. California diesel prices rose by 2.9 cents to average $3.477/gallon. Until the week ended June 24, 2019, California had been the only major market where diesel prices were above $4/gallon, where they had been for nine weeks. California prices retreated below $4/gallon from July through October, rose above $4/gallon again during the first three weeks of November, then weakened until June and July 2020. California diesel prices were 38.0 cents lower than they were at the same week last year.

Retail Gasoline Prices

The COVID-19 pandemic continues to have a huge impact on the U.S. gasoline market. Retail prices for gasoline dropped below $2 a gallon in April, and they remained there throughout April, May, and into early June before finally climbing back to the $2/gallon level during the week ended June 8. Until the pandemic, it had been over four years since the average retail price for gasoline had been below the $2/gallon mark. With the phased re-opening of the economy, demand began to rise, as did prices. Unfortunately, so did coronavirus infections. Gasoline prices mainly trended down in the autumn of 2020. December brought a price recovery, which now has been sustained for nine consecutive weeks. The current week brought a price increase of 1.3 cents.

During the current week ended January 25, average retail prices for gasoline rose by 1.3 cents to average $2.392/gallon. Prices rose in PADDs 1, 4 and 5, fell in PADD 3, and remained unchanged in PADD 2. Retail gasoline prices for the current week were 11.4 cents per gallon lower than they were one year ago.

Looking back at historic prices, gasoline prices hit a peak of $2.903/gallon during the week ended October 8, 2018. Prices then slid downward for 14 weeks in a row, shedding a total of 66.6 cents per gallon. In the next 17 weeks, prices marched back up by 66 cents/gallon. Prices came very close to the peak they hit in early October 2018. However, the months of May and the June 2019 brought an easing of prices amounting to 23.3 cents per gallon. The week ended July 1 reversed that downward trend and sent prices up once again. The COVID-19 pandemic caused a price collapse, but prices began to climb back up in May, June, and early July. The second half of July brought a modest easing of prices, which levelled off in mid-August and began to reverse course. September and October brought another price retreat, in keeping with the end of summer driving season, and compounded by the pandemic. The current rally is pulling gasoline prices back up.

For the current week ended January 25, East Coast PADD 1 gasoline retail prices rose by 2.4 cents to average $2.373/gallon. This week’s average price was 7.7 cents/gallon below where it was during the same week last year. Within PADD 1, New England prices rose by 1.8 cents to average $2.379/gallon. Central Atlantic market prices rose by 1.5 cents to average $2.534/gallon. Prices in the Lower Atlantic market increased by 3.2 cents to average $2.270/gallon.

In the Midwest PADD 2 market, retail gasoline prices were unchanged at an average $2.278/gallon. PADD 2 prices for the week were 9.3 cents/gallon lower than they were for the same week last year.

In the Gulf Coast PADD 3 market, gasoline prices fell by 1.0 cent to average $2.103/gallon. During the week ended March 16, PADD 3 was the first region where retail prices fell below the $2/gallon level. It was joined subsequently by PADD 2, then by PADD 1, and then by PADD 4. PADD 3 was the last PADD remaining where prices were below $2/gallon. PADD 3 usually has the lowest average prices among the PADDs. PADD 3 prices for the week were 9.2 cents/gallon lower than for the same week last year.

In the Rocky Mountains PADD 4 market, gasoline pump prices rose by 2.2 cents to average $2.263/gallon. This week’s PADD 4 prices were 28.8 cents/gallon lower than at the same time last year.

In the West Coast PADD 5 market, retail gasoline prices rose by 2.4 cents to average $2.934/gallon. PADD 5 typically has the highest retail prices for gasoline, and until mid-March it had been the only PADD where retail gasoline prices stayed above $3/gallon. Prices this week were 23.6 cents/gallon lower than last year’s price. Prices excluding California rose by 1.5 cents to average $2.576/gallon. This was 33.1 cents/gallon below last year’s price. California prices rose by 3.2 cents during the current week to average $3.245/gallon. California had been the last state where gasoline prices had remained above the $3/gallon line, but this changed the week ended March 30. On Thursday March 19, California led the U.S. by ordering a statewide shelter-in-place to combat the spread of COVID-19. This order affected approximately 40 million people, and other states followed suit. California gasoline prices gradually crept back up above the $3-a-gallon level in July. California retail gasoline prices were 14.3 cents per gallon below their levels from the same week last year.