Principal contributor: Matt French

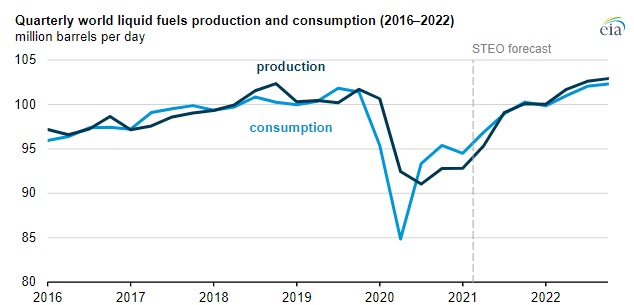

In the June Short-Term Energy Outlook (STEO), we forecast that rising global production of petroleum and other liquid fuels (driven by OPEC, Russia, and the United States) will limit price increases for global crude oil benchmarks Brent and West Texas Intermediate (WTI). We forecast production will increase more rapidly than consumption, ending the large global stock draws seen in the first two quarters of 2021 and limiting upward crude oil price movement.

At its June 1 meeting, OPEC+ (which includes OPEC members and several non-member countries) reaffirmed its commitment to continued production increases in the coming months. We forecast OPEC’s annual production to average 26.9 million barrels per day (b/d) in 2021 and 28.7 million b/d in 2022. We also forecast that production of petroleum and other liquids in Russia, an OPEC+ participant, will increase and that annual production will average 10.7 million b/d in 2021 and 11.5 million b/d in 2022.

The price of WTI crude oil increased from $52 per barrel (b) in January 2021 to $65/b in May, driving increases in the U.S. crude oil rig count—an indicator of active U.S. crude oil production capacity that is compiled by Baker Hughes. We expect the U.S. crude oil-directed rig count will likely continue rising in response to the rising WTI crude oil price.

We expect crude oil production in the United States will increase each quarter through the forecast period, averaging 11.4 million b/d in the fourth quarter of 2021 (4Q21), the highest level since 1Q20, and 11.1 million b/d for all of 2021. We expect U.S. crude oil production will average 11.8 million b/d in 2022.

Higher crude oil prices and planned OPEC+ production increases contribute to our forecast that global petroleum supply will increase over the next several months, resulting in an essentially balanced market in the second half of 2021. We then expect petroleum inventories to build in 2022 as production outpaces consumption.

Based on this global supply and demand forecast, we expect the Brent crude oil price will average $68/b in 3Q21. We expect the price to fall to $64/b in 4Q21 and decline further to average $60/b in 2022.

The extent to which countries adhere to the current OPEC+ production agreement and the volume of crude oil entering the market from Iran could push prices higher or lower. Similarly, if U.S. operators add fewer drilling rigs than expected, the result would be lower U.S. crude oil production in 2022, which would also affect prices.

For more a more detailed analysis, see This Week in Petroleum, published on June 9, and the June 2021 STEO.