This morning, news was released that Pfizer was seeking emergency use authorization for its COVID-19 vaccination. This gave an immediate booster shot to markets. Prices spiked, then retreated. Could this be analogous to the idea that the vaccination will require two shots? The European Union could approve the shots as early as next month, which could strengthen markets irrespective of U.S. actions. The initial elation over the prospect of a vaccine had been tempered by the idea that it could take months before widespread use. Moreover, U.S. unemployment claims unexpectedly rose again last week. The optimism-pessimism pull-push is keeping prices roughly stable today. Prices this week had continued to recover but at a slower pace because of the growing wave of COVID-19 infections. New daily cases of COVID-19 continue to rise, with over one million new cases diagnosed in the U.S. in just the past week. In the oil sector, investors are placing renewed faith in the OPEC+ group. OPEC’s technical meeting this week is likely to result in the group extending its production cut agreement for an additional three months. The original plan called for an easing of the cuts beginning in January. Global demand, however, has not recovered as much as hoped, and the market remains oversupplied. The group has not achieved full consensus, particularly over Libya’s status, but the cuts are likely to remain in place. Some market analysts believe that crude prices would drop by at least $5/barrel without the OPEC+ cuts. OPEC will hold meetings November 30-December 1. Today, WTI crude futures prices opened at $41.70 a barrel. Crude and product prices surged then retreated this morning, and the week appears to be heading for a finish in the black. This will reinforce the past two weeks of price recovery.

COVID-19 cases continue to surge, breaking new daily records and bringing over one million new cases in just the past week. According to the COVID Tracking Project, new cases in the U.S. on Thursday broke yet another record, hitting 182,832. New cases have exceeded 100,000 per day for the past 16 consecutive days. The last seven days brought over 1.1 million new cases. Hospitalizations are at a record of 80,698. This may be considered the third, and worst, surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. Yesterday’s new total of 182,832 shattered old records. Health experts warn that the promise of vaccines in the future should not be used as an excuse to let guards down. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 57,042,406, with 1,363,182 deaths. There are 11,720,318 cases in the U.S., with 252,564 deaths.

Source: COVID Tracking Project

The unemployment situation took a turn for the worse last week when initial weekly unemployment claims rose significantly, rather than declining as economists had forecast. According to data collected by the Department of Labor, initial claims jumped by 31,000 during the week, rising to a total of 742,000 during the week ended November 14. The prior week’s figure was revised up by 2,000 to 711,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but they had been stuck stubbornly above 800,000 until just the past five weeks. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From there, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. During the week ended August 8, claims finally fell below one million, but they were not able to sustain the downward trend. During the 34 weeks since U.S. states began to issue shelter-in-place orders, more than 68.2 million Americans have filed initial jobless claims.

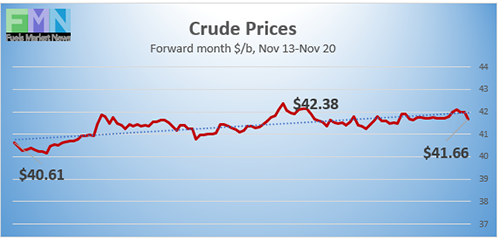

WTI crude futures prices opened at $41.70 a barrel today, an increase of $0.76 a barrel (1.9%) from last Friday’s open of $40.94 a barrel. WTI futures prices spiked then retreated today, trading in the range of $41.51-$42.12 a barrel currently. Prices are heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, November 13 through Friday, November 20. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

Gasoline Prices

Gasoline futures prices opened at $1.165 a gallon today on the NYMEX, compared with $1.1503 a gallon last Friday. This was a continued increase of 1.47 cents (1.3%,) building on last week’s recovery of 3.63 cents. U.S. average retail prices for gasoline rose by 1.5 cents to average $2.111/gallon during the week ended November 16. Retail prices reclaimed the territory above $2 per gallon during the first week of June. Gasoline futures prices are stabilizing after an early morning surge, trading in the range of $1.1589/gallon to $1.84/gallon. The week appears to be heading for a finish in the black for the third week in a row. The latest price is $1.1693/gallon.

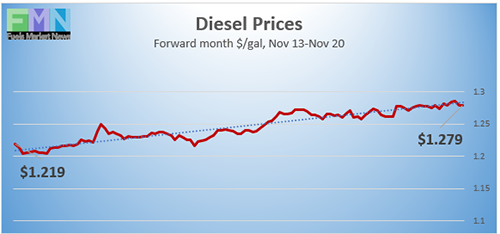

Diesel Prices

Source: Prices as reported by DTN Instant Market

Diesel opened on the NYMEX today at $1.2744/gallon, up significantly by 5.94 cents, or 3.9%, from last Friday’s open of $1.2269/gallon. This builds on the prior week’s recovery of 5.94 cents. U.S. average retail prices for diesel rose strongly by 5.8 cents per gallon during the week ended November 16 to average $2.441/gallon. Diesel prices generally have weakened this year, missing some of the price recovery seen in crude and gasoline markets. The past two weeks have reversed the downward trend. Currently, diesel futures prices are stabilizing after a brief surge, trading in the range of $1.2652-$1.2888/gallon. The week is heading for a finish in the black. The latest price is $1.2684/gallon.

