Excerpted from This Week in Petroleum, June 29, 2022

Agricultural trends and renewable fuels targets drive ethanol and biomass-based diesel prices

The prices of renewable identification number (RIN) credits—the compliance mechanism used for the Renewable Fuel Standard (RFS) program administered by the U.S. Environmental Protection Agency (EPA)—have increased in 2022 back to near the record prices set last year. The biomass-based diesel (D4) RIN peaked on April 28 at $1.91 per gallon (gal), and the ethanol (D6) RIN peaked at $1.68/gal on June 7 (Figure 1).

The RFS sets annual targets for the amount of renewable fuels required to enter into the U.S. fuel supply to increase biofuels use. Obligated parties—petroleum refiners and importers of motor gasoline and diesel—comply either by blending biofuels into petroleum-based fuels or by purchasing RIN credits. Ethanol production generates D6 RINs, and biomass-based diesel production generates D4 RINs but can also be used to generate D5 advanced biofuel RINs or D6 ethanol RINs. RIN credits allow market participants to offset rising biofuel costs and to continue blending at levels suitable for RFS compliance. In general, RIN credit prices increase in two situations: when the cost of a biofuel is higher than the petroleum fuel into which it is blended, or when RFS targets increase more than market-driven biofuel consumption, which may lead to additional blending. The recent increase in biomass-based diesel D4 RIN prices is likely due to the first situation, and the recent increase in fuel ethanol D6 RINs is likely due to the second.

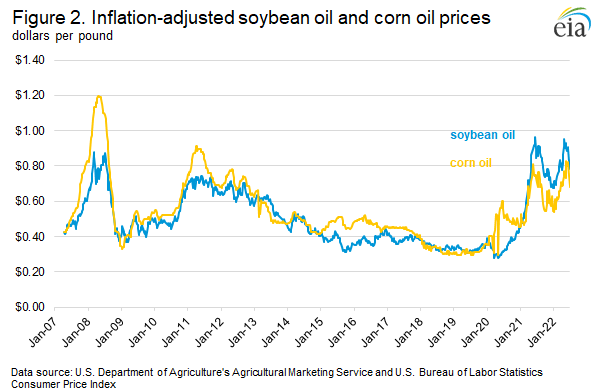

Rising global demand for the agricultural feedstocks used to make biomass-based diesel fuels has driven biofuel costs higher and has been a significant factor in increasing biomass-based diesel D4 RIN prices in 2022. Two common feedstocks for biodiesel and renewable diesel are soybean oil and corn oil. The spot price for Iowa soybean oil has been elevated for more than a year and reached a price of 94 cents per pound on April 29, 1 cent per pound lower than the record inflation-adjusted price set in June 2021. Spot prices for Illinois corn oil peaked on May 20 at 83 cents per pound, the highest real price since July 2011 (Figure 2).

Vegetable oils, such as soybean oil and corn oil, are used both as feedstocks for renewable fuels as well as for food. Because vegetable oils are somewhat interchangeable, their prices are affected by the aggregate supply of all vegetable oils as well as the supply and demand factors specific to the individual oil. Prices for soybean oil and corn oil, as well as other vegetable oils, have been near record highs so far in 2022 because of several factors, including the following:

- Russia’s full-scale invasion of Ukraine, because Ukraine accounts for two-thirds of global exports of sunflower oil and is the fourth-largest exporter of corn

- Drought and frosts in Argentina, the largest exporter of soybean oil, and drought in Brazil, the third-largest exporter of soybean oil, reducing production in those countries

- A temporary ban on palm oil exports from April 28 to May 19 in Indonesia, the largest supplier of the most produced vegetable oil

- A drought in Canada, the largest producer of canola oil, that cut canola production to its lowest level in 14 years

- Concerns that the La Niña weather pattern will bring hot and dry weather that negatively affects corn and soybean production in the United States

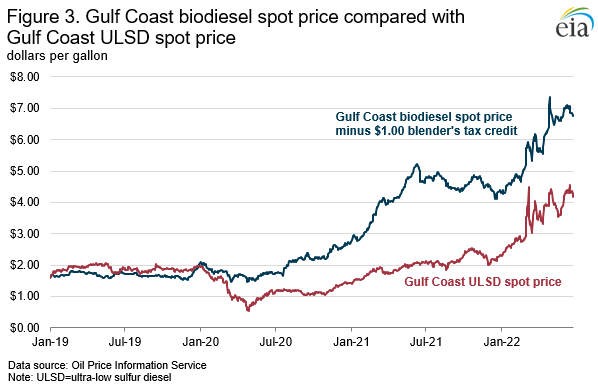

As feedstock costs have increased, biodiesel has become more expensive relative to petroleum diesel, and biomass-based diesel D4 RIN prices have had to increase to incentivize blending of biodiesel and renewable diesel. At its peak on April 28, the U.S. Gulf Coast spot price for biodiesel was $8.36/gal. Even when accounting for the $1.00/gal biodiesel tax credit that blenders receive for blending biodiesel, biodiesel spot prices were more than $3.00/gal more expensive than the $4.30/gal U.S. Gulf Coast spot price for ultra-low sulfur diesel (ULSD) (Figure 3). The margin has decreased slightly since then, reaching $2.61/gal on June 24, but remains big enough to necessitate high biomass-based diesel D4 RIN prices to drive enough blending of the fuel to meet the RFS targets.

