Washington Wades Into the Markets

- EPA submits lower-than-expected 2026 RVO levels for White House consideration

- D4 RINs prices move lower after positioning for a more bullish announcement

- Small Refinery Exemptions next on EPA’s to-do list

- FERC warns about potential strains to electricity grids

Sincerely,

David Thompson, CMT

Executive Vice President

Powerhouse

(202) 333-5380

The Matrix

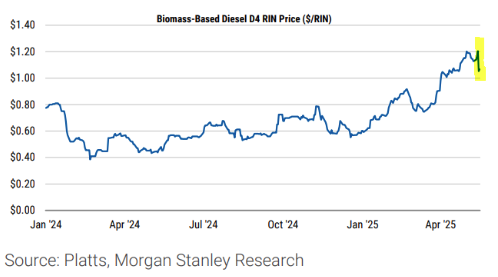

Late last week the Environmental Protection Agency (EPA) submitted its proposed rule for Renewable Volume Obligations (RVOs) for 2026 and beyond to the White House Office of Management and Budget (OMB) for review. RVO levels for 2026 are speculated to be 4.65 billion gallons — higher than 2025’s 3.35 billion gallon requirement, but below the 5.25 to 5.75 billion gallon recommendation made by an oil & biofuels coalition last month.

This development has led to a classic case of ‘buy the rumor, sell the fact’. D4 RIN prices had been rallying for most of 2025 on the basis of lower renewable fuel production and the prospect of a higher RVO level as a result of the combined lobbying efforts of two previously antagonistic industry groups, the American Petroleum Institute and the Renewable Fuels Association. With the news of a more easily achievable RVO level, D4 RIN prices sold off sharply.

Additionally, EPA Administrator Lee Zeldin testified to Congress that he intends to quickly clear the backlog of over 130 Small Refinery Exemption applications (SRE). This too could add downward pressure to RINs prices and by extension RBOB and ULSD prices. Finalization of the RVO rules will likely occur within 4-6 weeks while SRE announcements could come sooner.

These actions, taken in conjunction with efforts to jawbone OPEC into increasing production and streamlining the permitting process for U.S. drilling, show the Administration taking concrete steps to lower energy prices – an often-stated campaign pledge.

Supply/Demand Balances

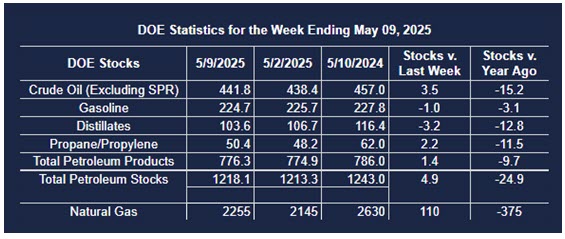

Supply/demand data in the United States for the week ended May 9, 2025, were released by the Energy Information Administration.

Total commercial stocks of petroleum increased (⬆) 4.9 million barrels to 1.2181 billion barrels during the week ended May 9th, 2025.

Commercial crude oil supplies in the United States were higher (⬆) by 3.5 million barrels from the previous report week to 441.8 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down (⬇) 0.7 million barrels to 8.0 million barrels

PADD 2: Down (⬇) 1.0 million barrels to 107.3 million barrels

PADD 3: Up (⬆) 1.9 million barrels to 251.4 million barrels

PADD 4: Up (⬆) 0.2 million barrels to 24.8 million barrels

PADD 5: Up (⬆) 3.1 million barrels to 50.5 million barrels

Cushing, Oklahoma, inventories were down (⬇) 1.1 million barrels to 23.9 million barrels.

Domestic crude oil production increased (⬆) 20,000 barrels per day from the previous report at 13.387 million barrels per day.

Crude oil imports averaged 5.841 million barrels per day, a daily decrease (⬇) of 214,000 barrels. Exports decreased (⬇) 637,000 barrels daily to 3.369 million barrels per day.

Refineries used 90.2% of capacity; an increase (⬆) of 1.2% from the previous report week.

Crude oil inputs to refineries increased (⬆) 330,000 barrels daily; there were 16.401 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, increased (⬆) 226,000 barrels daily to 16.610 million barrels daily.

Total petroleum product inventories increased (⬆) by 1.4 million barrels from the previous report week, down to 776.3 million barrels.

Total product demand decreased (⬇) 431,000 barrels daily to 19.441 million barrels per day.

Gasoline stocks decreased (⬇) 1.0 million barrels from the previous report week; total stocks are 224.7 million barrels.

Demand for gasoline increased (⬆) 77,000 barrels per day to 8.794 million barrels per day.

Distillate fuel oil stocks decreased (⬇) 3.2 million barrels from the previous report week; distillate stocks are at 103.6 million barrels. EIA reported national distillate demand at 3.777 million barrels per day during the report week, an increase (⬆) of 256,000 barrels daily.

Propane stocks rose (⬆) 2.2 million barrels from the previous report to 50.4 million barrels. The report estimated current demand at 416,000 barrels per day, a decrease (⬇) of 685,000 barrels daily from the previous report week.

Natural Gas

The EPA wasn’t the only Washington, D.C. based government entity making news last week. At its monthly meeting last Thursday, the Federal Energy Regulatory Commission (FERC) delivered its summer assessment. The Commission Chair stated that if summer weather is ‘average’ the nation’s energy grids should work as designed. With heightened demand, there could be issues.

“We are losing dispatchable generation at a pace that is not sustainable, and we are not adding sufficient equivalent generation capacity,” Federal Energy Regulatory Commission Chairman Mark Christie said. “Natural gas prices for summer 2025 are expected to be higher at all major trading hubs across the United States compared to summer 2024,” FERC staff noted. Meanwhile, U.S. natural gas demand is forecast to average 98.7 Bcf/d this summer, according to the Energy Information Administration. That would be around 1.7 Bcf/d higher than last summer, “and 9.7% more than the previous five-year summer average,” FERC staff added.

According to the EIA:

- Net injections into storage totaled 110 Bcf for the week ended May 9, compared with the five-year (2020–24) average net injections of 83 Bcf and last year’s net injections of 73 Bcf during the same week. Working natural gas stocks totaled 2,255 Bcf, which is 57 Bcf (3%) more than the five-year average and 375 Bcf (14%) lower than last year at this time.

- According to The Desk survey of natural gas analysts, estimates of the weekly net change to working natural gas stocks ranged from net injections of 97 Bcf to 119 Bcf, with a median estimate of 110 Bcf.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

This material has been prepared by a sales or trading employee or agent of Powerhouse Brokers, LLC and is, or is in the nature of, a solicitation. This material is not a research report prepared by Powerhouse Brokers, LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that Powerhouse Brokers, LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

Copyright 2025 Powerhouse Brokers, LLC, All rights reserved