WTI Crude Prices

Source: Prices as reported by DTN Instant Market

WTI crude futures prices opened at $41.70 a barrel today, an increase of $0.76 a barrel (1.9%) from last Friday’s open of $40.94 a barrel. Prices this week received support from the OPEC meeting, which is expected to result in a three-month continuation of production cuts. This morning, prices surged then retreated on news that Pfizer was seeking emergency authorization for its COVID-19 vaccine in the U.S. Perhaps it pleases the market to mirror the idea that the vaccination will require two shots? The optimism-pessimism pull-push is keeping prices roughly stable today. The COVID-19 pandemic continues to worsen, threatening economic recovery. U.S. cases are surging faster than anywhere else in the world, with over one million new cases added in just the past week. Futures contracts are trading in the range of $41.51-$42.12 a barrel currently. The week appears to be headed for a finish in the black, building on the past two weeks of price recovery. The latest price is $41.62 a barrel.

PRICE MOVERS THIS WEEK: FULL BRIEFING

This morning, news was released that Pfizer was seeking emergency use authorization for its COVID-19 vaccination. This gave an immediate booster shot to markets. Prices spiked, then retreated. Could this be analogous to the idea that the vaccination will require two shots? The European Union could approve the shots as early as next month, which could strengthen markets irrespective of U.S. actions. The initial elation over the prospect of a vaccine had been tempered by the idea that it could take months before widespread use. Moreover, unemployment claims unexpectedly rose again last week. The optimism-pessimism pull-push is keeping prices roughly stable today. Prices this week had continued to recover but at a slower pace because of the growing wave of COVID-19 infections. New daily cases of COVID-19 continue to rise, with over one million new cases diagnosed in the U.S. in just the past week. In the oil sector, investors are placing renewed faith in the OPEC+ group. OPEC’s technical meeting this week is likely to result in the group extending its production cut agreement for an additional three months. The original plan called for an easing of the cuts beginning in January. Global demand, however, has not recovered as much as hoped, and the market remains oversupplied. The group has not achieved full consensus, particularly over Libya’s status, but the cuts are likely to remain in place. Some market analysts believe that crude prices would drop by at least $5/barrel without the OPEC+ cuts. OPEC will hold meetings November 30-December 1. Today, WTI crude futures prices opened at $41.70 a barrel. Crude and product prices surged then retreated this morning, and the week appears to be heading for a finish in the black. This will reinforce the past two weeks of price recovery.

COVID-19 cases continue to surge, breaking new daily records and bringing over one million new cases in just the past week. According to the COVID Tracking Project, new cases in the U.S. on Thursday broke yet another record, hitting 182,832. New cases have exceeded 100,000 per day for the past 16 consecutive days. The last seven days brought over 1.1 million new cases. Hospitalizations are at a record of 80,698. This may be considered the third, and worst, surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. Yesterday’s new total of 182,832 shattered old records. Health experts warn that the promise of vaccines in the future should not be used as an excuse to let guards down. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 57,042,406, with 1,363,182 deaths. There are 11,720,318 cases in the U.S., with 252,564 deaths.

The unemployment situation took a turn for the worse last week when initial weekly unemployment claims rose significantly, rather than declining as economists had forecast. According to data collected by the Department of Labor, initial claims jumped by 31,000 during the week, rising to a total of 742,000 during the week ended November 14. The prior week’s figure was revised up by 2,000 to 711,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but they had been stuck stubbornly above 800,000 until just the past five weeks. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the week of March 28, initial jobless claims skyrocketed to hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. During the week ended August 8, claims finally fell below one million, but they were not able to sustain the downward trend. During the 34 weeks since U.S. states began to issue shelter-in-place orders, more than 68.2 million Americans have filed initial jobless claims.

The U.S. Energy Information Administration (EIA) published official inventory data for the week ended November 13. The EIA reported a modest addition of 0.769 million barrels (mmbbls) to crude oil inventories, plus an addition of 2.611 mmbbls to gasoline inventories. These were countered by a drawdown from diesel inventories of 5.216 mmbbls. The EIA net result was a small inventory drawdown of 1.836 mmbbls.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed in July through early August, sending Cushing stocks back up to 53,289 mmbbls during the week ended August 7. Cushing stocks have trended up this autumn. The current week ended November 13 showed Cushing crude stocks at 61,613 mmbbls.

During the week ended November 13, U.S. crude production rose by 0.4 mmbpd to reach 10.9 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. In August, however, production fell to an average of 10.475 mmbpd before rising to 10.575 mmbpd in September. October production averaged 10.6 mmbpd, and production during the first two weeks of November has averaged 10.7 mmbpd. The lower production averages this year have been attributed largely to shut-ins caused by record-breaking hurricanes, including Hurricanes Laura, Marco, and Zeta. So far this year, 30 named storms have formed over the Atlantic, breaking the last record of 28 storms in 2005, and making the year 2020 Atlantic hurricane season the most active one in recorded history.