Ethanol spot prices, however, have become cheaper relative to gasoline prices—which have increased to their highest inflation-adjusted prices since 2012 because of decreasing inventories, among other factors. This trend suggests that ethanol prices on their own would not necessitate high RIN prices to incentivize ethanol blending and that the recent increase in D6 RIN prices is likely because of an increased RFS target rather than increasing feedstock prices.

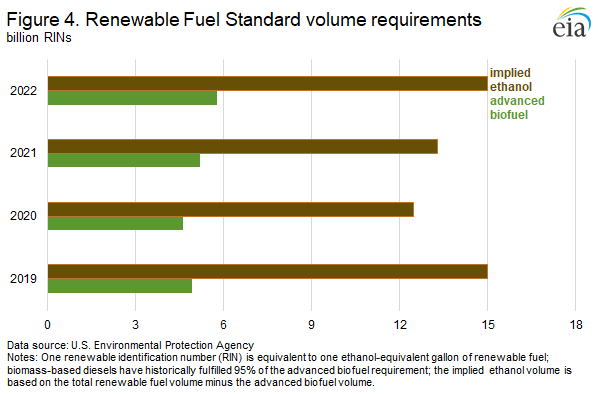

On June 3, 2022, EPA announced higher renewable volume obligations (RVOs) than in the previous two years (Figure 4). EPA set the biofuel target at 20.77 billion RINs in 2022, up from 17.13 billion RINs in 2020 and 18.52 billion RINs in 2021. Although some of the increase in biofuel targets must come from advanced biofuels, much of the increase will likely come from ethanol production. Obligated parties typically use ethanol to meet most of their volume obligations, although EPA sets no explicit targets for ethanol. We can calculate an implied target for ethanol by subtracting the volume obligations for advanced biofuels, biomass-based biofuels, and cellulosic biofuels from the total RFS fuel target. In 2022, like in 2019, the EPA set the implied ethanol target at the statutory maximum of 15.00 billion RINs. This target is an increase from 2020 and 2021, when they were lower because of reduced driving demand during the COVID-19 pandemic.

The higher RFS targets could increase the percentage of ethanol mixed into gasoline, yet there are several limitations to blending more ethanol. Most of the gasoline sold in the United States contains some ethanol, and E10 gasoline, which is a blend of 10% ethanol and 90% gasoline by volume, is the most common blend. A small portion of gasoline stations offer the higher ethanol blends of E15, which is a blend of up to 15% ethanol, and E85, which can contain up to 85% ethanol. Although relatively cheaper ethanol leads to more blending of E15 and E85, infrastructure constraints limit the supply of these blends. Most gasoline stations are not equipped with the necessary separate storage tanks and pumps to sell the less common blends. Because ethanol is comparatively less expensive than petroleum gasoline, E15 and E85 prices are also less expensive than E10. Even when accounting for the lower energy content of E15 and E85, lower prices can create greater consumer demand for the higher blend, so gasoline stations may upgrade their infrastructure to accommodate the blend. According to the EPA ruling, the 2022 RFS targets were deliberately set at a high level to facilitate investments in E15 and E85 infrastructure, and this high RFS target is contributing to higher D6 RIN prices in 2022.

The advanced biofuels target also increased and will likely be met with increased renewable diesel production. Historically, biodiesel and renewable diesel supply 95% or more of the non-cellulosic advanced biofuels target. We forecast U.S. biodiesel production to decrease slightly in 2022, but we expect renewable diesel production to increase significantly as new plants come online. So far in 2022, HollyFrontier’s Cheyenne, Wyoming, refinery has come online, and CVR Energy’s Wynnewood, Oklahoma, refinery has come partially online. Six other projects are scheduled to come online by the end of the year, which could bring renewable diesel production capacity up to about 180,000 barrels per day (b/d) by that time. Because of increasing production capacity, we forecast renewable diesel production to increase to 110,000 b/d in the fourth quarter of 2022 (4Q22), 39% more than in 4Q21. This increased renewable diesel production will likely meet the higher renewable fuels targets under the RFS program as well as meet carbon intensity standards under California’s Low Carbon Fuel Standard.